With a market cap of $788.6 billion, JPMorgan Chase & Co. (JPM) is a global bank and financial holding company that provides a wide range of services, including consumer banking, investment banking, and asset and wealth management across multiple regions worldwide. It serves individuals, businesses, and institutions with products such as loans, deposits, investment solutions, and financial advisory services. JPM is expected to announce its fiscal Q1 2026 results before the market opens on Tuesday, Apr. 14.

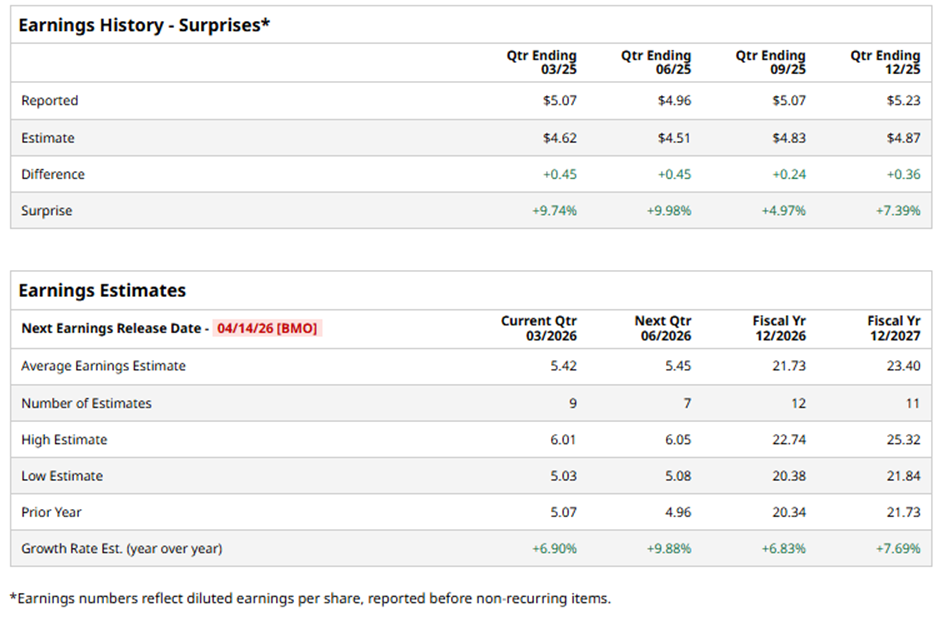

Ahead of this event, analysts forecast the New York-based company to report a profit of $5.42 per share, up 6.9% from $5.07 per share in the year-ago quarter. The company has surpassed Wall Street's earnings estimates in the last four quarters.

For fiscal 2026, analysts expect the global financial giant to report an EPS of $21.73, a 6.8% rise from $20.34 in fiscal 2025. In addition, EPS is anticipated to grow 7.7% year-over-year to $23.40 in fiscal 2027.

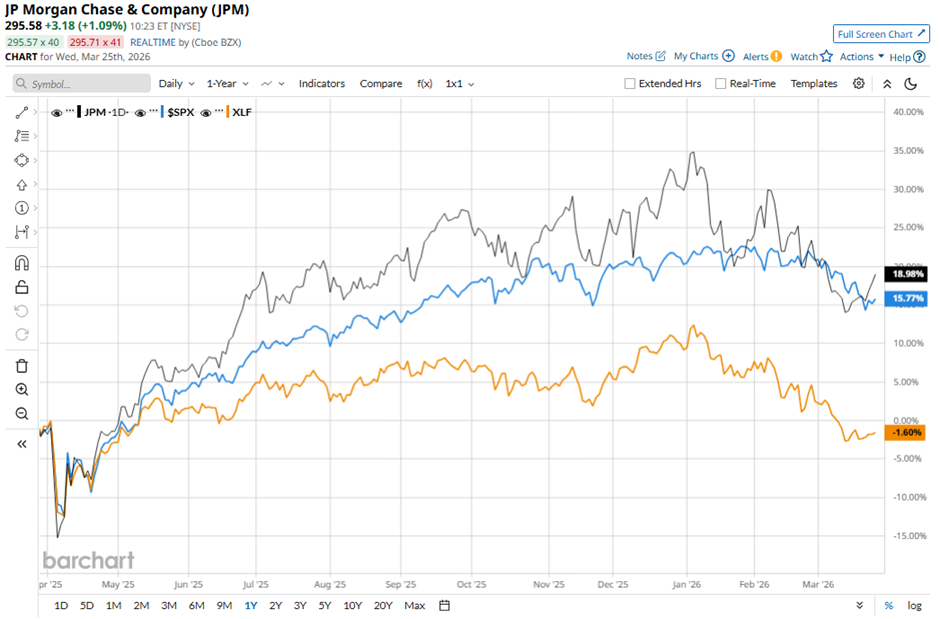

Shares of JPMorgan have soared 17.7% over the past 52 weeks, outperforming both the S&P 500 Index's ($SPX) 14.2% rise and the State Street Financial Select Sector SPDR ETF's (XLF) 1.8% decline over the same period.

Despite reporting Q4 2025 EPS of $5.23 and revenue of $46.8 billion, shares of JPMorgan fell 4.2% on Jan. 13 due to concerns over rising credit costs, with provisions for loan losses surging to $4.66 billion, well above the estimate and up from $2.63 billion a year earlier. Investor sentiment was further hurt by weak investment banking performance, as fees declined 5% year-over-year to $2.3 billion, missing the consensus and signaling softer deal activity.

Additional pressure came from forward-looking risks, including an expected card charge-off rate of about 3.4% and cautious outlook on consumer sentiment and mortgage trends, which outweighed strong growth in Markets revenue up 17% and Asset & Wealth Management AUM rising 18% to $4.8 trillion.

Analysts' consensus view on JPMorgan’s stock is cautiously optimistic, with a "Moderate Buy" rating overall. Among 28 analysts covering the stock, 13 recommend "Strong Buy," three "Moderate Buys," and 12 suggest "Hold." The average analyst price target of $339.08, indicating a potential upside of 14.7% from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- EchoStar Stock Just Broke Above Its 50-Day Moving Average on SpaceX IPO Hype. Does That Make SATS a Buy?

- Micron Broke Below Its 50-Day Moving Average. Should You Buy the Dip?

- As the Oil Shock Sends Energy Stocks Soaring, Buy These 3 Now

- Warning: Investing in Tech Stocks May Just Be 1 Big, Overcrowded Trade