California-based Essex Property Trust, Inc. (ESS) is a leading real estate investment trust (REIT) specializing in high-quality multifamily communities along the U.S. West Coast. With a market capitalization of $16.8 billion, the company owns, operates, and develops apartment properties primarily in supply-constrained, high-demand markets such as Southern California, the San Francisco Bay Area, and Seattle.

Essex Property Trust’s stock has been stuck in a slump, struggling to find momentum even as parts of the real estate market show signs of life. Over the past 52 weeks, shares have slid 14.2%, and they’re still down 8.5% year-to-date. That performance trails well behind the S&P 500 Index ($SPX), which has gained 11% and 12.3% over the same periods, respectively.

Even within its own sector, Essex hasn’t kept up. The Real Estate Select Sector SPDR Fund (XLRE) has fallen 6.5% over the past 52 weeks and gained marginally in 2025, still notably better than Essex’s persistent downturn.

On Oct. 29, Essex Property Trust reported its third-quarter 2025 results, triggering a brief bout of volatility in the stock. Shares initially slipped 3.5% as investors reacted to softer growth metrics, but the pullback didn’t last long. Over the next few trading sessions, the stock staged an impressive rebound of more than 5%. Its net income per share rose 39% to $2.56, while core FFO increased about 1.5% to $3.97. Same-property revenue and NOI both improved 2.7% and 2.4%, respectively, and occupancy held strong at 96%. The company reaffirmed confidence by raising its full-year net Income per diluted share guidance by $0.41 at the midpoint to a range of $10.53 to $10.63.

For the fiscal year 2025, ending in December 2025, Wall Street analysts expect Essex Property Trust’s bottom line to grow by 2.3% YOY to $15.96 per share on a diluted basis. The company has a solid history of surpassing consensus estimates, topping them in all of the trailing four quarters.

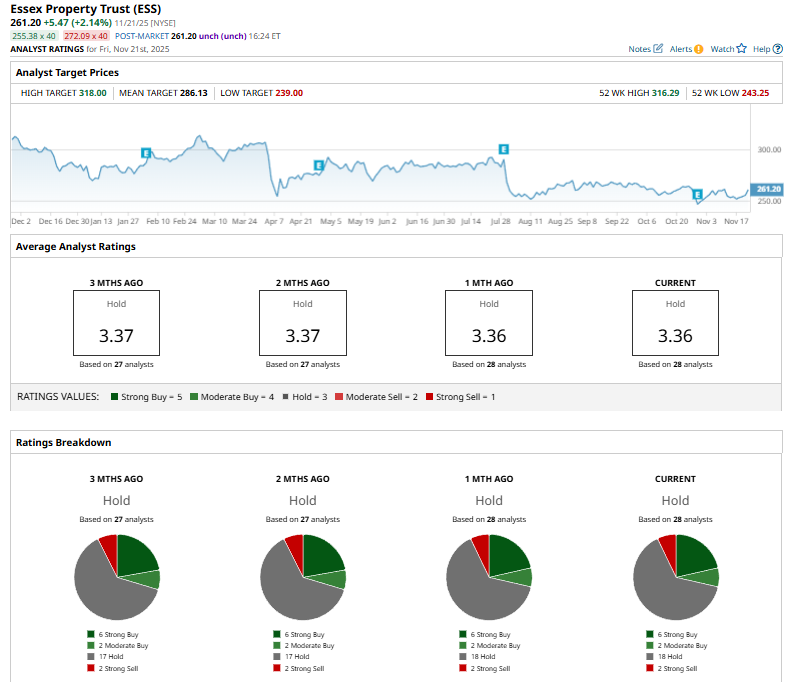

Among the 28 Wall Street analysts covering Essex Property Trust’s stock, the consensus is a “Hold.” That’s based on six “Strong Buy” ratings, two “Moderate Buys,” 18 “Hold” ratings, and two “Strong Sell” ratings.

On Oct. 14, Wells Fargo analyst James Feldman reiterated his “Hold” rating on Essex Property Trust and set a price target of $280.

Essex Property Trust’s mean price target of $286.13 indicates a 9.5% upside over current market prices. The Street-high price target of $318 implies a potential upside of 21.7%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- GDP, Retail Sales and Other Can't Miss Items this Week

- Chevron's Latest 5-Yr Plan Implies a Major Dividend Hike - CXX Stock Looks Cheap

- Wall Street Is Betting on a Nuclear Renaissance. Here Are the 3 Top-Rated Nuclear Energy Stocks to Buy Now.

- The Saturday Spread: Using Data Science to Pick Out the Most Compelling Discounts (NVO, SOFI, FAST)