North Chicago, Illinois-based Abbott Laboratories (ABT) discovers, develops, manufactures, and sells healthcare products. Valued at $200.5 billion by market cap, ABT is a global leader in the large and growing in-vitro diagnostic market and its products include pharmaceuticals, nutritional, diagnostics, and vascular products.

Companies worth $200 billion or more are generally described as “mega-cap stocks,” and ABT definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the medical devices industry. ABT offers a diverse range of healthcare products helping to mitigate risks and capture opportunities in various markets. With a global presence in over 160 countries, ABT can tap into different economic conditions. The company's strong focus on research and development (R&D) enables it to develop innovative products and technologies, giving it a competitive advantage.

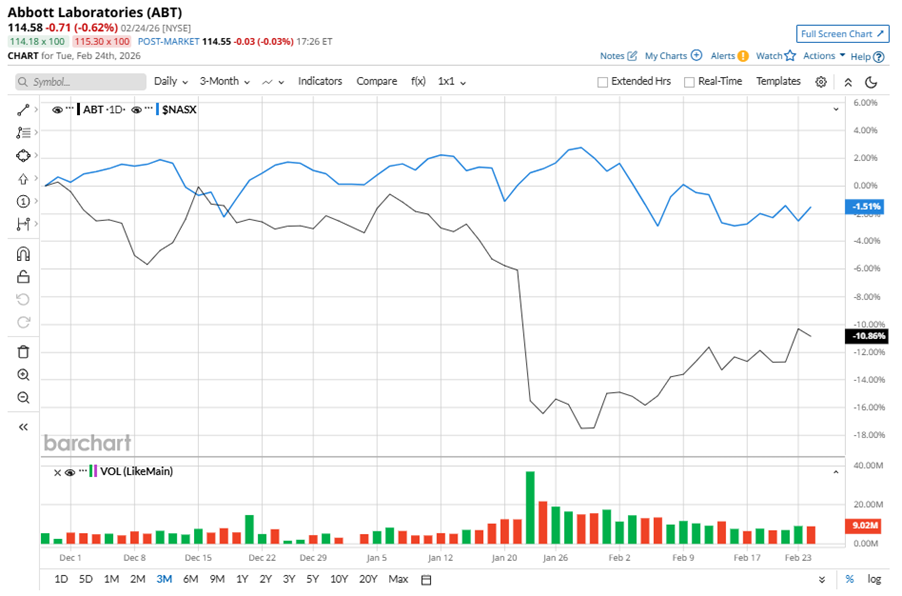

Despite its notable strength, ABT slipped 18.9% from its 52-week high of $141.23, achieved on Mar. 4, 2025. Over the past three months, ABT stock declined 9.9%, underperforming the Nasdaq Composite’s ($NASX) marginal dip during the same time frame.

Shares of ABT fell 8.6% on a YTD basis and dipped 15.1% over the past 52 weeks, underperforming NASX’s YTD losses of 1.6% and solid 18.6% returns over the last year.

To confirm the bearish trend, ABT has been trading below its 50-day and 200-day moving averages since mid-October, 2025, with slight fluctuations.

ABT’s underperformance is due to price-driven volume declines, especially after losing a major US WIC contract and ongoing consumer price sensitivity. CEO Robert Ford noted this path isn't sustainable, so they're making changes. Nutrition business is expected to remain pressured till mid-year, but new product launches in medical devices and diabetes care might boost growth.

On Jan. 22, ABT shares closed down more than 10% after reporting its Q4 results. Its adjusted EPS of $1.50 met Wall Street expectations. The company’s revenue was $11.5 billion, falling short of Wall Street forecasts of $11.8 billion. The company expects full-year adjusted EPS in the range of $5.55 to $5.80.

In the competitive arena of medical devices, Boston Scientific Corporation (BSX) has lagged behind ABT, with a 28% downtick over the past 52 weeks and a 21.2% losson a YTD basis.

Wall Street analysts are bullish on ABT’s prospects. The stock has a consensus “Strong Buy” rating from the 28 analysts covering it, and the mean price target of $134.38 suggests a potential upside of 17.3% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart