Headquartered in Secaucus, New Jersey, Quest Diagnostics Incorporated (DGX) runs one of the country’s largest diagnostic testing networks. The company connects laboratories, patient service centers, mobile healthcare professionals, and digital health platforms to deliver clinical testing, health screenings, and data driven medical insights for patients, physicians, and healthcare systems.

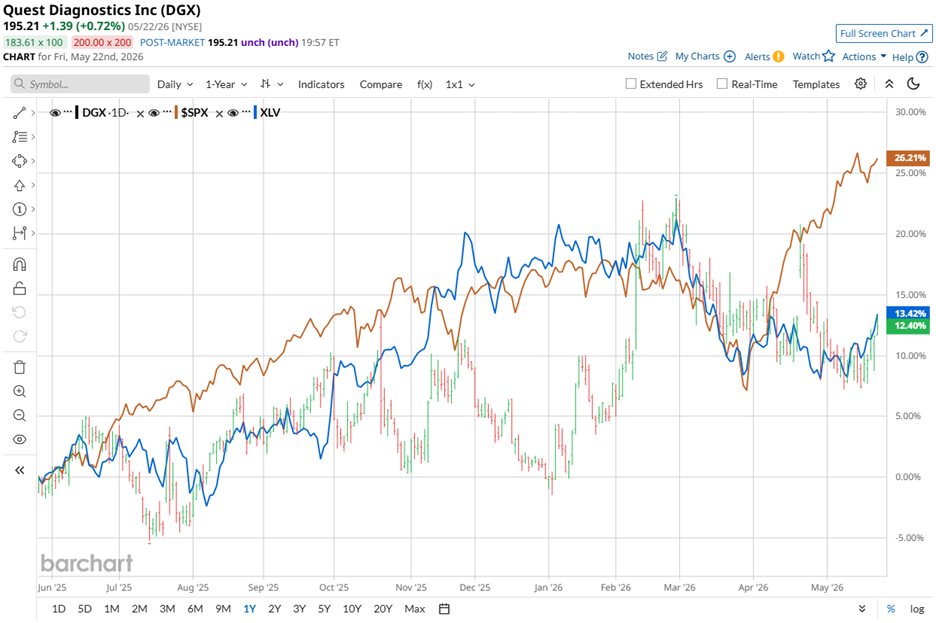

The nearly $21.6 billion market cap healthcare heavyweight has kept investors on their toes. Shares of Quest Diagnostics climbed 15.1% over the past 52 weeks, although the broader S&P 500 Index ($SPX) sprinted ahead with a 27.9% rally during the same stretch.

This year tells a different story altogether. DGX stock has jumped 12.5% year-to-date (YTD), comfortably outpacing the broader index’s 9.2% gain. Quest also managed to edge past the healthcare sector benchmark. The State Street Health Care Select Sector SPDR ETF (XLV) gained 14.8% over the last 52 weeks but lost 3.2% on a YTD basis.

On April 21, the stock added another 4.5% after Quest Diagnostics rolled out its Q1 FY2026 earnings results. Revenue climbed 9.2% year over year to $2.9 billion, sailing past analyst expectations of $2.82 billion. Adjusted EPS reached $2.50, up 13.1% from last year’s figure while also topping the Street’s $2.37 forecast.

The company rode a strong wave of demand for its clinical innovations while planting fresh flags in areas such as end stage renal disease and brain health. Automation along with artificial intelligence (AI) also greased the wheels through productivity improvements.

Quest Diagnostics now appears ready to keep the pedal to the metal. For full FY2026, management expects revenue between $11.78 billion and $11.90 billion, which translates to growth of 6.8% to 7.8%. Adjusted EPS could land between $10.63 and $10.83.

On the other hand, Wall Street expects diluted EPS for FY2026, ending in December, to rise another 8.8% year over year to $10.72. Quest has also earned a reputation for slipping past analyst expectations, having beaten EPS estimates in each of the last four quarters.

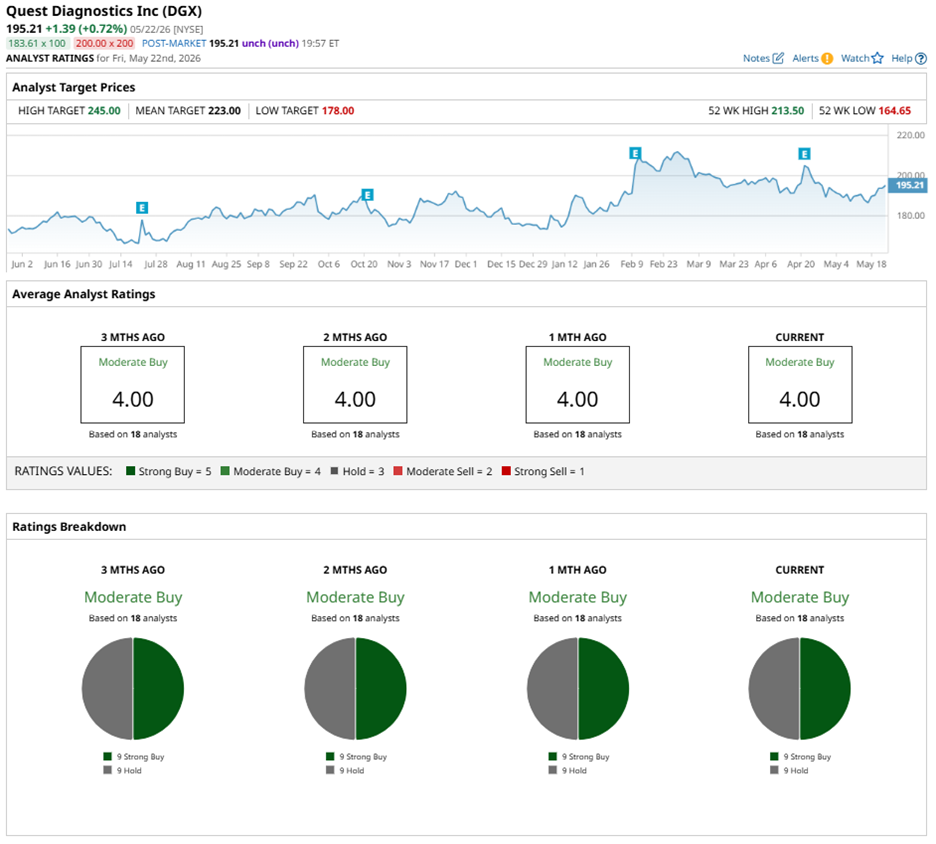

Wall Street seems happy to keep Quest Diagnostics in its good books as DGX stock is carrying an overall rating of “Moderate Buy.” Among 18 analysts tracking the stock, nine have planted their flag on a “Strong Buy” rating, while the remaining nine prefer to stay cautious with “Hold” calls.

Analyst sentiment has stayed steady as a rock over the past three months. Back then, nine analysts also tagged DGX stock with a “Strong Buy” rating, showing Wall Street has not changed its tune on the stock.

Analysts shuffled their targets after the company’s first quarter numbers hit the tape. On April 22, Baird lifted its price target on DGX stock to $229 from $224 while sticking with a “Neutral” rating after updating its model following the earnings report.

Barclays analyst Luke Sergott also stayed firmly in the bull camp the same day, backing the stock with a “Buy” rating and a $230 price target.

Even after the revised forecasts, analysts still believe DGX stock has room to run. The average price target of $223 points to potential upside of 14.2%. Meanwhile, the Street high target of $245 suggests the stock could climb another 25.5% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Investors Pile Into Tesla Call Options in Huge, Unusual Volume - a Bullish Signal?

- Dear Apple Stock Fans, Mark Your Calendars for June 18

- Billionaire Philippe Laffont Is Betting Big on ASML Stock as UBS Declares It the ‘Top Chip Stock’ in Europe

- Telecom Stocks Are Surging Ahead of the SpaceX IPO. This Chart Reminds Us All Rockets Come Crashing Back to Earth Eventually.