Commvault trades at $192.75 and has moved in lockstep with the market. Its shares have returned 13.9% over the last six months while the S&P 500 has gained 15.5%.

Is now the time to buy Commvault, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Commvault Not Exciting?

We're cautious about Commvault. Here are three reasons we avoid CVLT and a stock we'd rather own.

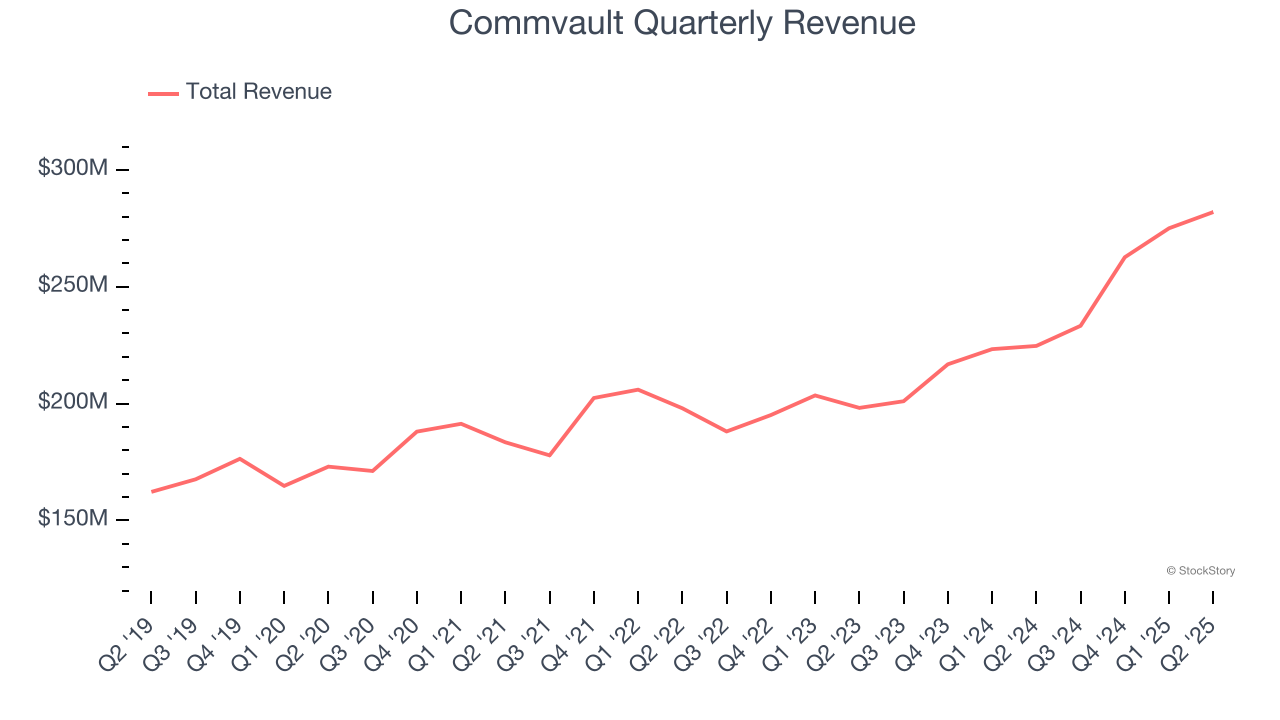

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Commvault grew its sales at a sluggish 9.1% compounded annual growth rate. This fell short of our benchmark for the software sector.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Commvault’s revenue to rise by 13.2%, a slight deceleration versus its 9.1% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

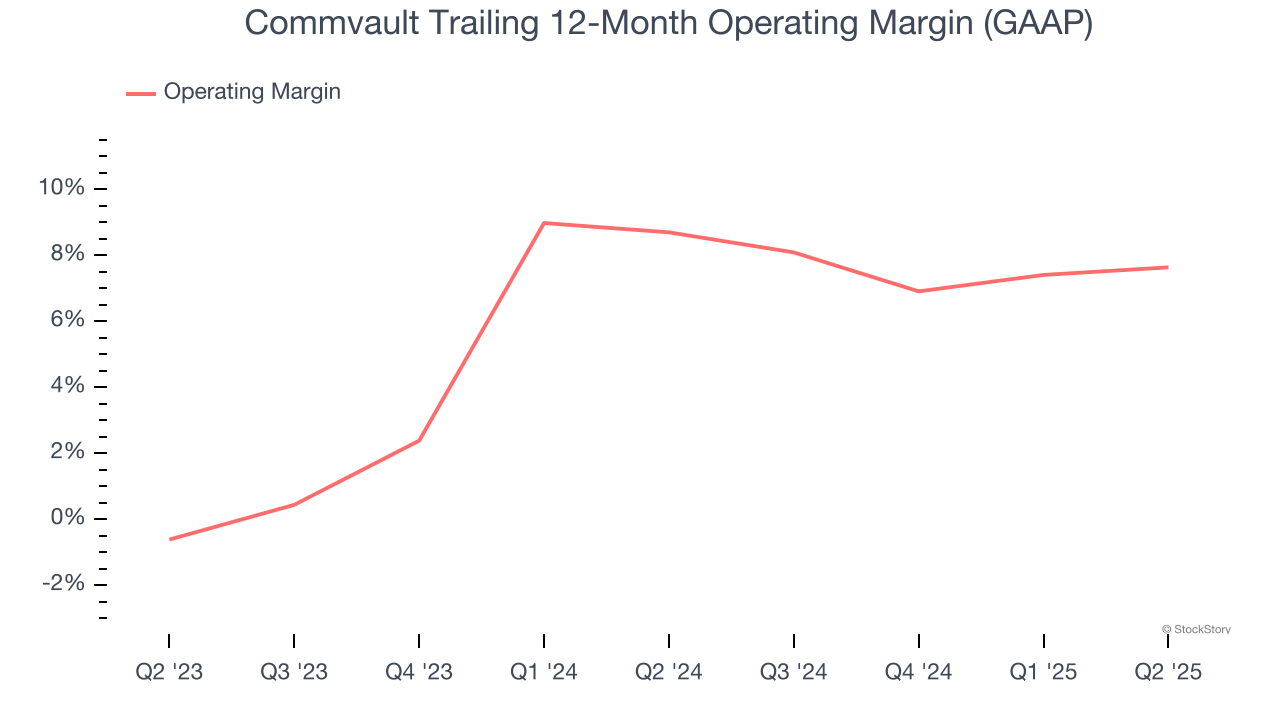

3. Shrinking Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Looking at the trend in its profitability, Commvault’s operating margin decreased by 1.1 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 7.6%.

Final Judgment

Commvault isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 7.3× forward price-to-sales (or $192.75 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Commvault

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.