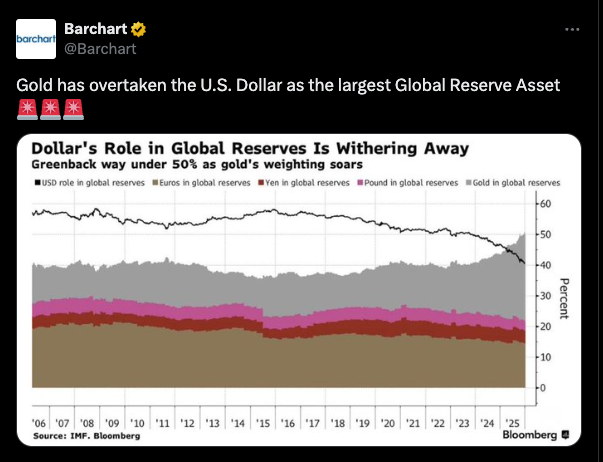

Markets continue to register concern over the geopolitical and economic situations with gold replacing the US dollar as the largest global reserve asset.

While gold and silver rallied overnight, the Energies sector was mostly lower indicating US bombs did not fall on Iran immediately following the close of the Winter Olympics.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.The Grains sector was under light pressure as it waits for China's New Year holiday to come to an end Monday.

Morning Summary: It’s pre-dawn Monday morning. Over the weekend the Winter Olympic torch was passed from Italy to France before being extinguished for four years, and as far as I know the world still turns. What I mean is a quick check and markets are trading, reflecting concern over the global political and economic situations, but there are at least situations in play to still be concerned over. Following last Friday’s US Supreme Court decision and expected announcement of increased tariffs by the self-declared President of Venezuela, the US dollar index ($DXY) was under pressure to start this week, down as much as 0.42, while US stock index futures were also in the red. Meanwhile, indicating the world is expecting something to happen, both gold and silver posted strong rallies, April gold (GCJ26) gaining as much as $117.90 (2.3%) and March silver (SIH26) adding as much as $5.34 (6.5%). In related news, Barchart posted a Bloomberg chart showing gold has overtaken the US dollar as the largest global reserve asset. As for Energies, the sector was mostly lower early Monday morning with natural gas and spot heating oil the outliers. Also related to the US one word trade policy, the Chinese New Year holiday ends today.

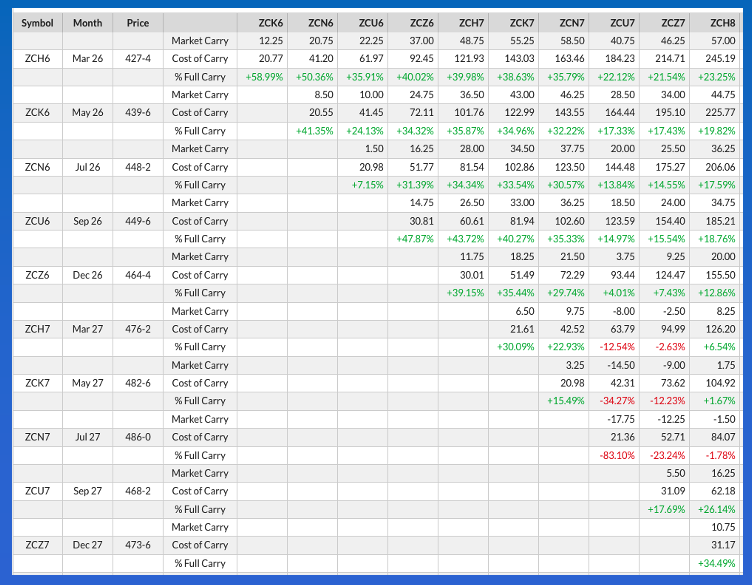

Soybeans: The idea of a global (universal?) 15% increase in tariffs sent the soybean market lower initially with the May issue (ZSK26) falling as much as 9.75 cents on still light overnight trade volume of 11,500 contracts. Again, activity was likely limited by the last hours of China’s 9-day New Year holiday, putting the spotlight on Monday night’s (Tuesday morning Beijing time) open. We also know Brazil’s harvest continued to progress over the weekend, though the May-July spread isn’t showing much commercial activity to start the week. A look back at Friday’s close and we see both the March-May and May-July spreads covered more calculated full commercial carry than the previous week’s settlement, though holding in neutral territory on either side of 50%. The National Soybean Index was priced near $10.7250 Friday night, putting national average basis at about 80.75 cents under May futures, as compared to the previous Friday’s final figure of 80.25 cents under and the previous 5 and 10-year lows for the first weekly close of March (next week) of 81.5 cents under May. On the other side of the market, Watson reportedly increased its net-long futures position by 45,460 contracts, pushing it to 191,790 contracts as of Tuesday, February 17. This opens the door wider for long liquidation.

Corn: The corn market was quietly lower overnight through early Monday morning. The May issue posted a trading range 1.75 cents, all of it below unchanged on trade volume of 18,500 contracts and was sitting 1.0 cent lower at this writing. Along with the rapid progress of Brazil’s 2026 soybean harvest, the first corn crop continues to roll in while fields are made ready for the safrinha (second) corn crop. This had both the March-May and May-July futures spreads under pressure at last week’s close, covering 59% and 41% calculated full commercial carry respectively as compared to the previous week’s settlement of 49% and 39%. As for basis, the National Corn Index ($CNCI) was priced at $3.9525, still below the previous 5-year end of February low of $3.9975 and putting the national average basis calculation at 44.5 cents under May future. The previous Friday’s final figure was 43.25 cents under with the previous 5-year and 10-year low weekly closes for this first week of March at about 40.5 cents under May. The bottom line: Heading into the last week of the winter quarter (Q2), US corn supplies are growing in relation to demand. Meanwhile, the latest Commitments of Traders report showed Watson had largely moved to the sidelines in corn.

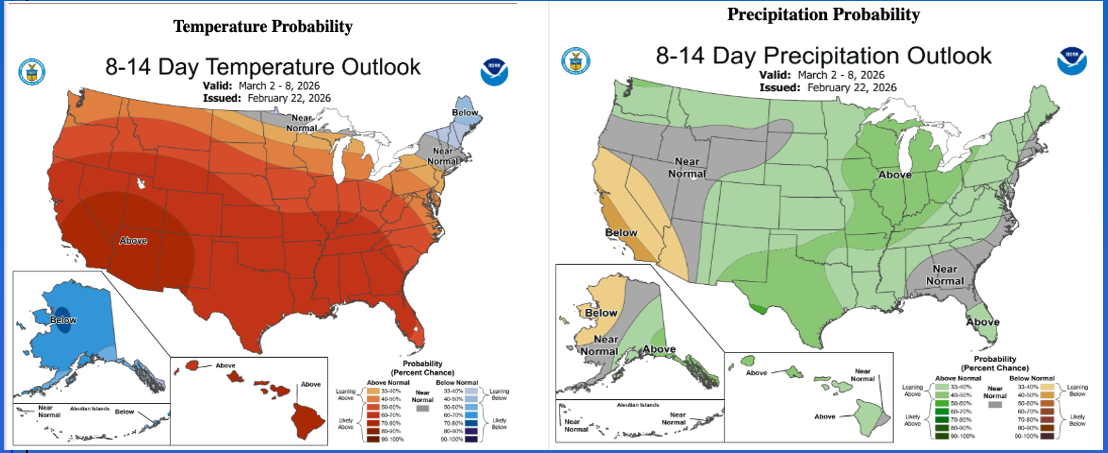

Wheat: The wheat sub-sector was in the red pre-dawn Monday, again on what could be considered solid overnight trade volume. The first market that caught my eye was HRS where the March issue was sitting 10.75 cents lower after falling as much as 16.75 cents on trade volume of 120 contracts. Meanwhile, the May issue was down 3.25 cents and showing 165 contracts changing hands. I’m not sure how much to read into this regarding commercial selling, but it is something to keep an eye on as today and the rest of the week plays out. The May SRW issue lost as much as 5.75 cents overnight on trade volume of 9,700 contracts but was sitting only 1.5 cents lower at this writing. With meteorological spring fast approaching, on March 1 to be exact, attention should continue to turn to new-crop winter wheat. The July SRW issue was down 2.0 cents after sliding as much as 5.75 cents to open the week. Over in HRW the July issue (KEN26) was down 2.75 cents while registering about 550 contracts changing hands. The latest 8-to-14-day forecast calls for above normal temperatures and precipitation across the US Plains and Midwest winter wheat growing areas.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart