Choosing between non-QM loans and conventional mortgages boils down to way more than just what interest rate you'll get and how much you'll pay each month - it's also about whether you'll even qualify for a home loan.

The two loan types serve totally different kind of borrowers, with conventional loans being perfect for people who work for a company and get a regular pay check and non-QM loans being the way to go for self-employed people, real estate investors, and anyone else with a financial situation that's a bit more complicated.

This guide will cover things like how to qualify for both loan types, how much it'll cost, and what you need to think about when making up your mind. Whether you're a 9-to-5 kind of person who's got steady pay stubs coming in the door, or a business owner who's got a tax return that doesn't exactly tell the whole story, understanding the difference between these two loan types will help you figure out which way to go.

This guide's for people who are trying to decide which loan to go with, self-employed people who are having trouble getting all the documents they need, and real estate investors who are looking to grow their portfolio.

The Big Difference: Conventional mortgages follow the rules set down by government sponsored enterprises Fannie Mae and Freddie Mac, which basically mean that they need to see real proof that you earn a steady income. Non-QM loans, on the other hand, are a bit more flexible and they let people qualify who don't fit into the standard, more rigid parameters, but at a higher cost.

By reading this guide, you'll be able to:

- figure out what makes a conventional loan vs a non-QM loan

- compare things like credit scores, down payments, and debt to income ratios

- understand the real cost difference, including interest rates, fees, and private mortgage insurance

- figure out which loan is right for your financial situation

- get a clear idea of the steps you need to take to get either one of these loans

Understanding Mortgage Loan Types

The mortgage market breaks down into two main types based on how lenders figure out if you can afford the monthly mortgage payments: loans that follow the federal rules and ones that don't. This makes a big difference in whether you qualify, how much it costs, and what kind of protection you get throughout the loan term.

Getting a clear idea of where you stand in these categories can save you a lot of time and help you focus on finding a lender who's got your back.

What are conventional mortgages

Conventional loans are these home loans that lack government backing from government agencies like the Federal Housing Administration (FHA) or Veterans Affairs (VA). Instead, they follow the rules set down by some government sponsored enterprises - Fannie Mae and Freddie Mac - that buy up loans from lenders and sell them on the open market.

Conventional mortgages break down into two basic types: conforming loans and jumbo loans. Conforming loans are loans that are within the standard limit for most areas of the US - currently $726,525 - and follow the Fannie and Freddie rules pretty strictly. Jumbo loans are bigger than that, but they still pretty much follow the same rules - you need to put a bigger down payment in and have a better credit score.

These loans are considered qualified mortgages which means they're allowed to charge up to 3% in fees, and they've got to follow some pretty strict rules to make sure that the lender can actually prove that the borrower can afford the payments. This is important because it means qualified mortgage status provides both lenders and borrowers with legal safe harbor protections, ensuring loans meet federal ability to repay standards set by the Consumer Financial Protection Bureau.

What are non-QM loans

Non-qualified mortgage loans - they're a whole different ball game when it comes to lending regulations. They deliberately don't align with Consumer Financial Protection Bureau (CFPB) mortgage guidelines, opting for alternative income verification methods to confirm the borrower's ability to make the monthly mortgage payments. This is not because the applicant lacks the ability to repay for a home, but rather because their financial situation doesn't fit neatly into the standard W-2 & paycheck picture.

These non-QM loans still have to comply with a broader rule about being able to afford the mortgage, but they have more flexible income verification methods and will accept things like 12-24 months of bank statements, 1099s for freelancers, investment account statements showing income from retirement accounts, or debt service coverage calculations for property investors.

Types of non-QM loans

Some of the more common loan types include:

- Bank statement loans: Use your bank statements to qualify instead of digging up tax returns

- Asset depletion loans: Qualifying based on how fast you can use up your liquid assets

- DSCR loans: A loan for investment property based on your rental income versus your mortgage payments

- Interest-only loans: Lower interest only payments in the beginning with the principal to be paid later, possibly through balloon payments

- Recent credit event loans: Options for people with credit challenges from bankruptcy or foreclosure

These non-QM products are a fairly new addition to the market, since 2017 reforms, with a market share of around 5-7% of all mortgage originations, reaching $44 billion by 2022. This represents the growing number of self-employed Americans now estimated at 40 million.

What Sets Non-QM Loans Apart From Conventional Mortgages

Once you understand what non-QM loans are all about, non-QM loans typically differ from conventional loans when you consider factors like your eligibility and costs.

What makes a borrower eligible and what documents are required

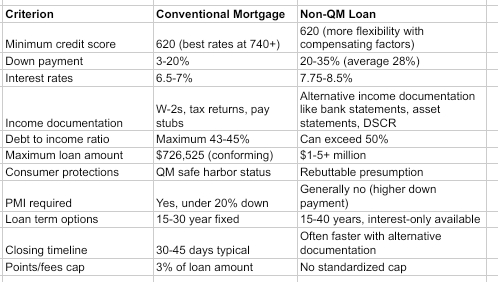

Credit Scores are one key area of difference. Conventional loans usually want a minimum credit score of 620, with the best interest rates available for borrowers with scores over 740. Non-QM loans also accept scores of around 620, but they're more willing to overlook low credit scores if you have a lot of cash on hand or a big down payment.

Income verification is another area where non-QM loans are significantly more flexible. Conventional loans want you to show two years of tax returns, W-2s from your employer, recent paychecks, and proof of employment history. But non-QM loans accept alternative income documentation tailored to people who own their own business, or rent out properties:

- 12-24 months of bank statements showing consistent cash flow

- 1099 forms for freelancers

- Investment account statements to show you have liquid assets

- A profit and loss statement with a letter from the accountant

- Documentation of rental income for your investment property

DTI ratios are also a key area of difference. Conventional loans limit your back-end DTI to around 43-45% - that's total monthly debt payments vs your monthly income. But non-QM loans often have higher ratios - sometimes exceeding 50% - when you have a lot of cash on hand or a high income that's not steady.

Employment History is another area where conventional loans can be more restrictive. They want two years of steady employment history. Non-QM loans are a bit more flexible - they look at your whole employment picture, rather than just the last two years.

Interest rates and fees

Interest Rates on non-QM loans are usually 0.25 - 1% higher than what you'd see on conventional mortgages - sometimes spiking up to an extra 1.5% during tough economic times. For now conventional rates are hanging around 6.5 - 7%, while non-QM loans typically have rates that top out at 7.75 - 8.5%, which can add up to a pretty big difference in monthly mortgage payments over the life of the loan.

For a 600 grand loan, that difference in rates looks like this:

- Conventional at 6.75%: About $3,893 a month for principal and interest payments

- Non-QM at 7.75%: About $4,298 a month for principal and interest payments

- Year over year that's an extra $4,860 in interest payments just because of the higher rate

Points and Fees get regulated in different ways depending on whether its a qualified mortgage or non-QM loan. For qualified mortgage loans lender fees are capped at 3% of the loan amount, while non-QM loans can tack on way higher origination fees and processing costs - and sometimes even hit you with a prepayment penalty. Closing costs on non-QM loans tend to be $3,000 to $8,000 higher than with a conventional loan.

Private Mortgage Insurance is going to kick in on conventional loans if you put down less than 20%, adding another 0.5 to 1.5 % on to your costs each year. Non-QM loans are different - they usually want a larger down payment or minimum down payment of 20 to 35%, which eliminates the need for PMI but means you end up putting more cash up front.

Loan features and terms

Repayment Plans can be a lot different between conventional and non-QM loans. Conventional mortgages are pretty standard - you make a monthly payment that includes a bit of principal and a bit of interest, and that's it for 15 to 30 years. Non-QM loans are a bit more flexible - some of them let you make interest only payments for a while, which cuts down your monthly payments at first but puts off reducing the loan balance.

Down Payment Requirements reflect how much risk lenders are taking on:

- Conventional: 3 to 20% down, and you'll need PMI with less than 20%

- Non-QM: 20 to 35% down, averaging 28% in 2024

Maximum Loan Limits are where non-QM loans have a real advantage, especially if you're looking to purchase property with a higher value. Conventional loans top out at $726,525, after which you need to get jumbo financing with stricter credit standards. Non-QM loans, on the other hand can take you all the way up to $1 to $3 million, and some private lenders have been known to lend on properties worth over 5 million.

Consumer Protections are a key difference between QM loans, which are qualified mortgages, and non-QM loans. Qualified mortgages get this special "safe harbour" status that means lenders and by extension, borrowers are protected from lawsuits over whether the borrower actually has the ability to repay the loan back. Non-QM loans don't have that, and are instead considered "rebuttable presumption" loans, which means lenders need to be super careful about documenting everything, but also don't offer as many standard borrower protections.

Detailed Comparison and Decision Framework

Building off the differences outlined above, the rest of this section provides some practical tools to help you figure out which loan type is right for your situation and your financial goals.

Side-by-side comparison table

When evaluating whether non-QM is a viable option, it's worth keeping in mind that higher costs don't necessarily rule out non-QM as a choice. The real comparison for some borrowers is going with non-QM lending, versus not getting a loan at all.

Who should be looking at conventional mortgages

Conventional loans are for borrowers who fit the standard documentation requirements - people who're pretty straightforward to qualify:

People who get regular paychecks, like W-2 employees, will often find conventional loans to be the best option. If you get paid on time every month, have two years of tax returns showing steady income or better, and have a credit score above 620, conventional mortgages, also known as traditional mortgages, generally offer the lowest interest rates and the strongest borrower protections available.

First timers who can't save up a down payment can benefit from conventional programs like Fannie Mae’s HomeReady - they offer a minimum down payment as low as 3% with income limits based on where you live. These programs make it possible to get into a home without needing to save up a ton of money.

Those who care most about the total cost of the loan should aim for conventional financing if they qualify - the combination of lower interest rates, capped fees, and the ability to sell the loan on the secondary market means you can save a significant amount - we're talking $50,000 to $100,000 on a 30 year loan term, compared to non-QM alternatives. That's a potentially huge difference.

And if you're someone who needs to know that your loan is going to be safe, conventional loans have got you covered. As qualified mortgages, they're QM safe harbor compliant, so you can be confident that your loan meets federal standards for responsible lending and that the lender has verified your ability to repay.

Who should be considering non-QM loans

Non-QM loans are usually for people who have strong finances but don't fit into the standard boxes that conventional lenders look at:

Self-employed and business owners often show minimal income on their tax returns because they're taking all sorts of deductions that are legitimate, but it doesn't give you a complete picture of how much cash flow they actually have coming in. For instance, a business might generate $500,000 a year, but the owner might only show $80,000 of taxable income after all the expenses they've deducted. That can make them ineligible for a conventional loan, even though they've got a ton of money coming in. Bank statement loans look at how much money you're actually taking in, not just what you're reporting on your taxes.

Real estate investors who are building up a portfolio of properties often hit a wall with conventional lending because most conventional lenders only want to finance 10 properties or fewer. DSCR loans work a bit differently - they look at the income from the property versus the debt payments to figure out how much you can qualify for.

So if you're looking to purchase property like a $1.5 million rental property that generates $12,000 a month in rent and your monthly debt payments are $9,000, that's a debt service coverage ratio of 1.33 - which is more than enough to get approved for a non-QM loan, regardless of what your W-2 income says. Speaking on the company's transition to direct lending, Matt Hickey, CEO of Launch Financial Group, a Non-QM lender based in New York says, DSCR loans underscore our commitment to empowering property investors with competitive financing options.

People who have been through a bit of a rough patch but are still sitting pretty with substantial assets might find non-QM is a more realistic option. Conventional loans often require 4-7 years of seasoning after a bankruptcy or foreclosure before you can get approved again. But non-QM lenders might be more willing to work with you if you've got significant assets in reserves. They're acknowledging that past credit challenges don't always mean you can't pay your bills now.

High-net-worth individuals who have a lot more going on in their financial picture than just a W-2 income can use asset depletion loans to qualify for a home loan. So if you're a retiree with $3 million in investments and no income coming in from a job, you might be able to qualify for a loan by dividing your assets by 360 months. That works out to $8,333 a month in equivalent income, which is more than enough to get approved for a mortgage. That's a door that's just not open with conventional lending.

Common Challenges and Solutions You'll Face

When it comes to loan categories, borrowers usually run into predictable hurdles that have some pretty standard workarounds.

Documentation challenges (Especially self-employed borrowers)

There's a real gap between the income you report on your tax return and how much money your business is actually making. This makes it tough for business owners to qualify for home loans. And to make matters worse, tax optimization strategies that cut down on liability also tend to cut down on the amount of income that gets documented.

The Solution: Some lenders use bank statement loans, which look at 12-24 months of deposits and apply qualification rates of 50-100% to the average monthly deposits. To get ready for this, you'll want to:

- Keep your business and personal accounts completely separate

- Make sure you've got a consistent cash flow deposit pattern

- Document the source of any irregular large deposits

- Work with a good accountant to get some expense ratio letters if that makes sense

Different lenders will require 12 months of statements, while others will want to see 24 months - so shop around and find the best terms for your situation.

Credit scores, financial capacity and lender requirements

If you've got a lot of assets but a low credit score because of medical bills, a divorce, or some other circumstance, you're likely to get turned down by conventional lenders even though you've got the money to pay back the loan.

The Solution: Asset-based lenders and larger down payments can fill the gap here. Non-QM lenders will look at your liquid assets investment accounts, retirement funds, and cash reserves to see if they think you're stable enough to take on a loan. A borrower with a credit score of 600 but $2 million in the bank looks like a lower risk than one with a 750 credit score but not much cash in savings.

And for borrowers who are just a little bit short of the minimum credit score requirements, doing some targeted credit repair to focus on the high-impact factors like utilization rate, late payments and credit report errors - can get you another 20-50 points on your credit score within 3-6 months.

The higher costs of non-QM loans

Non-QM loans do come with a higher rate and bigger fees, which can raise some legitimate concerns about affordability, especially over a long loan term.

The Solution: Think of non-QM as a short-term solution rather than a long-term one. Many borrowers use non-QM loans to purchase property and then refinance to a conventional loan after a couple of years when they've got more established income and credit. You'll need to have:

- A couple of years of steady monthly payments

- A more stable income that can be documented

- Some improvements in your credit score

- Some equity built up in the property

If you shop around, you'll see that there's a big difference in rates between different private lenders, banks, and credit unions - some spreads can be as much as 0.5% or more. So get quotes from at least three lenders before you commit to anything.

Do the maths on whether or not a non-QM loan makes sense for you if you can purchase property that's going up in value 5% a year while you'd otherwise be renting, the higher rate might be worth paying.

Summary

The right loan choice for you will depend on whether you're able to document your income and whether or not you're willing to pay a bit more for the flexibility of a non-QM loan agreement. Conventional mortgages are the lowest-cost option and they come with the strongest protections for borrowers who fit the standard income profile. Non-QM loans on the other hand unlock homeownership for self-employed people, investors and other borrowers who don't fit the W-2 mould.

Here's what to do next:

- Be honest with yourself about your documentation capabilities how likely are you to be able to produce two years of consistent W-2s and tax returns?

- Check your credit score and credit report through AnnualCreditReport.com so you can see where you're at

- Work out your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income

- Get quotes from a few different mortgage lenders, including credit unions - both conventional and non-QM - to see how the rates and fees compare

- Consult with a mortgage pro who specialises in your type of situation before you start applying for loans

Some other topics worth exploring include strategies for getting out of a non-QM loan and into a conventional one, credit repair and how long it takes to get your credit score sorted, and FHA loans backed by the Federal Housing Administration as an alternative for borrowers who've got credit issues but can still document their income.

Frequently Asked Questions

Can I qualify for both and choose?

Yes - if you meet the conventional documentation requirements. If you qualify for both, you should probably go with the conventional loan; it has lower interest rates, lower fees, and better borrower protections. The only exception is if you're an investor looking to keep your conventional loan slots open while using DSCR products for investment properties.

What credit score do I need for each?

Both types generally require a minimum credit score of 620, but conventional loans will give you the best rates if you can manage a score of 740 or better. Non-QM lenders will be a bit more flexible and might approve scores in the 580-619 range if you've got a big down payment and some reserves.

How much more do non-QM loans cost compared to conventional?

Expect to pay 0.25-1% more in interest, which on a typical loan will mean an extra $200-500 a month. Closing costs can be 3-8 thousand dollars higher, and down payments can be as high as 28%, as opposed to 3-20% for conventional, which adds up to a lot more cash upfront.

Can I refinance from non-QM to conventional later?

Yes, that's a pretty common strategy. After a couple of years of steady monthly payments and potentially some improvements on your documentation or credit, you can refinance to a conventional loan and get a lower rate. Think about this when you're doing the maths on whether or not a non-QM loan makes sense for you.

What kind of documentation do you need to get approved for a loan agreement?

Conventional loans want to see your W-2s, your last two years of tax returns, pay stubs, bank statements, and proof that you actually work for the people who say you work for them. Non-QM loans can be a bit more flexible - but only just - and the paperwork needed can vary depending on what kind of non-qualified mortgage loan you're going for.

Bank statement loans will want 12 to 24 months of records showing your deposits going in, for instance. Asset depletion loans need to see what you're doing with your investments, and DSCR loans are really all about showing that the property will bring in enough money to cover the mortgage, so they want to see all your leases and rental history.

How long will it take to get through underwriting for each loan?

Conventional loans usually take at least a month and a half to two months from the time you submit your application to closing. Non-QM loans can potentially close faster, sometimes in as little as 3-4 weeks, because verifying your bank statements is a lot easier than digging deep into your tax returns. But it's worth noting that complicated cases in either category can really drag out the whole process.