Recent advancements in artificial intelligence have sent shockwaves through countless industries, sparking widespread fears that core services could soon become obsolete. Nowhere is this panic more pronounced than in the software sector, where an unfolding “SaaS-pocalypse” has erased billions in market value as investors fret over AI’s potential to commoditize everything from productivity tools to enterprise platforms.

Intuit (INTU) was already experiencing a decline before the late-January wave of AI-driven selling intensified, but the panic accelerated its slide. From its all-time high near $814 last July, INTU stock has plummeted 47% to current levels around $440. Yet this selloff appears overdone—Intuit is not only positioned to survive the SaaS-pocalypse but is also poised to thrive in the AI era.

The Roots of Intuit’s Pre-Panic Slide

Even before the latest AI fears erupted, Intuit faced mounting pressure that weighed on its valuation. Investors grew concerned about a cooling growth trajectory, highlighted by softer Q3 guidance calling for just 10% revenue growth compared to the 17% posted in the prior quarter. Integration challenges with the Mailchimp acquisition continued to drag on the Global Business Solutions segment, even as core offerings like QuickBooks delivered robust 21% growth ex-Mailchimp.

Broader market dynamics compounded the issue: a sharp contraction in the stock’s price-to-earnings multiple—from above 50x to roughly 25x—reflected higher interest rates and a recalibration of software-sector expectations. From late November through late February, these factors alone drove a roughly 35% decline, setting the stage for the accelerated drop once AI panic took hold.

Why the Market Initially Feared AI Disruption

The software selloff intensified in late January as investors fixated on AI’s ability to automate complex tasks once considered moat-protected. For Intuit, the spotlight fell squarely on TurboTax and QuickBooks. Headlines about tools like Claude Cowork and lingering ChatGPT tax-filing speculation fueled worries that consumers and small businesses could bypass Intuit’s platforms entirely.

Critics argued that general-purpose AI could handle basic tax preparation and accounting workflows, eroding the need for specialized software subscriptions. This narrative triggered indiscriminate selling across SaaS names, with Intuit caught in the crossfire despite its decades of embedded compliance expertise and customer data. The result was a swift acceleration of an already softening stock, wiping out nearly $100 billion in market value over six months and pushing shares to multi-year lows.

Analysts Highlight Resilience Amid the Turmoil

Wall Street has pushed back against the doomsday narrative. Jefferies’ proprietary AI Risk Matrix and At-Risk Basket—now down 24% year-to-date (YTD)—flag vulnerable software names but explicitly exclude Intuit from the highest-risk cohort. Instead, analysts named Intuit their “top large-cap pick in apps,” citing its massive data moat: 80 different AI model variations trained on more than 40 years of data across roughly 100 million customers. Embedded workflows, regulatory expertise, and scale create barriers that general-purpose AI tools cannot easily replicate.

Mizuho echoed this view, calling recent AI disruption fears “overblown” and reiterating an “Outperform” rating while characterizing Intuit as among the most resilient names in its Software AI Resilience Framework. The firm emphasized Intuit’s integrated data, compliance edge, and end-to-end workflows as durable advantages.

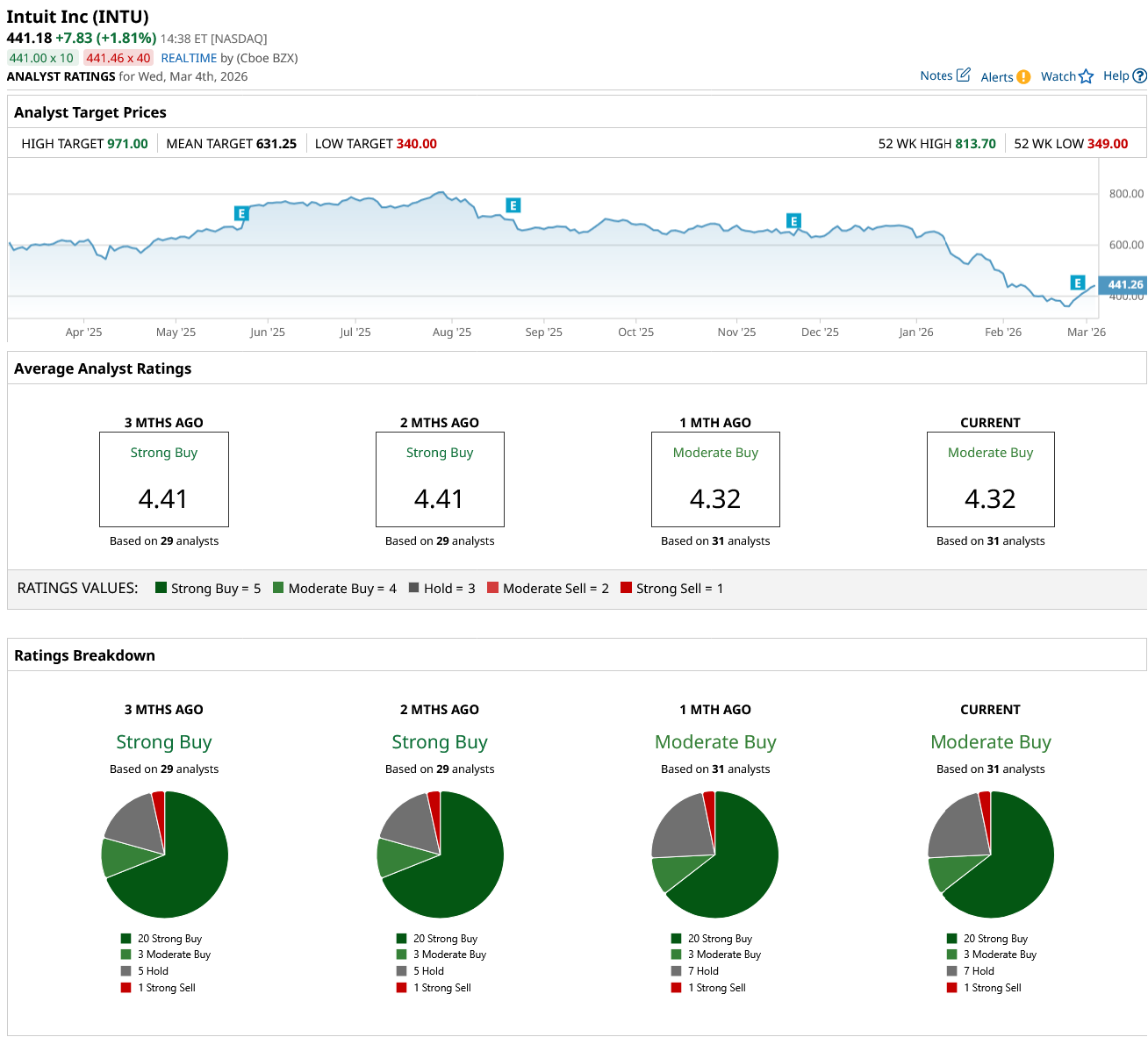

Overall, Wall Street remains constructive. Thirty-one analysts rate INTU a consensus "Moderate Buy," with an average price target hovering near $631—implying more than 43% upside potential from current levels despite recent downward revisions from a handful of firms.

Key Takeaway

Beneath the headline volatility, Intuit’s underlying business continues to perform exceptionally well. The company is growing its top line at a rapid clip—17% year-over-year revenue growth to $4.65 billion in fiscal Q2, beating estimates—while generating substantial free cash flow. That cash engine supports aggressive capital returns: Intuit repurchased $961 million of stock in fiscal Q2 alone, with $3.5 billion still authorized.

On the dividend front, the board just approved a quarterly payout of $1.20 per share, a 15% increase, keeping the payout ratio low at roughly 30%. The company now boasts 14 consecutive years of dividend raises, with a 16% compound annual growth rate over the past decade.

In a sector gripped by AI panic, Intuit stands out as a beaten-down dividend growth stock with the fundamentals and moat to not only survive the SaaS-pocalypse but deliver lasting shareholder value long after the panic subsides.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart