Wrapping up Q2 earnings, we look at the numbers and key takeaways for the household products stocks, including Kimberly-Clark (NASDAQ: KMB) and its peers.

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

The 10 household products stocks we track reported a mixed Q2. As a group, revenues missed analysts’ consensus estimates by 0.6% while next quarter’s revenue guidance was 0.7% below.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

Kimberly-Clark (NASDAQ: KMB)

Originally founded as a Wisconsin paper mill in 1872, Kimberly-Clark (NYSE: KMB) is now a household products powerhouse known for personal care and tissue products.

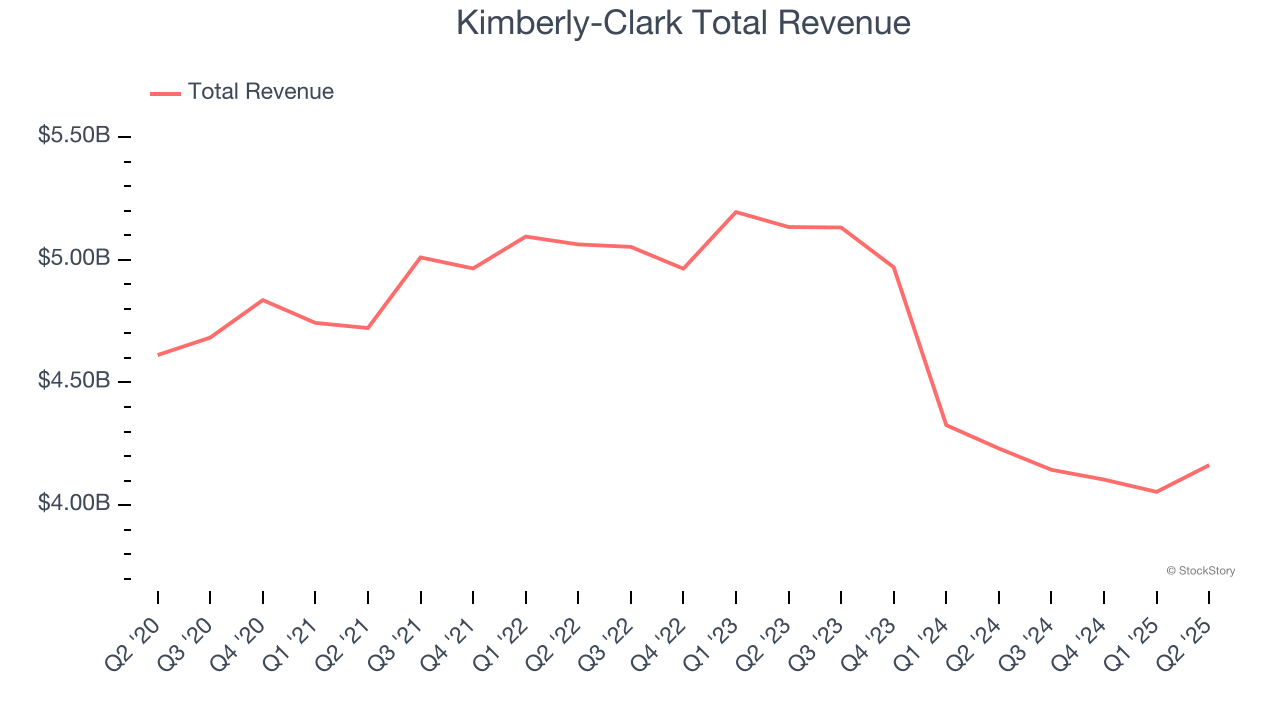

Kimberly-Clark reported revenues of $4.16 billion, down 1.6% year on year. This print fell short of analysts’ expectations by 9.6%. Overall, it was a mixed quarter for the company with an impressive beat of analysts’ EBITDA estimates but a miss of analysts’ gross margin estimates.

Kimberly-Clark delivered the weakest performance against analyst estimates of the whole group. The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $125.20.

Is now the time to buy Kimberly-Clark? Access our full analysis of the earnings results here, it’s free.

Best Q2: Clorox (NYSE: CLX)

Founded in 1913 with bleach as the sole product offering, Clorox (NYSE: CLX) today is a consumer products giant whose product portfolio spans everything from bleach to skincare to salad dressing to kitty litter.

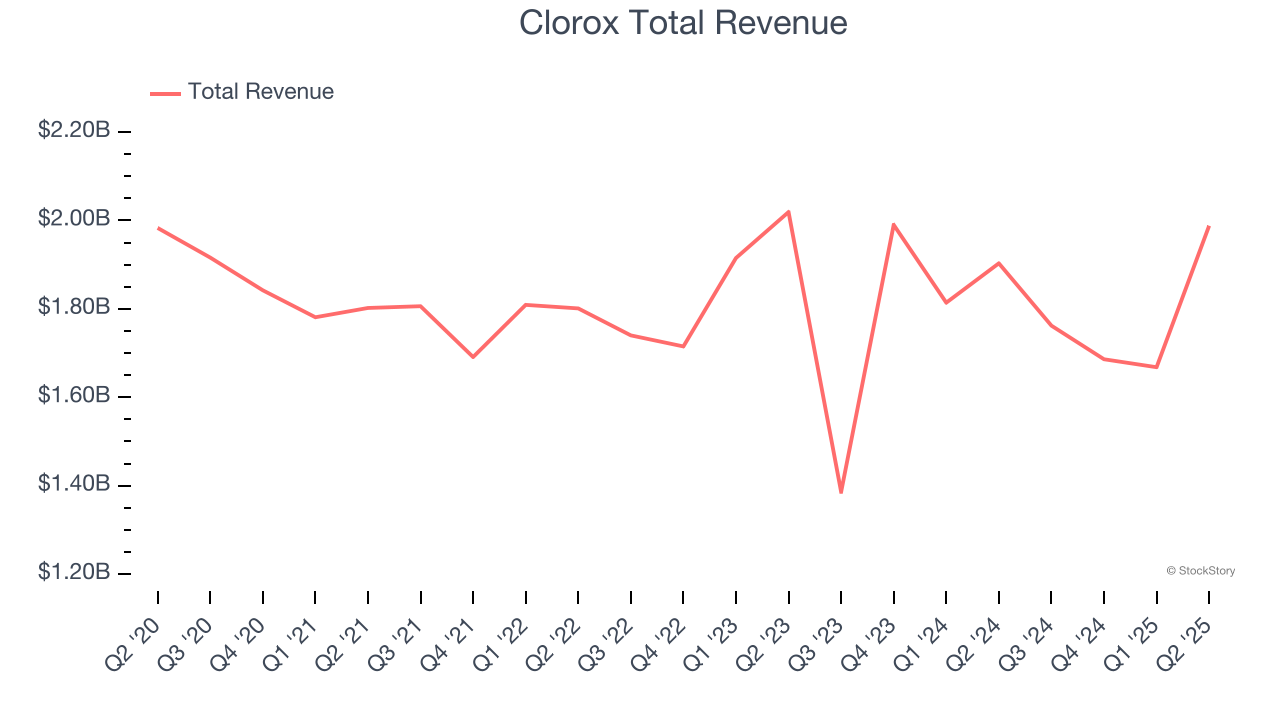

Clorox reported revenues of $1.99 billion, up 4.5% year on year, outperforming analysts’ expectations by 3.3%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA and organic revenue estimates.

Clorox scored the fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.1% since reporting. It currently trades at $120.15.

Is now the time to buy Clorox? Access our full analysis of the earnings results here, it’s free.

Slowest Q2: Spectrum Brands (NYSE: SPB)

A leader in multiple consumer product categories, Spectrum Brands (NYSE: SPB) is a diversified company with a portfolio of trusted brands spanning home appliances, garden care, personal care, and pet care.

Spectrum Brands reported revenues of $699.6 million, down 10.2% year on year, falling short of analysts’ expectations by 5.5%. It was a disappointing quarter as it posted a significant miss of analysts’ organic revenue and EBITDA estimates.

Spectrum Brands delivered the slowest revenue growth in the group. As expected, the stock is down 1.8% since the results and currently trades at $52.

Read our full analysis of Spectrum Brands’s results here.

Procter & Gamble (NYSE: PG)

Founded by candle maker William Procter and soap maker James Gamble, Proctor & Gamble (NYSE: PG) is a consumer products behemoth whose product portfolio spans everything from facial tissues to laundry detergent to feminine care to men’s grooming.

Procter & Gamble reported revenues of $20.89 billion, up 1.7% year on year. This result was in line with analysts’ expectations. More broadly, it was a satisfactory quarter as it also produced an impressive beat of analysts’ EBITDA estimates but a slight miss of analysts’ gross margin estimates.

The stock is down 2.3% since reporting and currently trades at $153.39.

Read our full, actionable report on Procter & Gamble here, it’s free.

Central Garden & Pet (NASDAQ: CENT)

Enhancing the lives of both pets and homeowners, Central Garden & Pet (NASDAQ: CENT) is a leading producer and distributor of essential products for pet care, lawn and garden maintenance, and pest control.

Central Garden & Pet reported revenues of $960.9 million, down 3.6% year on year. This print missed analysts’ expectations by 2.1%. Aside from that, it was a satisfactory quarter as it recorded a solid beat of analysts’ EBITDA estimates.

The stock is down 13.9% since reporting and currently trades at $33.96.

Read our full, actionable report on Central Garden & Pet here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.