Carlisle has been treading water for the past six months, recording a small return of 2% while holding steady at $333.65. The stock also fell short of the S&P 500’s 32.7% gain during that period.

Is now the time to buy CSL? Find out in our full research report, it’s free for active Edge members.

Why Does CSL Stock Spark Debate?

Originally founded as Carlisle Tire and Rubber Company, Carlisle Companies (NYSE: CSL) is a multi-industry product manufacturer focusing on construction materials and weatherproofing technologies.

Two Positive Attributes:

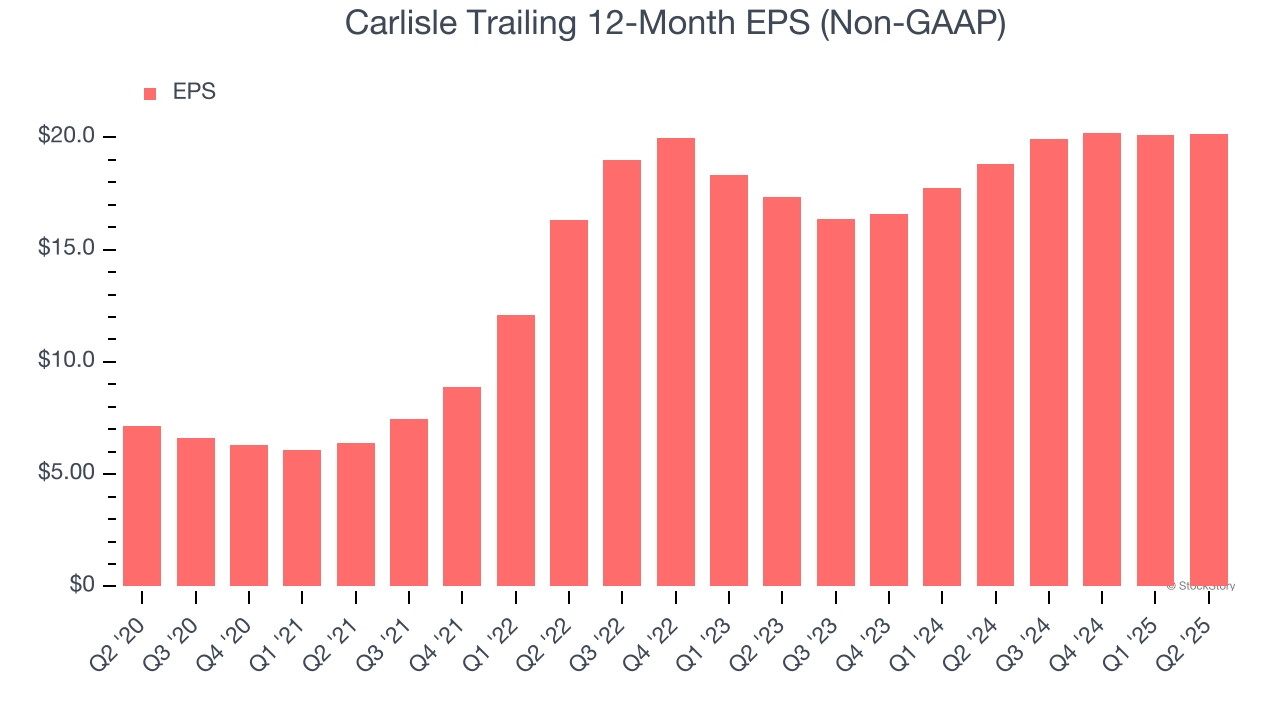

1. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Carlisle’s EPS grew at an astounding 23% compounded annual growth rate over the last five years, higher than its 2.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

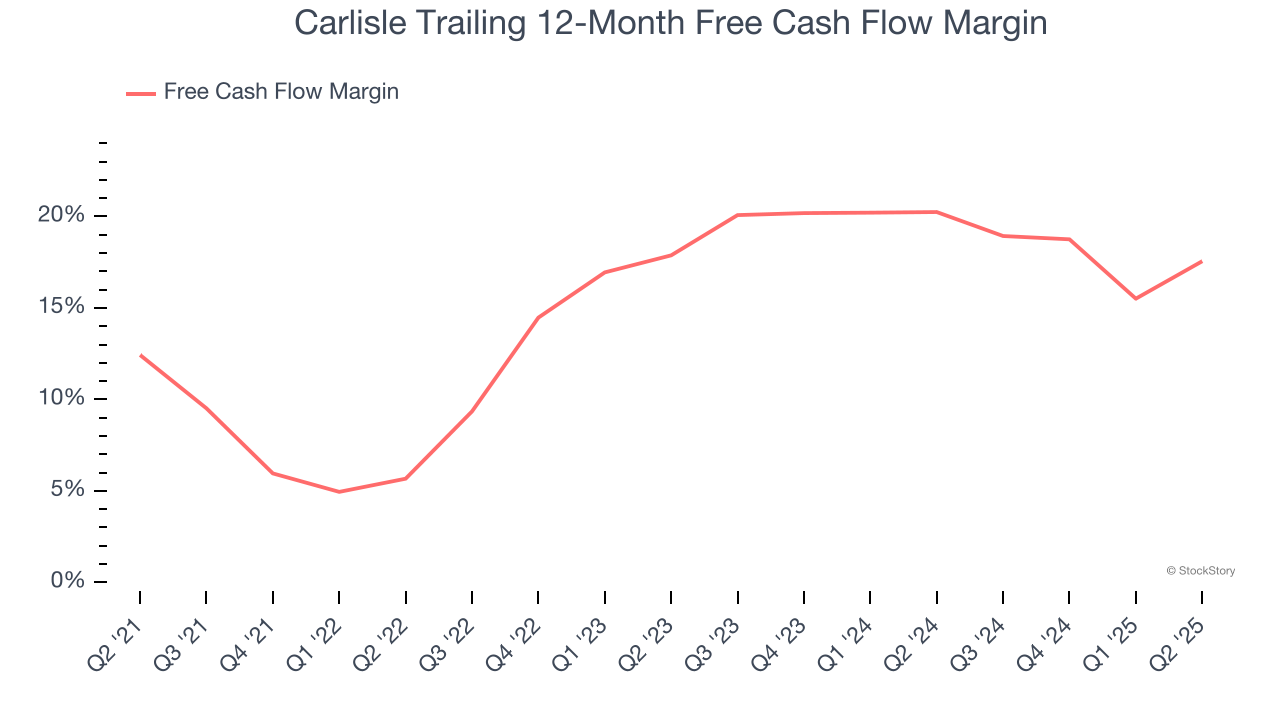

2. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Carlisle’s margin expanded by 5.1 percentage points over the last five years. This is encouraging because it gives the company more optionality. Carlisle’s free cash flow margin for the trailing 12 months was 17.6%.

One Reason to be Careful:

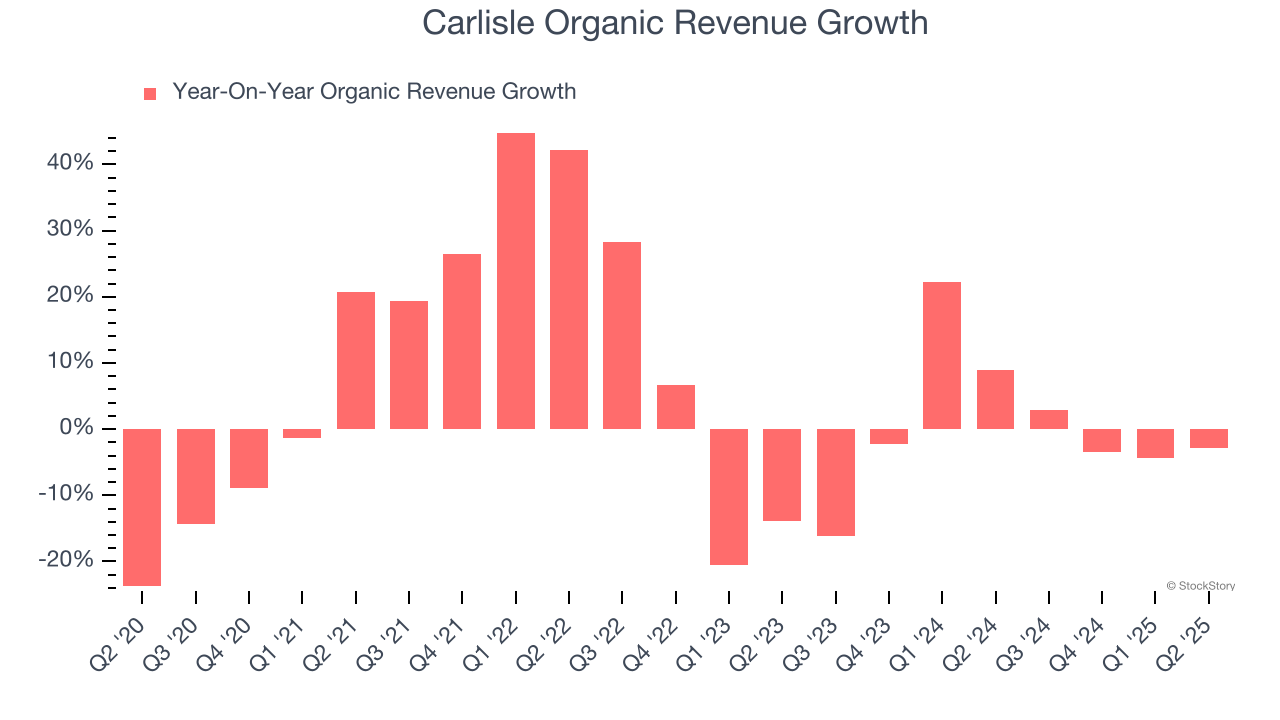

Core Business Falling Behind as Demand Plateaus

We can better understand Building Materials companies by analyzing their organic revenue. This metric gives visibility into Carlisle’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Carlisle failed to grow its organic revenue. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Carlisle might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

Final Judgment

Carlisle’s positive characteristics outweigh the negatives. With its shares trailing the market in recent months, the stock trades at 14× forward P/E (or $333.65 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free for active Edge members .

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.