Monday.com’s (NASDAQ: MNDY) guidance is tepid relative to the consensus outlook, but no reason to sell the stock and certainly no reason for the market to drop 10%. As tepid as the guidance may be, it is still a strong guide for the business, and it is likely to be cautious, given the trends. Some takeaways from the Q3 report are outperformance, scaling, expansion, and deepening penetration of clients - takeaways that add up to strengthening business leverage for the leading work management platform. The stock price pulled back following the release but will likely not stay down long.

Monday.com Builds Leverage With Workplace Automation

Monday.com’s Q3 results are good. The company grew revenue to $251 million, up 32.7% compared to last year, beating the consensus estimate by 190 basis points. The strength was driven by deepening penetration and a growing client count that shows Monday.com growing alongside the businesses it serves while capturing new, larger clients.

The number of clients contributing more than $50K and $100K in annual recurring revenue increased by more than 40%, putting total ARR above $1 billion. The net retention rate or revenue from existing customers as a percentage of last year’s contribution is 111%, accelerating from the previous month as the rate of penetration increases.

Margin news is also good. The company’s adjusted operating margin held steady at 13%, driving a 30% increase in net cash from operations and a 26% increase in free cash flow. The free cash flow is a significant driver for this investment, as the margin ran at 32% for the quarter and is expected to sustain a 30% pace for the full year. The cash flow allows the company to reinvest to expand offerings and scale operations while maintaining a fortress balance sheet. The balance sheet highlights include a cash build and increased assets that more than offset the increased liability. The net result is a 20% increase in equity, with most assets in cash. Total leverage is less than 0.5x cash and less than 1x equity.

Monday.com Guides for Sustained Growth and Robust Cash Flow

Monday.com’s guidance is mixed. The full-year targets are better than the consensus reported by MarketBeat.com ahead of the release due to the Q3 strengths, but Q4 will be tepid, only aligning with the forecasts quarterly. The risk is that growth is slowing to below 30%, but the 28% forecasted by the company is still solid and likely to be cautious. Regardless, analysts are unlikely to alter their positions because of the guide, and they support the market.

The analysts' trends in 2024 include increased coverage and a growing conviction that the stock is undervalued. The number of analysts covering the stock increased by nearly 50% to 15, while the consensus price target trended higher. The consensus target puts the market near $306, but the most recent revisions run in the $320 to $340 range, a gain of 15% to 20% from support targets near $280.

Institutions also support the stock and are likely to buy with the price at a discount. They have bought the stock on balance for 3 consecutive quarters, aligning with the market bottom in early 2024 and the updraft since summer.

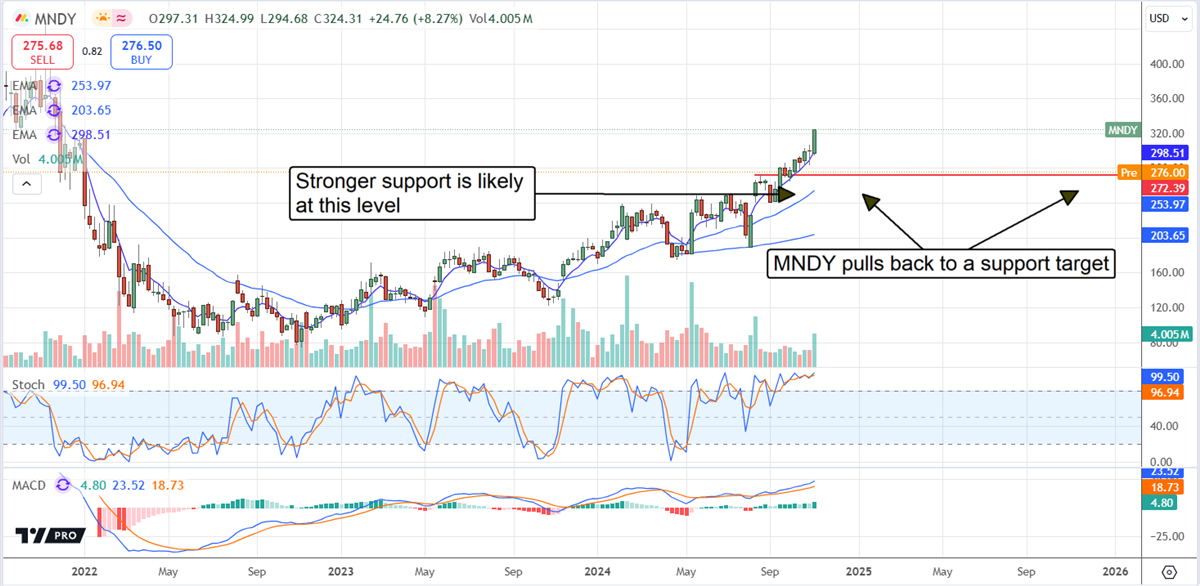

Monday.com Price Pulls Back: Wait for the Market to Signal

Monday.com's price pulled back to a potential buying point, but the market hasn’t confirmed the bottom in the pullback yet. While a rebound is expected, the market may move as low as $250 before it begins. The $275 level is a possible support target but weak compared to the firmer support provided by the 150-day EMA. A move below that level would be bad for the market and could lead to an even larger decline. Assuming the market confirms support near $250 or higher, new highs are likely before mid-year 2025.