Golf equipment and apparel company Acushnet (NYSE:GOLF) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 4.6% year on year to $620.5 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $2.48 billion at the midpoint. Its GAAP profit of $0.89 per share was 12.9% above analysts’ consensus estimates.

Is now the time to buy Acushnet? Find out by accessing our full research report, it’s free.

Acushnet (GOLF) Q3 CY2024 Highlights:

- Revenue: $620.5 million vs analyst estimates of $620.4 million (in line)

- EPS: $0.89 vs analyst estimates of $0.79 (12.9% beat)

- EBITDA: $107.4 million vs analyst estimates of $96.34 million (11.5% beat)

- The company reconfirmed its revenue guidance for the full year of $2.48 billion at the midpoint

- EBITDA guidance for the full year is $400 million at the midpoint, in line with analyst expectations

- Gross Margin (GAAP): 54.4%, up from 52% in the same quarter last year

- Operating Margin: 13.2%, in line with the same quarter last year

- EBITDA Margin: 17.3%, in line with the same quarter last year

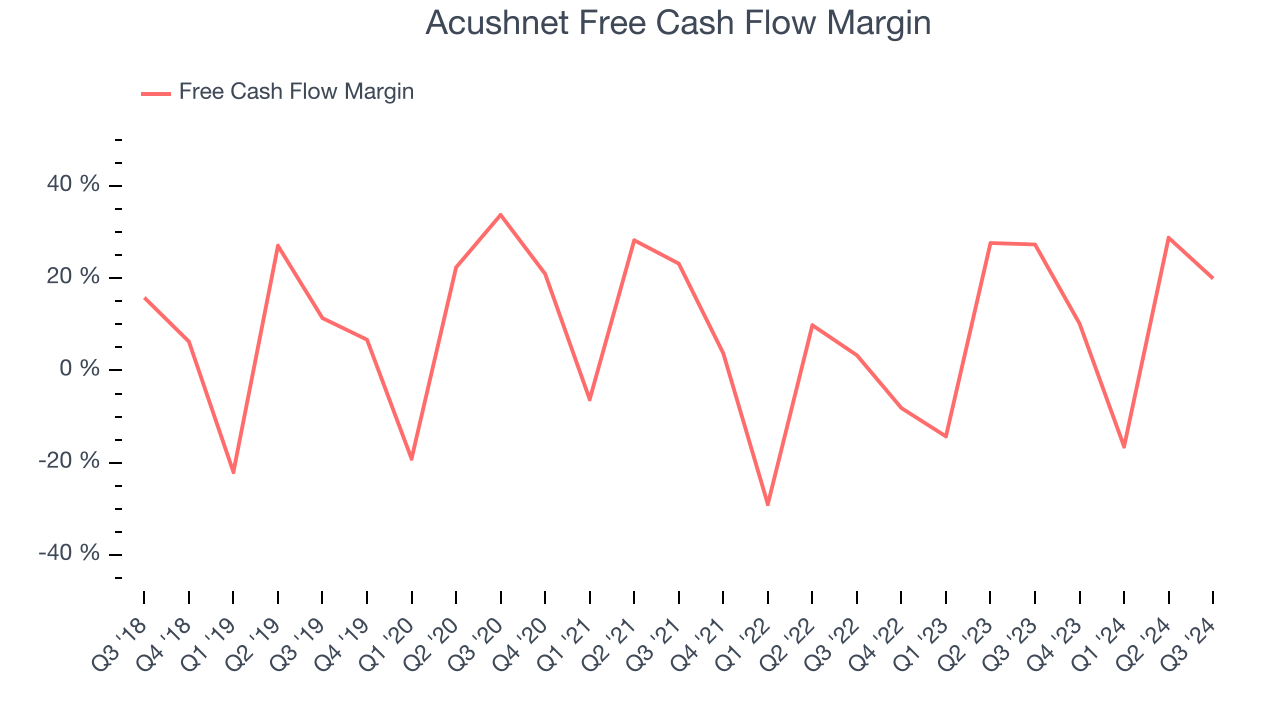

- Free Cash Flow Margin: 19.9%, down from 27.3% in the same quarter last year

- Market Capitalization: $3.91 billion

Company Overview

Producer of the acclaimed Titleist Pro V1 golf ball, Acushnet (NYSE:GOLF) is a design and manufacturing company specializing in performance-driven golf products.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

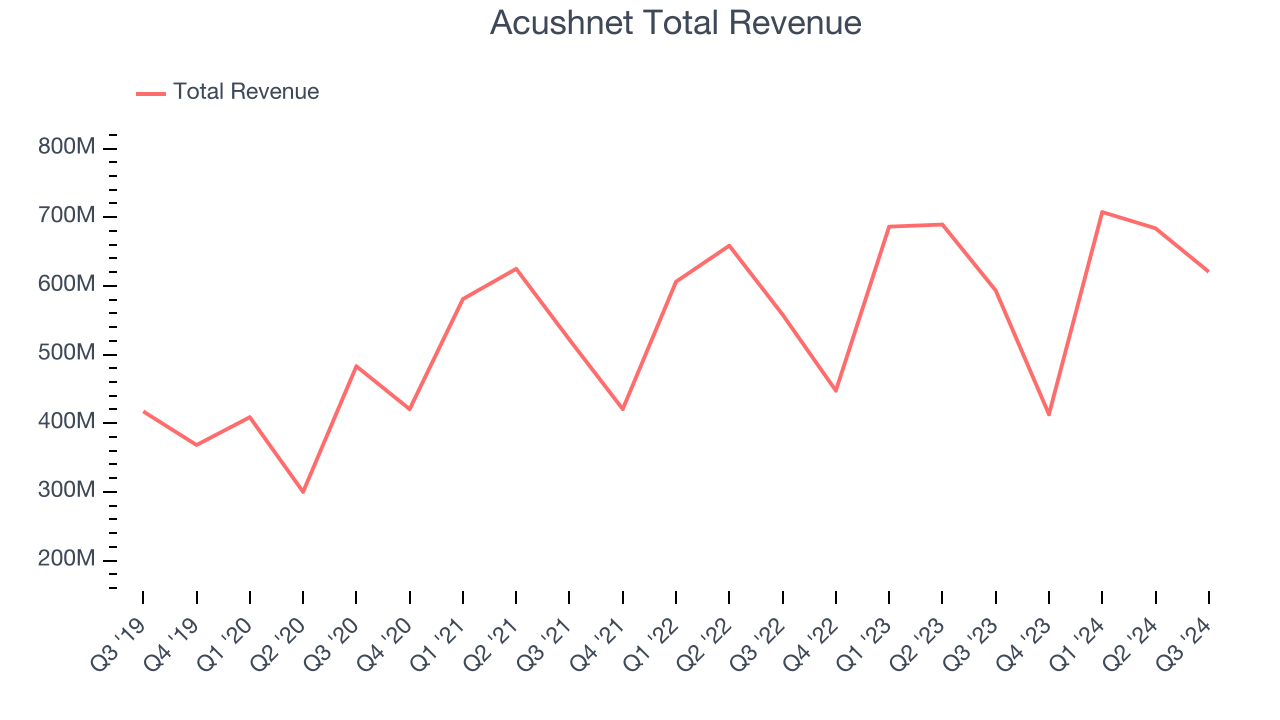

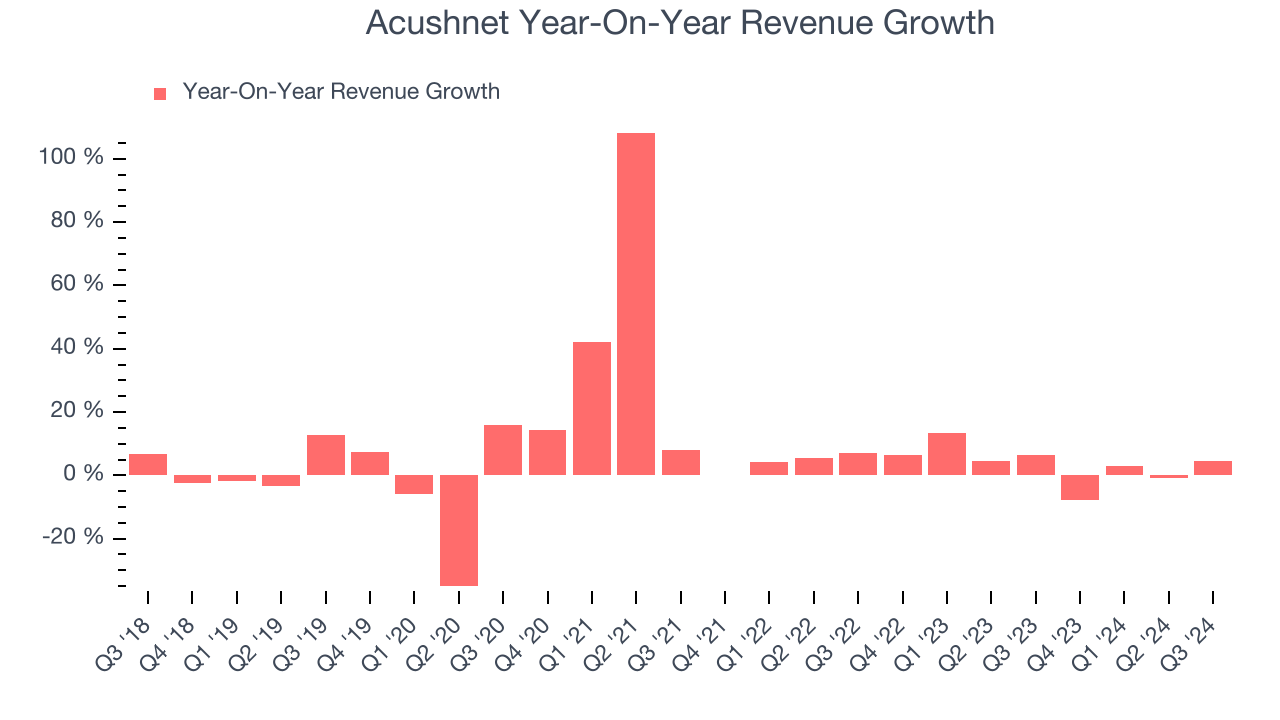

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Over the last five years, Acushnet grew its sales at a sluggish 7.9% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Acushnet’s recent history shows its demand slowed as its annualized revenue growth of 4% over the last two years is below its five-year trend.

We can dig further into the company’s revenue dynamics by analyzing its three most important segments: Titleist Balls, Titleist Clubs, and FootJoy, which are 30.7%, 34.5%, and 21.5% of revenue. Over the last two years, Acushnet’s Titleist Balls (golf balls) and Titleist Clubs (golf clubs) revenues averaged year-on-year growth of 8.1% and 9.4% while its FootJoy revenue (apparel) averaged 4.1% declines.

This quarter, Acushnet grew its revenue by 4.6% year on year, and its $620.5 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, an improvement versus the last two years. While this projection illustrates the market thinks its newer products and services will catalyze better performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Acushnet has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9.6%, subpar for a consumer discretionary business.

Acushnet’s free cash flow clocked in at $123.7 million in Q3, equivalent to a 19.9% margin. The company’s cash profitability regressed as it was 7.4 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

Key Takeaways from Acushnet’s Q3 Results

It was good to see Acushnet beat analysts’ EBITDA and EPS expectations this quarter. On the other hand, its Titleist Clubs revenue missed. Still, this quarter had some key positives. The stock traded up 4.5% to $66.22 immediately following the results.

Indeed, Acushnet had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.