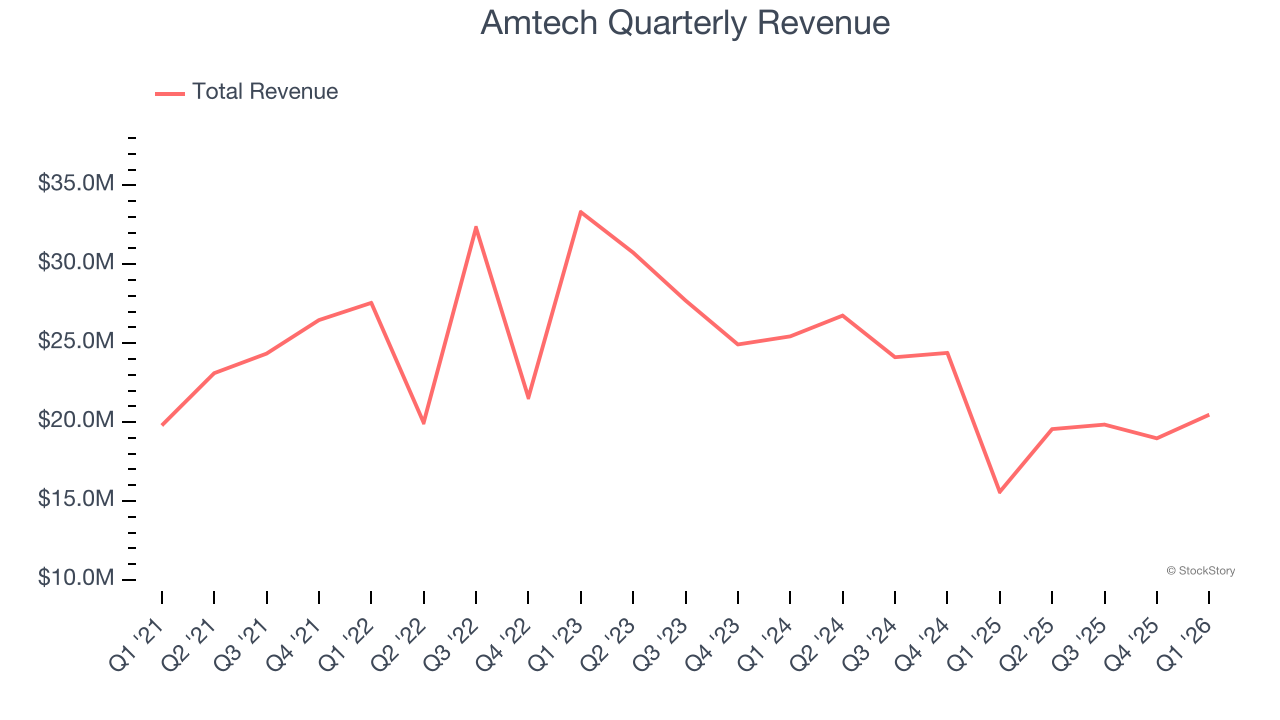

Semiconductor production equipment provider Amtech Systems (NASDAQ: ASYS) announced better-than-expected revenue in Q1 CY2026, with sales up 31.4% year on year to $20.47 million. On top of that, next quarter’s revenue guidance ($21.5 million at the midpoint) was surprisingly good and 7.5% above what analysts were expecting. Its non-GAAP profit of $0.10 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Amtech? Find out by accessing our full research report, it’s free.

Amtech (ASYS) Q1 CY2026 Highlights:

- Revenue: $20.47 million vs analyst estimates of $19.5 million (31.4% year-on-year growth, 5% beat)

- Adjusted EPS: $0.10 vs analyst estimates of $0.05 (significant beat)

- Adjusted EBITDA: $2.52 million vs analyst estimates of $2.1 million (12.3% margin, relatively in line)

- Revenue Guidance for Q2 CY2026 is $21.5 million at the midpoint, above analyst estimates of $20 million

- Operating Margin: 8.8%, up from -53.1% in the same quarter last year

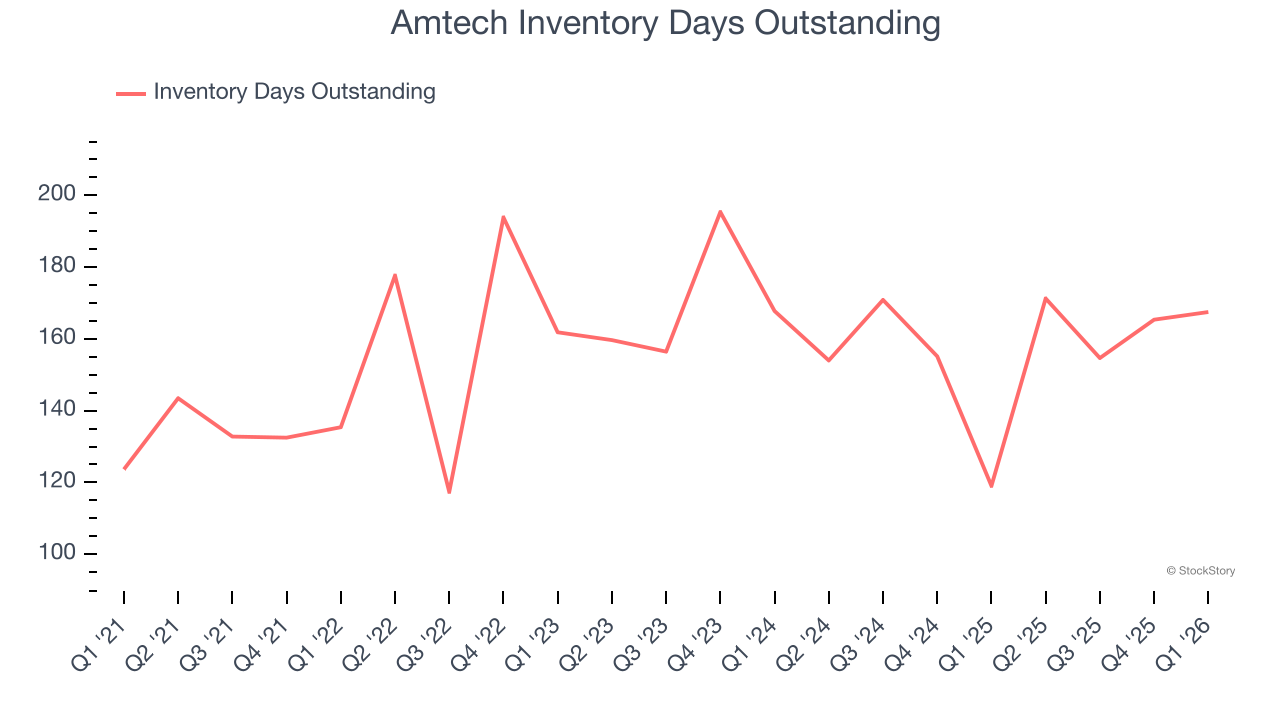

- Inventory Days Outstanding: 167, up from 165 in the previous quarter

- Market Capitalization: $262.1 million

Company Overview

Focusing on the silicon carbide and power semiconductor sectors, Amtech Systems (NASDAQ: ASYS) produces the machinery and related chemicals needed for manufacturing semiconductors.

Revenue Growth

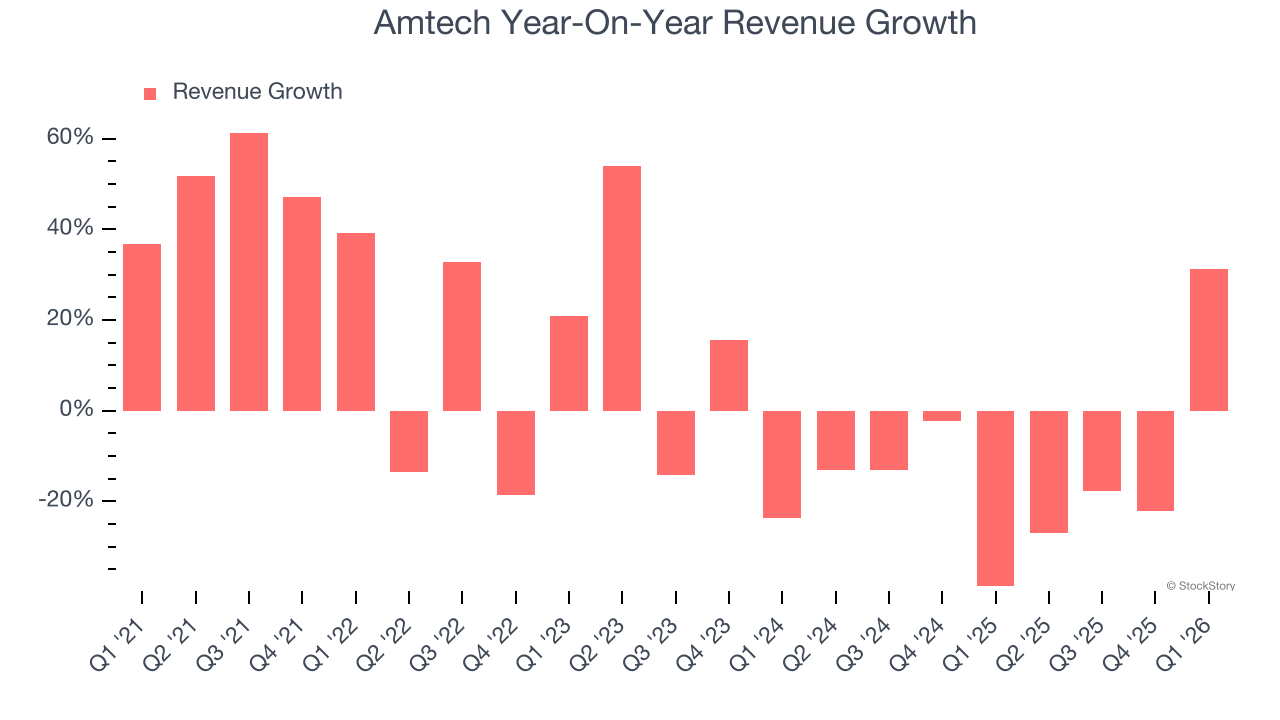

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Amtech grew its sales at a mediocre 3% compounded annual growth rate. This was below our standards and is a tough starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Amtech’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 14.9% annually.

This quarter, Amtech reported wonderful year-on-year revenue growth of 31.4%, and its $20.47 million of revenue exceeded Wall Street’s estimates by 5%. Adding to the positive news, Amtech’s growth inflected positively this quarter, pointing to a new upcycle as we come off the trough from the recent downturn. Company management is currently guiding for a 9.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.3% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Amtech’s DIO came in at 167, which is 11 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Amtech’s Q1 Results

It was good to see Amtech beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock remained flat at $19.09 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).