Eli Lilly currently trades at $1,061 and has been a dream stock for shareholders. It’s returned 541% since December 2020, blowing past the S&P 500’s 85.2% gain. The company has also beaten the index over the past six months as its stock price is up 37.7% thanks to its solid quarterly results.

Is now still a good time to buy LLY? Or are investors being too optimistic? Find out in our full research report, it’s free for active Edge members.

Why Is Eli Lilly a Good Business?

Founded in 1876 by a Civil War veteran and pharmacist frustrated with the poor quality of medicines, Eli Lilly (NYSE: LLY) discovers, develops, and manufactures pharmaceutical products for conditions including diabetes, obesity, cancer, immunological disorders, and neurological diseases.

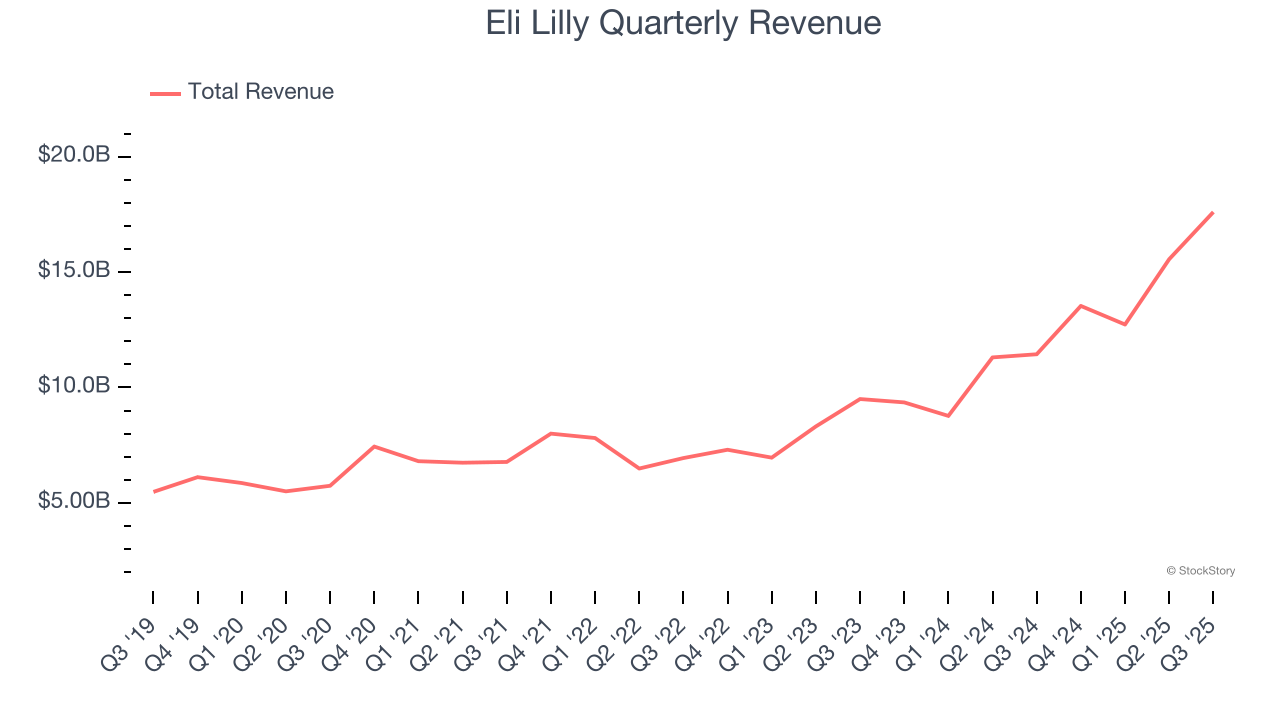

1. Skyrocketing Revenue Shows Strong Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Eli Lilly grew its sales at an impressive 20.7% compounded annual growth rate. Its growth surpassed the average healthcare company and shows its offerings resonate with customers.

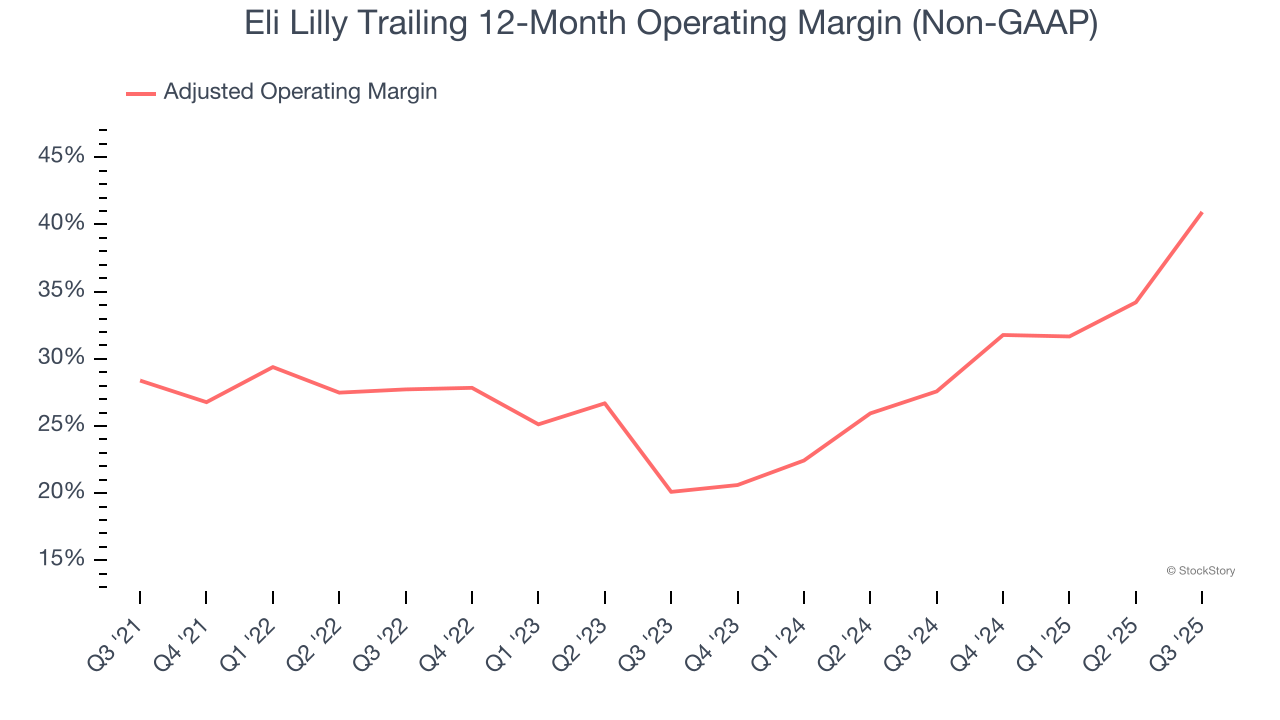

2. Adjusted Operating Margin Rising, Profits Up

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Analyzing the trend in its profitability, Eli Lilly’s adjusted operating margin rose by 20.8 percentage points over the last two years, as its sales growth gave it immense operating leverage. Its adjusted operating margin for the trailing 12 months was 40.9%.

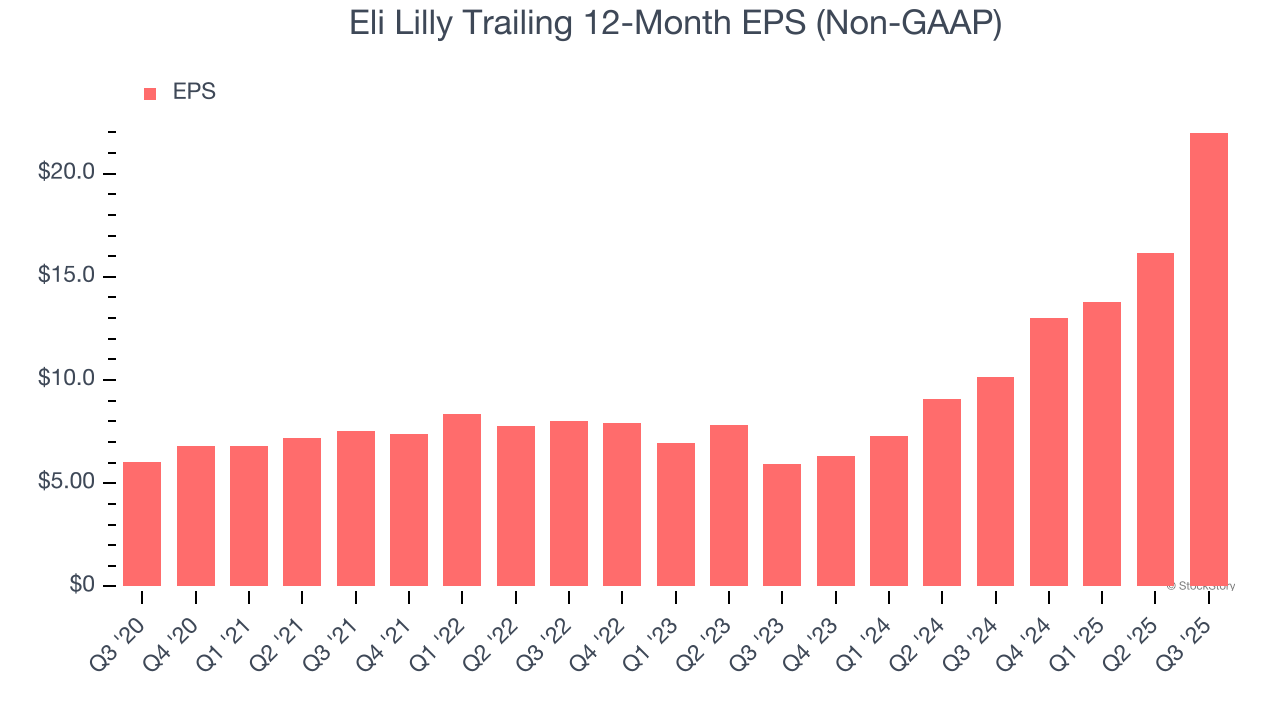

3. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Eli Lilly’s EPS grew at an astounding 29.5% compounded annual growth rate over the last five years, higher than its 20.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why we're bullish on Eli Lilly, and with its shares topping the market in recent months, the stock trades at 34.2× forward P/E (or $1,061 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free for active Edge members.

Stocks We Like Even More Than Eli Lilly

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.