Among Marketbeat’s numerous investor resources are screener pages seeking hard-to-find investments. One of those tools is the screener page for Cheap Dividend Stocks, which is a veritable treasure trove of candidates. It roots out stocks trading within 20% of their 52-week lows that pay 3% or more in yield. Investors can use the list as a starting point for their research and apply other criteria to weed bad from the good. This is a look at the top 5 stocks on the list and whether they are a buy, sell, or hold.

#5 AdvisoryShares Dorsey Wright Short ETF Made the Cut

AdvisoryShares Dorsey Wright Short ETF (NASDAQ: DWSH) made the cut, regarding its trading status and dividend yield, but investors should think twice before buying into this one. This actively managed ETF focused on short strategies has only trended lower since its launch in 2019. It pays a dividend but has made only one payment and is an excellent example of why screener lists of any kind shouldn’t be trusted with blind faith. This is a candidate to sell.

#4 Ambev’s High Yield Trades at Rock Bottom

Ambev’s (NYSE: ABEV) high-yielding stock is trading at rock bottom and is attractive for several reasons. The dividend yields about 10% with shares trading at this level, but there is risk to the payout. The company pays at least 40% of annual adjusted profits, so the distribution can be erratic. The mitigating factor is that the company is expected to pivot back to YOY growth as soon as the current quarter and extend the series of annual distribution increases to three years.

Ambev is a candidate for Dividend Capture Strategies because it pays annually. This means investors may target the stock to buy before the expected dividend announcement and then sell it after the ex-dividend date, capturing the entire yield in the shortest possible time. Seven analysts rate ABEV at Hold and see it advancing at least 15% at the low end of their target range. ABEV is a candidate to Buy.

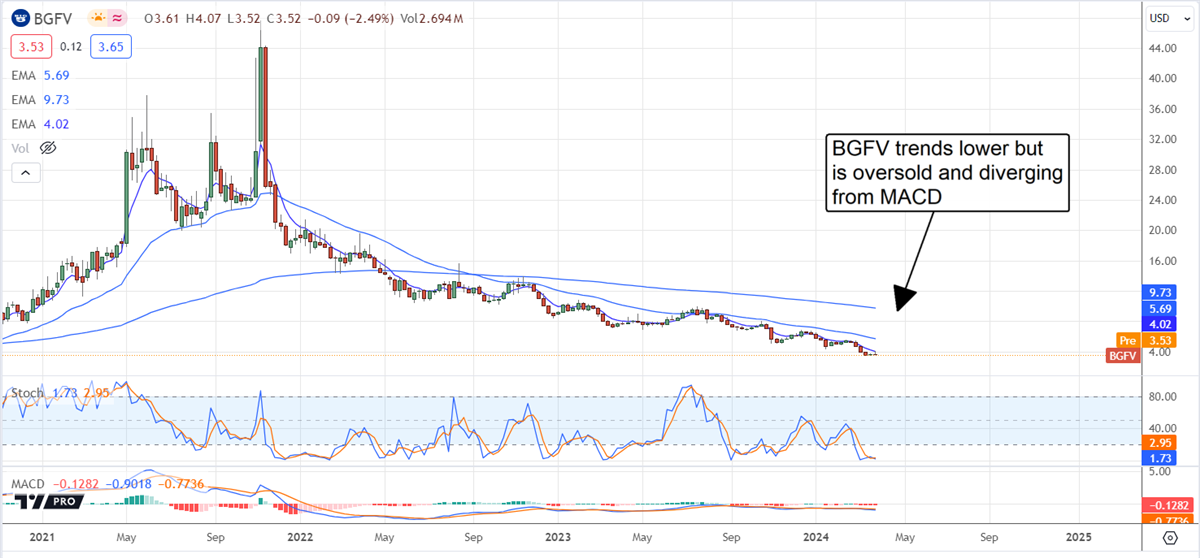

#3 Big 5 Sporting Goods is a Deep Value

Big 5 Sporting Goods (NASDAQ: BGFV) headwinds have left the stock trading at a multi-year low. The low is partly due to a recent distribution cut that shaved more than 50% off the payout. However, the stock yields more than 5% and is a value play for investors. Big 5 should pivot back to growth and sustained profitability by the end of the fiscal year, and the new payout will be reliable until then. The company’s balance sheet is a fortress with no debt and the ability to invest in growth. Big 5 plans to open five new stores this year while closing four as part of its optimization program. One analyst rates BGFV at Hold and sees the stock advancing 170%.

#2 Cullman Bancorp, Inc. Is a Solid Yield For Small Cap Investors

Cullman Bancorp (NASDAQ: CULL) is a small bank in Alabama that pays a safe and reliable 1.2%. The company made a distribution cut in 2021 but can sustain the payment, and today’s outlook includes potential for distribution growth. The payout ratio is less than 20% of cash flow, with deposits and revenue up substantially over the two- and three-year periods. No analysts rate this stock, but institutional activity is interesting. Institutional buying increased last year, and activity was sustained in Q1 2024, led by Vanguard. The institutions own about 25% of the stock and may continue to purchase because shares are near a 13-year low.

#1 Hanover Bancorp: Better Yield and Value For Smallcap Investors

Hanover Bancorp (NASDAQ: HNVR) is a small-cap bank in New York that offers better value and yield than Cullman Bancorp. It trades at less than half the value, near 8X, pays 150 basis points more in yield, and has a similar financial standing and outlook. One analyst tracked by Marketbeat has a rating on this stock. Piper Sandler boosted its target to $21 from $20 in January this year, implying a 40% upside for investors.