Just days after Advanced Micro Devices (AMD) delivered a blockbuster first-quarter 2026 earnings report, the semiconductor industry is experiencing a major shift. On May 5, AMD posted revenue of $10.3 billion, up 38% year-over-year (YOY), beating consensus estimates of around $9.9 billion. But what especially caught investors' attention was the Q2 guidance of approximately $11.2 billion and management's sharply upgraded outlook for the server CPU market, which is now expected to exceed $120 billion by 2030 with annual growth above 35%.

This comes as analysts note resurging excitement around CPUs, pointing to AMD's results as validation of a trend that bodes well for Intel (INTC). Both Intel and AMD are now raising CPU prices by 10% to 15% (or more) as tight supply meets surging demand in server and client segments.

Intel, the longtime CPU market leader, brings some serious advantages to this moment with its larger manufacturing scale, established customer base, advancing foundry capabilities, and strong U.S. government backing. Could Intel actually turn out to be the biggest winner from the CPU resurgence that its rival just validated? Let's take a closer look.

Intel's Remarkable Turnaround Story

Headquartered in Santa Clara, California, Intel designs and manufactures semiconductors, including microprocessors, chipsets, and integrated circuits for data centers, personal computers, and AI applications.

INTC stock has delivered exceptional returns, now trading around the $124 malr with year-to-date (YTD) gains of 239% and a 52-week surge of 495%.

Intel now commands a market capitalization of $550 billion, although its forward price-to-earnings (P/E) ratio of 180.7 times sits well above the sector median. The price-to-cash flow multiple of 50.4 times also exceeds the sector average.

Intel reported Q1 2026 earnings on April 23. The report backed up the optimism driving shares higher. For the period, Intel delivered revenue of $13.58 billion versus analyst estimates of $12.39 billion, marking 7% YOY growth and a 9.6% beat.

Adjusted EPS of $0.29 blew past analyst expectations of $0.01. Intel's adjusted operating income hit $1.67 billion compared to analyst estimates of $397.4 million, achieving a 12.3% margin that beat expectations and showed improving profitability in its core business.

The quarter did have its challenges, as Intel's GAAP operating margin came in at -23.1%, down from -2.4% in the same quarter last year. Free cash flow also stayed negative at -$2.02 billion, although this was better than the -$3.68 billion from the prior-year period.

Intel's Strategic CPU Wins

Intel has locked down several major partnerships that support the CPU-focused AI infrastructure story. On April 9, Intel and Alphabet's (GOOGL) Google announced a multiyear deal to advance AI and cloud infrastructure, with Google Cloud committing to deploy multiple generations of Intel Xeon processors across its global infrastructure.

Google Cloud is deploying Intel Xeon processors across workload-optimized instances, including the latest Xeon 6 processors powering C4 and N4 instances for AI training coordination, latency-sensitive inference, and general-purpose computing. Intel CEO Lip-Bu Tan noted that "scaling AI requires more than accelerators — it requires balanced systems" where CPUs and IPUs deliver the performance modern AI workloads need.

Even bigger was the news that Elon Musk has tapped Intel's 14A process technology for a major project. Tesla (TSLA), SpaceX, and xAI plan to use Intel's next-generation 14A manufacturing process for Terafab, an AI semiconductor manufacturing initiative.

Apple (AAPL) added more validation on May 5 when reports emerged that the tech giant is exploring Intel's foundry services for domestic chip manufacturing. This potential partnership could reshape Intel's future, given that Apple previously dropped Intel processors entirely for its own Apple Silicon, manufactured exclusively by Taiwan Semiconductor (TSM). Landing Apple as a foundry customer would justify Intel's massive capital investments and create a domestic U.S. supply chain for AI and consumer electronics chips.

Intel also released its Core Series 3 processors on April 16, the company's first entry into the hybrid AI-ready core series segment. These processors deliver AI-ready performance with up to 40 platform trillions of operations per second (TOPS) for small businesses and value-focused buyers.

Wall Street's Measured Optimism

Looking ahead, Intel is scheduled to report Q2 2026 earnings on July 23, with analysts expecting the CPU momentum to keep building. The average earnings estimate for the current quarter ending June 2026 stands at $0.10, a sharp turnaround from the prior year's loss of $0.26. That translates to a YOY growth rate of 138%.

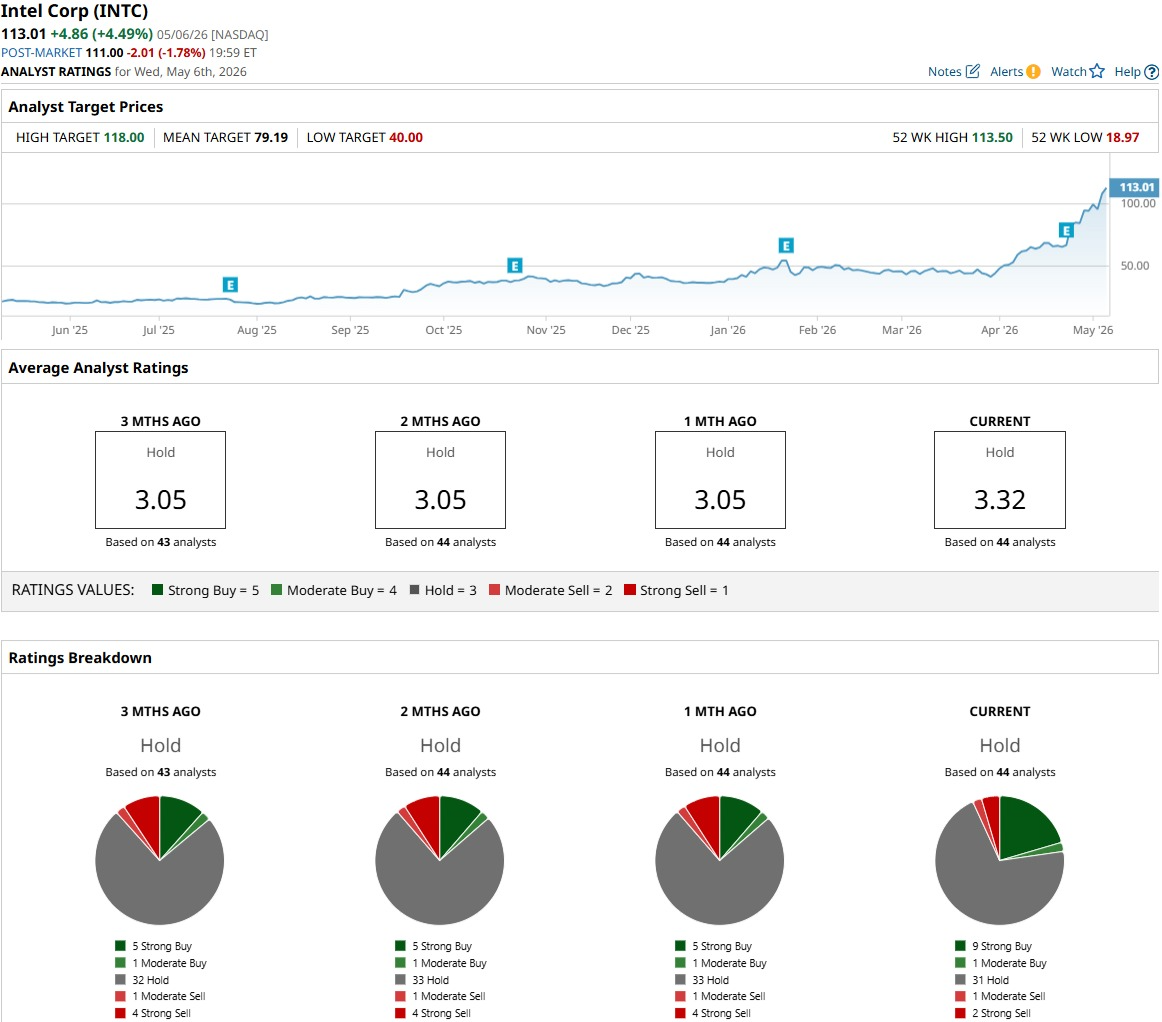

Wall Street has responded to these developments with mixed signals. Evercore analyst Mark Lipacis upgraded Intel to "Outperform" and raised his price target to $111 from $45. Lipacis noted that the market may be underestimating Intel's earnings power a few years out, suggesting the CPU comeback could drive sustained profits beyond current forecasts.

Not all analysts are as bullish, though. Stifel analyst Ruben Roy raised Intel's price target from $42 to $65 but kept a "Hold" rating on INTC stock. This position shows confidence in Intel's recovery path while stopping short of recommending that investors buy more, particularly given Intel's negative free cash flow in Q1 2026.

The broader analyst consensus reflects this push and pull between optimism about the CPU cycle and concerns about valuation. Based on 44 analysts with coverage, the consensus rating sits at “Hold.” The average price target of $79.97 implies potential downside of 36% from current levels.

Conclusion

Intel looks positioned to benefit from the CPU resurgence that AMD's earnings confirmed. INTC stock has already surged 495% over 52 weeks, yet analysts remain cautious with a consensus "Hold" rating and a nearly $80 average price target. Whether shares can justify current valuations depends on Intel executing its manufacturing plans and strategic partnerships. Given strong CPU demand and Intel's capacity advantages, continued momentum seems more likely than a sharp pullback, although some near-term swings wouldn't be surprising at these high valuations.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart