Electric cars have been the hot issue of the past five years as companies like Tesla (NASDAQ: TSLA) take over the podium to deliver all the benefits of switching from fossil fuel dependency to the claimed "Zero-emission" alternatives. However, while electric vehicles may be quiet, most of the knocking and banging required to bring a car to the open road happens behind the scenes. Valero Energy (NYSE: VLO) has taken the initiative to break down the zero-emission myth, as they call it, into the following reasoning.

Is Valero Really Taking on Elon?

Within the latest investor presentation by Valero, management took the time to explain to investors just why the rollout of the company's "Diamond Green Diesel," or DGD, as they have termed the product line, is a better and safer alternative to the growing adoption of electric vehicles.

According to management figures, embedded CO2 emissions at zero miles traveled (meaning emissions required to manufacture a car and bring it to market) are 50% lower for a gasoline-fueled car than for a fully electric vehicle. This reasoning is backed by stating that the lifecycle emissions generated from mining and extracting copper and lithium for batteries and the processing of these metals, along with the standard manufacturing process of the actual car, plus a good network of charging stations, all accrue to the added CO2 output.

Lastly, management brings up the point of the actual power generation (electricity) needed to upkeep the growing number of electric vehicles in the market today, as most of the power grid in the world is backed by natural gas or coal, which are both fossil fuels. While some nations are trying to switch to a nuclear energy source to decouple from these traditional power grids, Valero management has a valid point in that EVs are causing more harm than good on a CO2 basis. So what is their value proposition, then?

Renewable Diesel, the New Low-Carbon Fuel

Global magnates like Bill Gates have been on a quest to solve, or at least partly solve, the CO2 issue currently being faced. The former Microsoft (NASDAQ: MSFT) founder is focused more on global issues via the Bill and Melinda Gates Foundation. One of his main drivers is finding a reliable source of nuclear energy. Further, Gates has agreed that the world should attempt to find and adopt renewable sources of fossil fuels, such as the ones proposed by Valero in their DGD initiative.

Valero had reportedly deployed USD 725 million in capital expenditures dedicated to expanding their renewable diesel production capacity, enabling the company to produce nearly 1.2 billion gallons a year as of 2022, when only in 2013, their output capacity was 160 million gallons. The question becomes, how has this affected the operations of the business and therefore investor stakes?

As of 2015, Valero's renewable diesel business became EBITDA positive and has delivered growing returns to its dedicated capital expenditures. As of 2021, this segment generated nearly USD 400 million in EBITDA, declining from a high of USD 500 million in EBITDA for 2020. While refining represents most of the operating income power for Valero and all refineries operated at a weighted average of 97% capacity utilization (significantly higher than the industry's 75% average), the renewable diesel segment brought on palpable cost cuts.

As capacity expands for renewable diesel and subsequent economies of scale are achieved, Valero can extract more EBITDA from the segment and grow the overall business' margins despite capital expenditures associated with opening the newest DGD plant in Port Arthur.

Value Proposition

Gross margins have increased by nearly 7% from 1.9% in 2021 to 9.5% in 2022, partly from the high capacity utilization and volumes from the refinery business but also largely due to the profitability achieved in renewable diesel. These benefits have allowed the company to return USD 10.1 billion in dividends and an identical sum via share buybacks to investors. These trends, however, could be affected by the increase in oil prices lately, hurting the refining business but boosting the renewable diesel demand at the same time if markets deem Valero's battle against EV emissions valid.

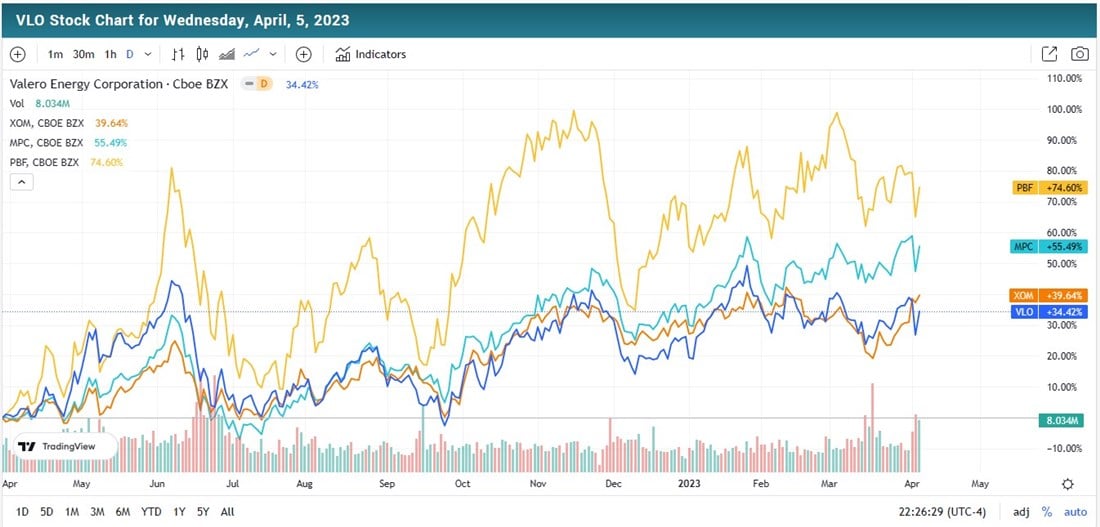

Despite offering a 3%+ dividend yield and further buyback potential, Valero stock is underperforming its peers Exxon Mobile (NYSE: XOM), Marathon Petroleum (NYSE: MPC), and PBF Energy (NYSE: PBF) even though these alternatives do not offer the dividends that Valero just left on the table for its shareholders.

Valero stock is also, according to analysts, the higher upside play when it comes to price targets. However, greedier value investors could wait out market volatility to deliver them the most proximate support range of $112-$118 per share, which lines up with the company's NAV (net asset value) per share computed as total assets minus total debt per share, a value translated to $118.75.