Looking back on sales software stocks’ Q2 earnings, we examine this quarter’s best and worst performers, including ZoomInfo (NASDAQ: GTM) and its peers.

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

The 4 sales software stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 2.6% while next quarter’s revenue guidance was in line.

While some sales software stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.7% since the latest earnings results.

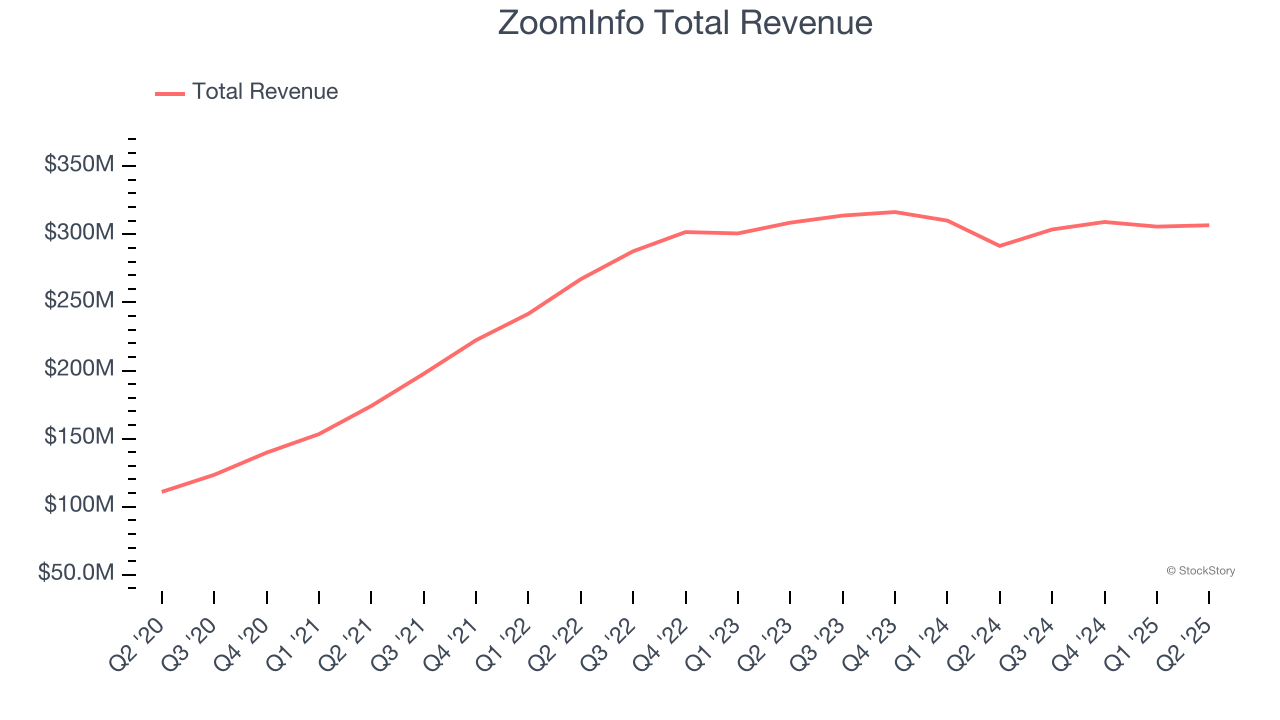

ZoomInfo (NASDAQ: GTM)

Operating a platform it calls "RevOS" - short for Revenue Operating System - ZoomInfo (NASDAQ: GTM) provides sales, marketing, and recruiting teams with business intelligence and analytics to identify prospects and deliver targeted outreach.

ZoomInfo reported revenues of $306.7 million, up 5.2% year on year. This print exceeded analysts’ expectations by 3.5%. Overall, it was a satisfactory quarter for the company with accelerating growth in large customers but EPS guidance for next quarter missing analysts’ expectations.

“We continued to deliver on our AI and data focused innovation roadmap resulting in another quarter of strong financial results,” said Henry Schuck, ZoomInfo Founder and CEO.

ZoomInfo scored the biggest analyst estimates beat but had the slowest revenue growth of the whole group. The company added 16 enterprise customers paying more than $100,000 annually to reach a total of 1,884. Even though it had a relatively good quarter, the market seems discontent with the results. The stock is down 6% since reporting and currently trades at $11.38.

Is now the time to buy ZoomInfo? Access our full analysis of the earnings results here, it’s free.

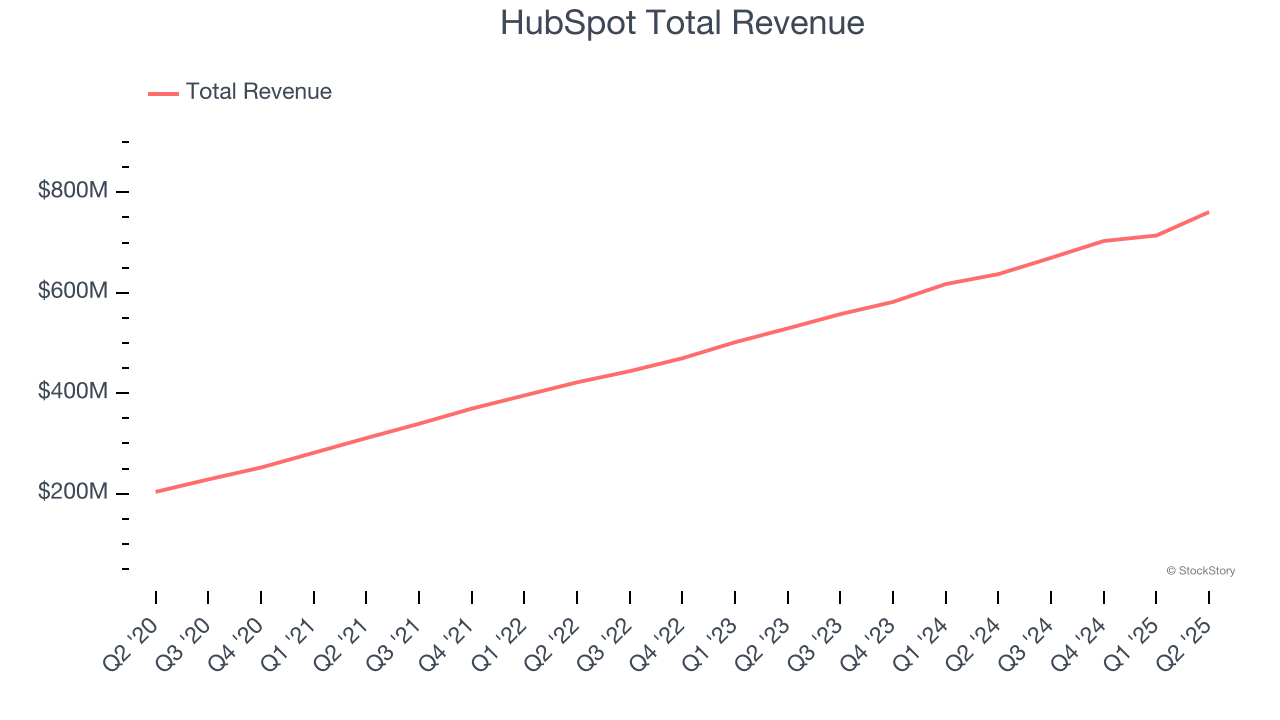

Best Q2: HubSpot (NYSE: HUBS)

Born from the idea that traditional interruptive marketing was becoming less effective, HubSpot (NYSE: HUBS) provides an integrated platform that helps businesses attract, engage, and manage customer relationships through marketing, sales, service, and content management tools.

HubSpot reported revenues of $760.9 million, up 19.4% year on year, outperforming analysts’ expectations by 2.9%. The business had a strong quarter with a solid beat of analysts’ billings and EBITDA estimates.

HubSpot achieved the fastest revenue growth and highest full-year guidance raise among its peers. The company added 9,724 customers to reach a total of 267,982. The market seems happy with the results as the stock is up 6% since reporting. It currently trades at $519.80.

Is now the time to buy HubSpot? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Salesforce (NYSE: CRM)

With its cloud-based platform named after its stock ticker symbol CRM (Customer Relationship Management), Salesforce (NYSE: CRM) provides customer relationship management software that helps businesses connect with their customers across sales, service, marketing, and commerce.

Salesforce reported revenues of $10.24 billion, up 9.8% year on year, exceeding analysts’ expectations by 1%. Still, it was a mixed quarter as it posted a miss of analysts’ billings estimates.

Salesforce delivered the weakest performance against analyst estimates and weakest full-year guidance update in the group. As expected, the stock is down 4.5% since the results and currently trades at $244.99.

Read our full analysis of Salesforce’s results here.

Freshworks (NASDAQ: FRSH)

Starting as a customer service solution before expanding into a comprehensive software suite, Freshworks (NASDAQ: FRSH) provides AI-powered software-as-a-service solutions that help companies manage customer service, IT support, sales, and marketing functions.

Freshworks reported revenues of $204.7 million, up 17.5% year on year. This result beat analysts’ expectations by 2.9%. Overall, it was a strong quarter as it also produced an impressive beat of analysts’ EBITDA estimates and EPS guidance for next quarter beating analysts’ expectations.

The company added 700 enterprise customers paying more than $5,000 annually to reach a total of 23,975. The stock is down 9.8% since reporting and currently trades at $12.55.

Read our full, actionable report on Freshworks here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.