Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Ally Financial (NYSE: ALLY) and the best and worst performers in the consumer finance industry.

Consumer finance companies provide loans and credit products to individuals. Growth drivers include increasing consumer spending, financial inclusion initiatives in developing markets, and digital lending platforms reducing distribution costs. Challenges include credit risk during economic downturns, regulatory scrutiny of lending practices, and intensifying competition from traditional banks and fintech firms offering innovative credit solutions.

The 20 consumer finance stocks we track reported a very strong Q3. As a group, revenues beat analysts’ consensus estimates by 3%.

Luckily, consumer finance stocks have performed well with share prices up 10.5% on average since the latest earnings results.

Ally Financial (NYSE: ALLY)

Born from the former GMAC (General Motors Acceptance Corporation) and rebranded in 2010, Ally Financial (NYSE: ALLY) operates a digital-first bank offering auto financing, insurance, mortgage lending, and investment services to consumers and commercial clients.

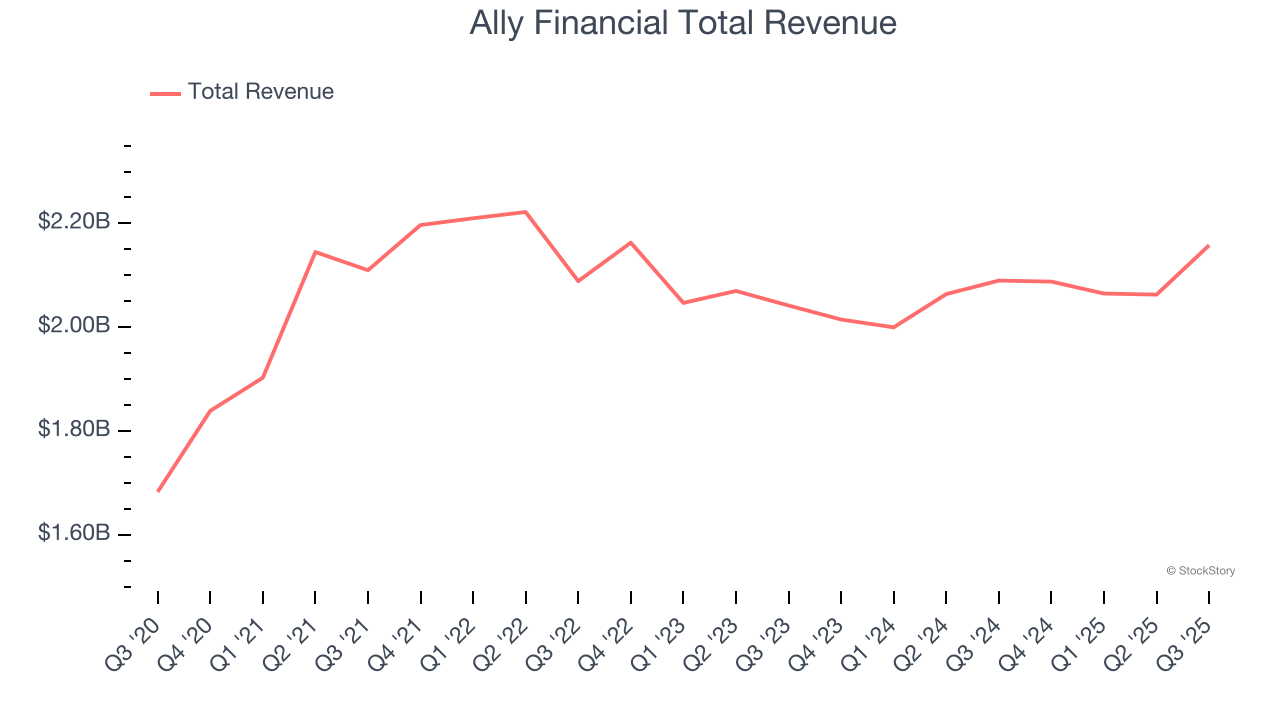

Ally Financial reported revenues of $2.16 billion, up 3.3% year on year. This print exceeded analysts’ expectations by 1.7%. Overall, it was a very strong quarter for the company with a beat of analysts’ EPS estimates and a decent beat of analysts’ revenue estimates.

Interestingly, the stock is up 18.8% since reporting and currently trades at $45.70.

Is now the time to buy Ally Financial? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Nelnet (NYSE: NNI)

Starting as a student loan servicer in the 1970s and evolving through the changing landscape of education finance, Nelnet (NYSE: NNI) provides student loan servicing, education technology, payment processing, and banking services while managing a portfolio of education loans.

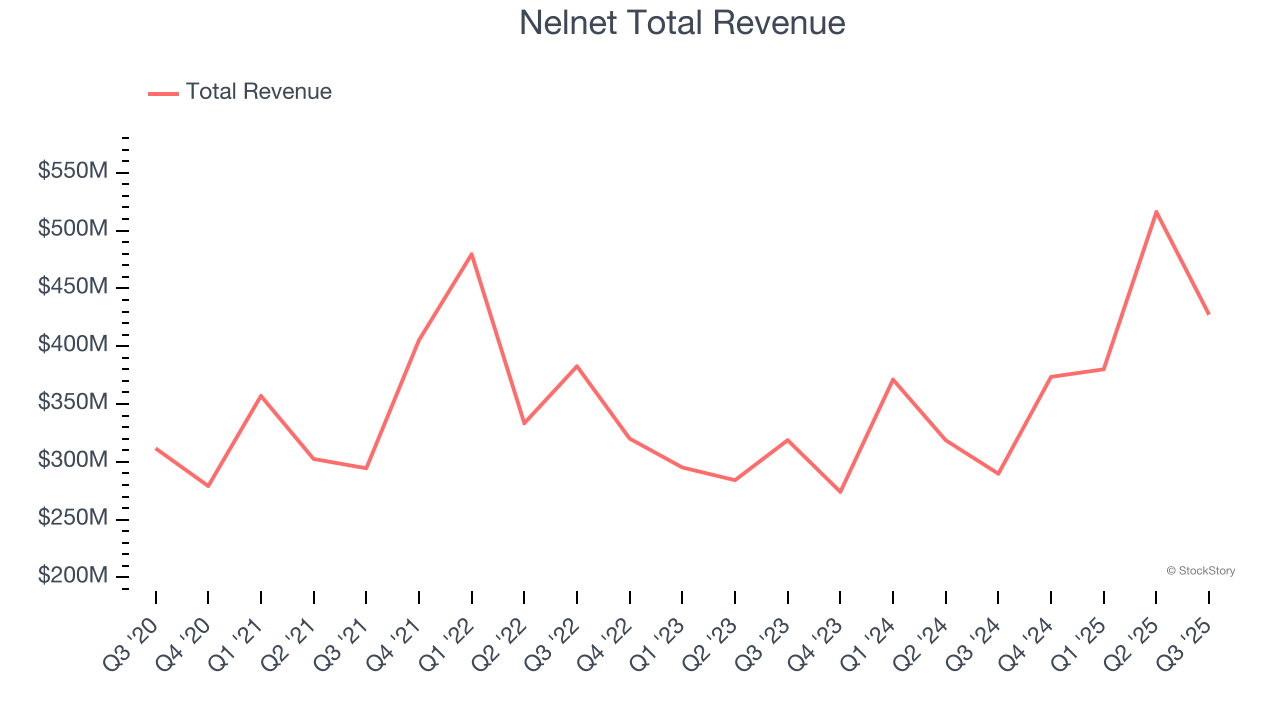

Nelnet reported revenues of $427.4 million, up 47.5% year on year, outperforming analysts’ expectations by 14.9%. The business had an incredible quarter with a beat of analysts’ EPS and revenue estimates.

Nelnet pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 6.7% since reporting. It currently trades at $138.44.

Is now the time to buy Nelnet? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Credit Acceptance (NASDAQ: CACC)

Founded in 1972 by Donald Foss to serve customers overlooked by traditional lenders, Credit Acceptance (NASDAQ: CACC) provides auto financing solutions that enable car dealers to sell vehicles to consumers with limited or impaired credit histories.

Credit Acceptance reported revenues of $405.1 million, up 5.9% year on year, falling short of analysts’ expectations by 19.6%. It was a slower quarter as it posted a significant miss of analysts’ revenue estimates.

Credit Acceptance delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 1.9% since the results and currently trades at $462.05.

Read our full analysis of Credit Acceptance’s results here.

Bread Financial (NYSE: BFH)

Formerly known as Alliance Data Systems until its 2022 rebranding, Bread Financial (NYSE: BFH) provides credit cards, installment loans, and savings products to consumers while powering branded payment solutions for retailers and merchants.

Bread Financial reported revenues of $971 million, down 1.2% year on year. This print was in line with analysts’ expectations. Overall, it was a very strong quarter as it also produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ net interest margin estimates.

The stock is up 24.8% since reporting and currently trades at $75.54.

Read our full, actionable report on Bread Financial here, it’s free for active Edge members.

Mastercard (NYSE: MA)

Recognizable by its iconic "Priceless" advertising campaign that has run in over 120 countries, Mastercard (NYSE: MA) operates a global payments network that connects consumers, financial institutions, merchants, and businesses, enabling electronic transactions and providing payment solutions.

Mastercard reported revenues of $8.60 billion, up 16.7% year on year. This number beat analysts’ expectations by 0.8%. More broadly, it was a mixed quarter as it also logged a decent beat of analysts’ EBITDA estimates but a significant miss of analysts’ transaction volumes estimates.

The stock is up 3.3% since reporting and currently trades at $572.96.

Read our full, actionable report on Mastercard here, it’s free for active Edge members.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.