Markets have a funny way of testing conviction. One day a stock drops double digits on a headline; the next it claws its way back as if nothing happened. The question for investors isn’t what caused the drop; it’s whether that event changed the long-term story. If it didn’t, then the selloff may have been an opportunity in disguise. That’s precisely the situation with AST SpaceMobile (ASTS) today. Was the recent stumble a warning sign—or just noise?

A Volatile Year but Still Beating Expectations

Let’s start with the numbers. According to Barchart data, AST SpaceMobile has delivered a strong performance in 2026 despite recent volatility. Year to date (YTD), ASTS stock has outpaced the broader S&P 500 ($SPX), even after its mid-April dip. Its stock is up 17% versus a 4.1% gain.

That drop came when Blue Origin failed to place the BlueBird 7 satellite into its intended orbit—sending ASTS shares down 15% in a single session. But here’s what matters: the recovery.

- ASTS closed yesterday at $80.01, nearly reclaiming all losses.

- Shares are up 4.5% in premarket trading, putting them within 3.6% of pre-drop levels.

That’s not a market losing faith. That’s a market recalibrating.

Surprisingly, this rebound happened alongside a much bigger development—one that changes the long-term equation.

The FCC Approval That Changes Everything

Let’s get to the real story. AST SpaceMobile announced that the Federal Communications Commission (FCC) has granted full commercial approval for its planned 248-satellite constellation. That’s not incremental progress—that’s a regulatory green light for the entire business model.

Here’s why that matters. Direct-to-device (D2D) satellite communication—connecting everyday smartphones directly to satellites—has been more theory than reality. Now, it’s becoming operational. And only two companies currently have full Supplemental Coverage from Space (SCS) approval:

- SpaceX

- AST SpaceMobile

That’s it. That’s a fancy way of saying ASTS just built a regulatory moat. Competitors can’t simply launch satellites and compete. They need approval, spectrum coordination, and compliance. That takes years. Blue Origin has filed a request with the FCC to launch and operate a network, but SpaceX has filed an objection to it.

Granted, ASTS itself still needs to execute: launch satellites, scale capacity, and generate revenue. But regulatory risk? That hurdle just got cleared.

ASTS Is Expensive but Not Without Reason

Let’s talk valuation, because this is where investors need to stay grounded.

According to Barchart’s “Ratios” section, AST SpaceMobile trades at elevated multiples—largely because it is still pre-revenue at scale. Traditional metrics like P/E don’t apply cleanly yet. But it goes for 460.13 sales and 13.40x book. That said, investors are valuing ASTS on future cash flows tied to its constellation.

Compare that to peers:

| Company | Business Model | Profitability | Market Position |

| AST SpaceMobile | Direct-to-device satellite | Pre-profit | Early leader |

| SpaceX | Launch + Starlink broadband | Private (for now) | Dominant scale |

| Legacy telecoms | Ground networks | Profitable | Mature |

In short, ASTS is priced as a future infrastructure provider, not a current earnings machine.

That comes with risk. If deployment delays stretch or capital needs rise, valuation could compress. But if execution stays on track, today’s price reflects early positioning in a potentially massive market.

What Analysts Think About ASTS Stock

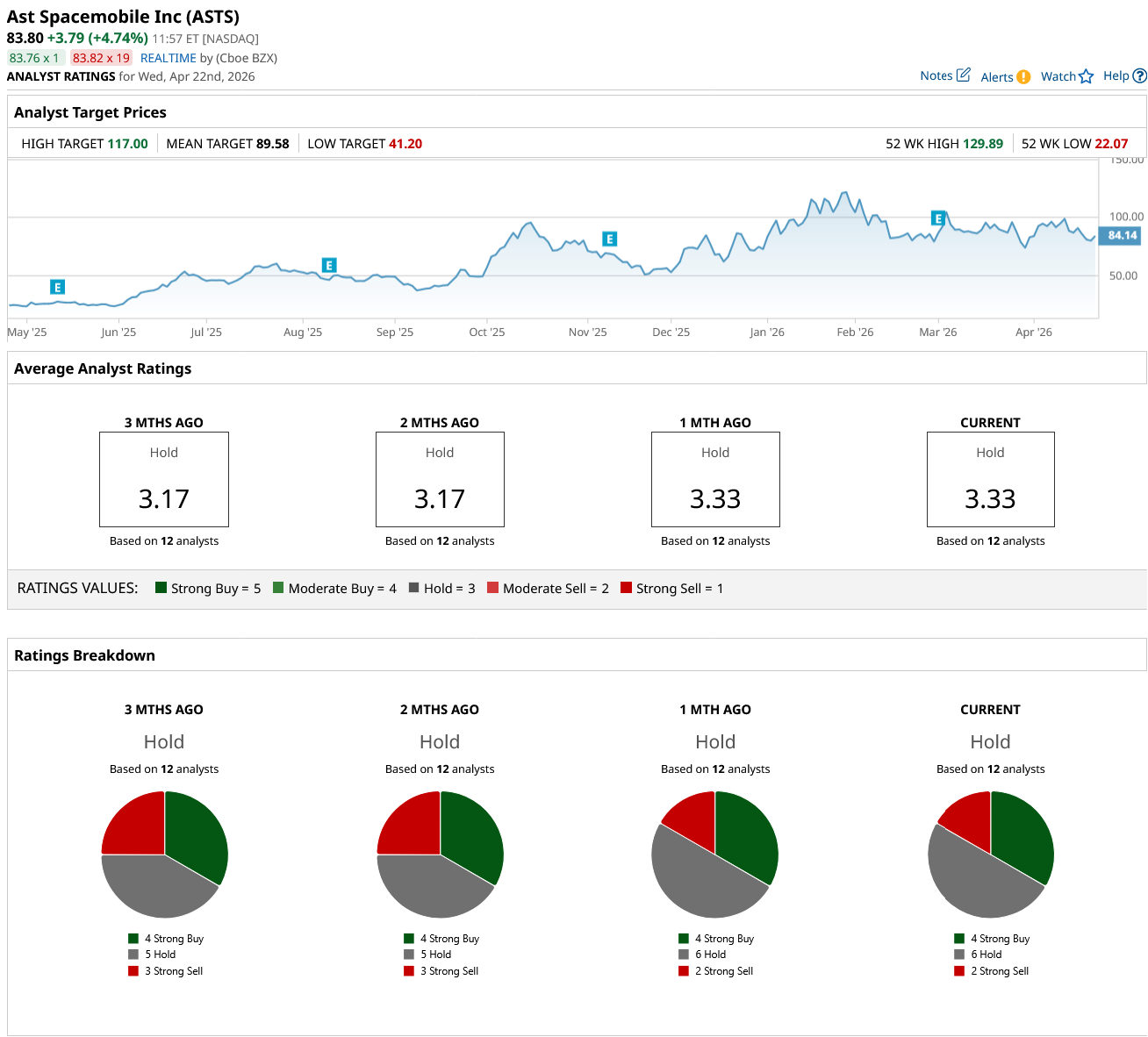

Let’s bring in Wall Street. Based on analyst data from Barchart, analysts have a mean price target of $89.58, implying 11.96% upside potential from Tuesday's $80.01 closing price. Targets range from a low of $41.20 to a high of $117, or 46% upside potential. That spread tells you everything you need to know—this is a high-conviction, high-uncertainty stock.

Analysts have a consensus "Hold" on ASTS based on 12 analyst ratings. There are four "Strong Buy" ratings, six "Hold," and two "Strong Sell."

Wall Street's analysts aren’t debating whether the opportunity exists. They’re debating how well AST SpaceMobile captures it.

Bottom Line

The BlueBird 7 mishap made headlines but didn’t break the business. Satellite deployment always carries risk: delays, misfires, and adjustments are part of the process. What matters is whether those events derail the broader trajectory. In this case, they didn’t. It said more about Blue Origin than it did about ASTS.

Meanwhile, the FCC approval quietly did something far more important: it validated ASTS’s long-term path and narrowed the competitive field to essentially two players. In short, this wasn’t a setback—it was a reminder.

Investors who sold on the drop reacted to an event. Investors who bought the dip focused on the trajectory. That said, this isn’t a risk-free story. Execution still matters. Capital needs are real. And timelines can shift. But regardless of how you look at it, AST SpaceMobile now has:

- Regulatory approval

- A defined deployment roadmap

- A near-duopoly position in D2D

When all is said and done, those are the factors that drive long-term returns, not a single launch anomaly. For investors willing to tolerate volatility, the lesson here is simple: don’t bet against a company whose core thesis just got stronger.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- 17 Unusually Active Call Options: Buy 3 for Under $300 and Big Potential Profits

- Honeywell Just Announced That Its Quantinuum Unit Filed for an IPO. How Should You Play HON Stock Here?

- UnitedHealth Is Back! But Should You 'Long-Term Care' About UNH Stock?

- Capital Group Is Doubling Down on MicroStrategy. Should You Buy MSTR Stock Here Too?