Rocket Lab (RKLB) saw RKLB stock drop more than 11% on March 18 after announcing plans for a $1 billion stock sale, reigniting fears of additional dilution following the completion of a $749 million equity sale under a prior at-the-market facility. However, the selloff was quickly followed by a major new contract win: a $190 million U.S. Department of War agreement for 20 hypersonic test flights using its HASTE launch vehicle. This marks the single-largest launch contract in the company’s history and catapults its total backlog across launch services and space systems past the $2 billion mark.

While dilution concerns are undeniably real for shareholders, Rocket Lab's rapidly expanding business momentum and record backlog raise a key question. Is the growth trajectory still worth the risk?

Dilution Risks Loom Large

The fresh $1 billion equity distribution agreement allows Rocket Lab to sell shares opportunistically over time, providing flexibility to fund ambitious projects like the medium-lift Neutron rocket and expanded space systems production. However, after exhausting nearly $749 million from the previous facility, investors worry about repeated share issuance eroding ownership stakes and pressuring the RKLB stock price.

With the company still pre-profit and burning cash on Neutron development — recently delayed but critical for scaling beyond the small-sat-focused Electron — dilution appears baked into the growth story. Short-term holders felt the sting immediately, as the announcement reversed prior gains and highlighted ongoing capital needs in a high-cost industry.

RKLB stock is down 4% year-to-date (YTD), but shares are still up 260% over the past year as the business has grown.

Rocket Lab's Defense Business Gains Momentum

The $190 million HASTE contract represents a significant expansion into defense, shifting Rocket Lab beyond its traditional commercial roots. HASTE, a modified Electron variant capable of accelerating payloads past Mach 5, will support the Multi-Service Advanced Capability Hypersonic Test Bed (MACH-TB) 2.0 program over four years. This block buy brings the launch backlog above 70 missions and underscores growing U.S. government reliance on commercial providers for rapid hypersonic testing, an area where traditional infrastructure has lagged.

While most of Rocket Lab's revenue — a record $602 million in 2025 — still stems from frequent commercial Electron launches and space systems contracts (including satellite components and constellations), defense wins like this and the recent $816 million Space Development Agency satellite order signal a pivotal diversification. These contracts could become a key growth driver, offering higher margins and long-term visibility as national security priorities accelerate.

Execution and Funding Risks Temper Optimism

The defense pivot isn’t without hurdles, however. Executing 20 HASTE missions demands flawless reliability; Rocket Lab boasts an impressive launch cadence and near-perfect recent success rate with Electron, but scaling hypersonic tests introduces new technical and regulatory complexities. Government funding priorities add another layer of uncertainty — budgets for hypersonics could shift with political changes, sequestration, or competing programs.

The backlog provides revenue visibility (roughly $685 million expected to convert in the next 12 months pre-contract), yet converting it depends on timely launches and customer payments. Meanwhile, dilution funds Neutron, which promises to unlock medium-lift markets and compete more directly with SpaceX, but any further delays could amplify cash burn and investor skepticism.

With RKLB stock trading at 61.6 times sales, it is premium priced for the growth story, meaning any shocks — like dilutive share sales — will cause shares to pull back.

What Does Wall Street Think of Rocket Lab Stock?

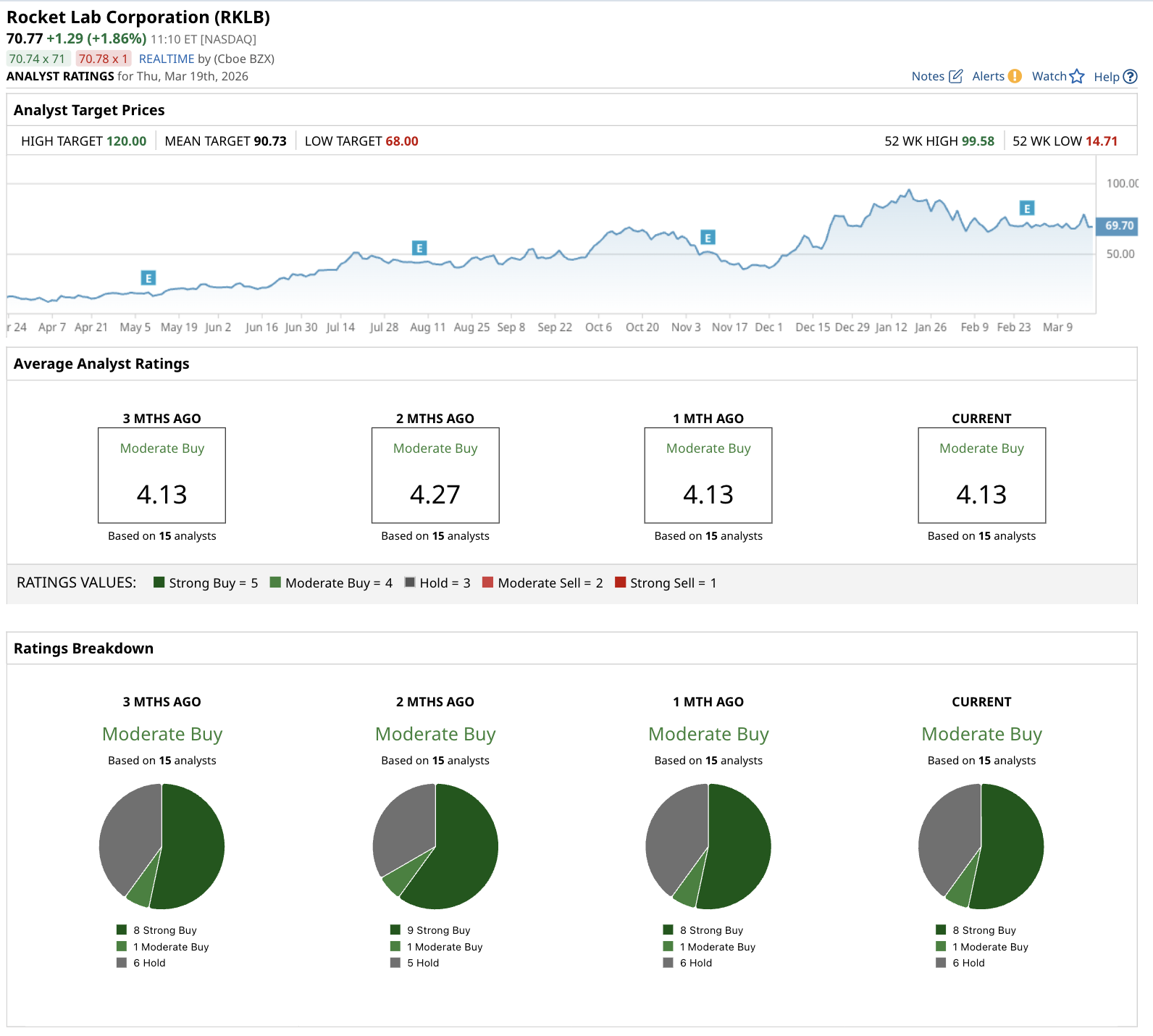

Wall Street has a “Moderate Buy” consensus rating on RKLB stock based on 15 analysts with coverage. This consensus breaks down to eight "Strong Buy" ratings, one "Moderate Buy," and six "Hold" ratings. No analysts tracked by Barchart suggest selling shares, while the mean price target of $90.73 implies roughly 35% potential upside from current levels.

The sentiment, though, has weakened slightly over the past two months. Where Cantor Fitzgerald recently reiterated its “Overweight” rating, Needham maintained a "Buy" rating but lowered its price target from $110 to $95. However, the Street-high target price stands at $120.

The Bottom Line

Rocket Lab’s $2 billion backlog delivers tangible proof of demand and positions the company as a diversified space leader, with defense contracts increasingly offsetting reliance on commercial launches. This growth narrative partially offsets dilution risks by promising future revenue scale that could support profitability and higher valuations as Neutron comes online.

However, persistent capital raises and execution/funding uncertainties mean shareholders must tolerate volatility. For risk-tolerant long-term investors who believe in Rocket Lab’s vertical integration and hypersonic edge, RKLB stock remains a compelling buy at current levels — backlog momentum outweighs the dilution drag. Conservative buyers may prefer waiting for clearer Neutron progress or reduced offering activity.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart