Chord Energy has been on fire lately. In the past six months alone, the company’s stock price has rocketed 43.6%, reaching $142.75 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is CHRD a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Are We Positive On CHRD?

Holding the largest acreage position in the Williston Basin, Chord Energy (NASDAQ: CHRD) drills for and produces crude oil, natural gas liquids, and natural gas in North Dakota's Williston Basin.

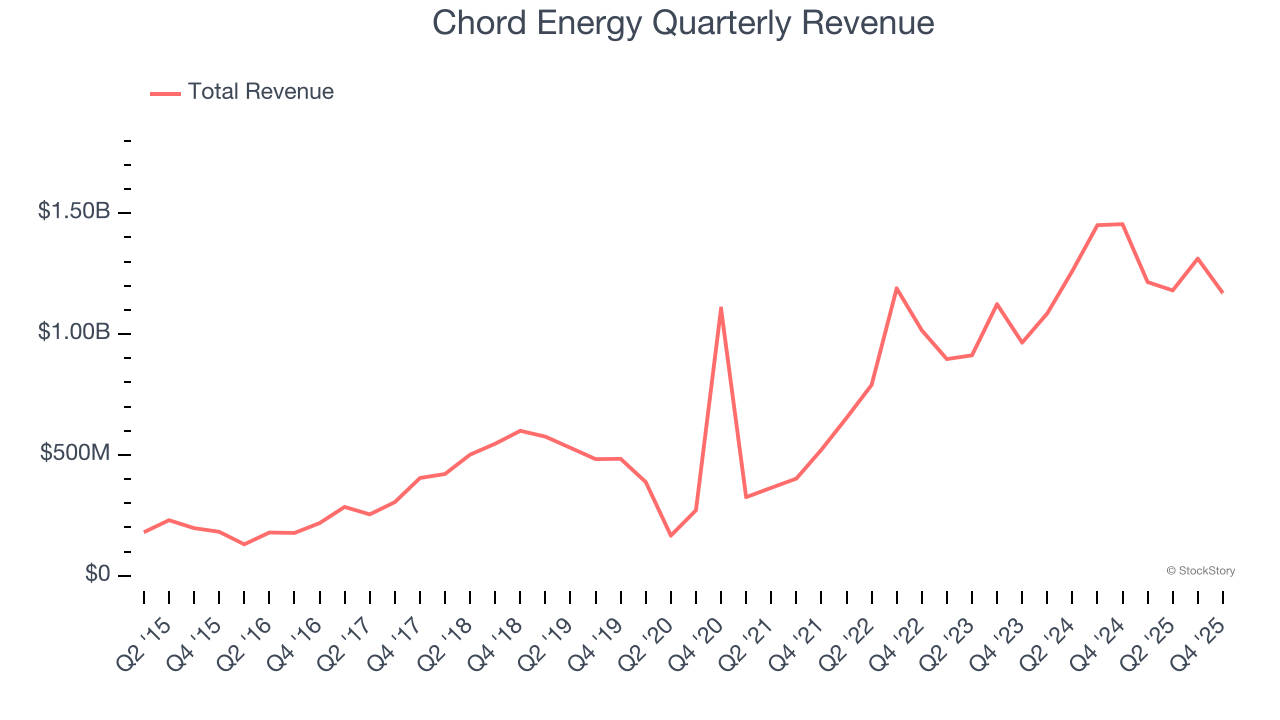

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Luckily, Chord Energy’s sales grew at an excellent 20.4% compounded annual growth rate over the last five years. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program.

Chord Energy’s $4.88 billion of revenue in the last year is mid-sized for the industry.

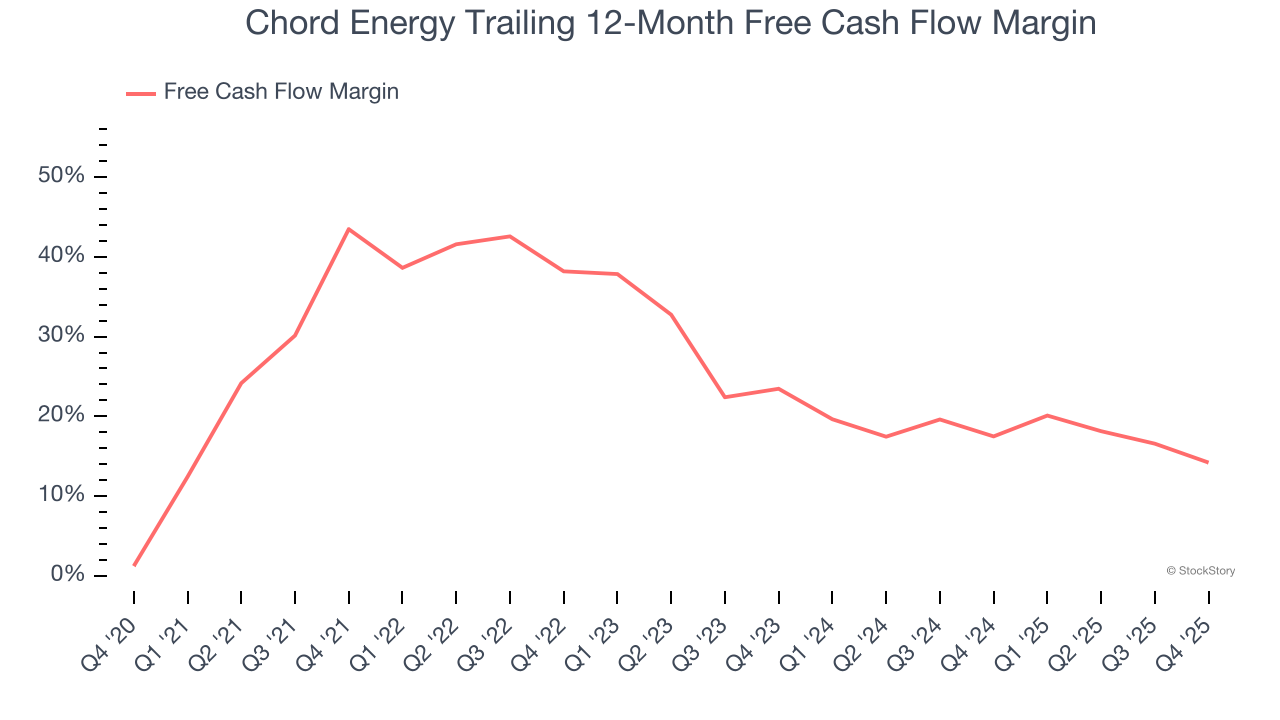

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Chord Energy has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 24% over the last five years.

Final Judgment

These are just a few reasons why we think Chord Energy is an elite energy upstream and integrated energy company, and with the recent surge, the stock trades at 13× forward P/E (or $142.75 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Chord Energy

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.