What a brutal six months it’s been for Pilgrim's Pride. The stock has dropped 30.4% and now trades at $27.77, rattling many shareholders. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Pilgrim's Pride, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Pilgrim's Pride Not Exciting?

Even with the cheaper entry price, we’re cautious about Pilgrim's Pride. Here are three reasons why there are better opportunities than PPC, plus one stock we’d rather own.

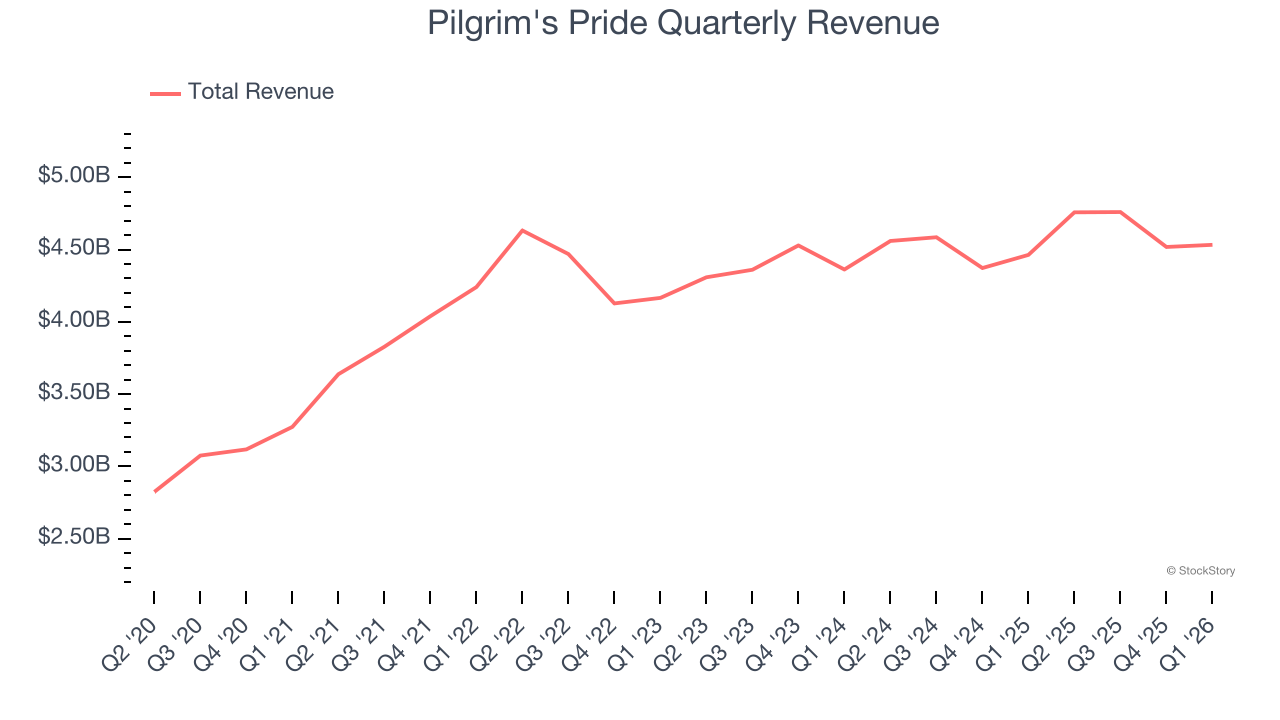

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Pilgrim's Pride grew its sales at a sluggish 2.2% compounded annual growth rate. This fell short of our benchmarks.

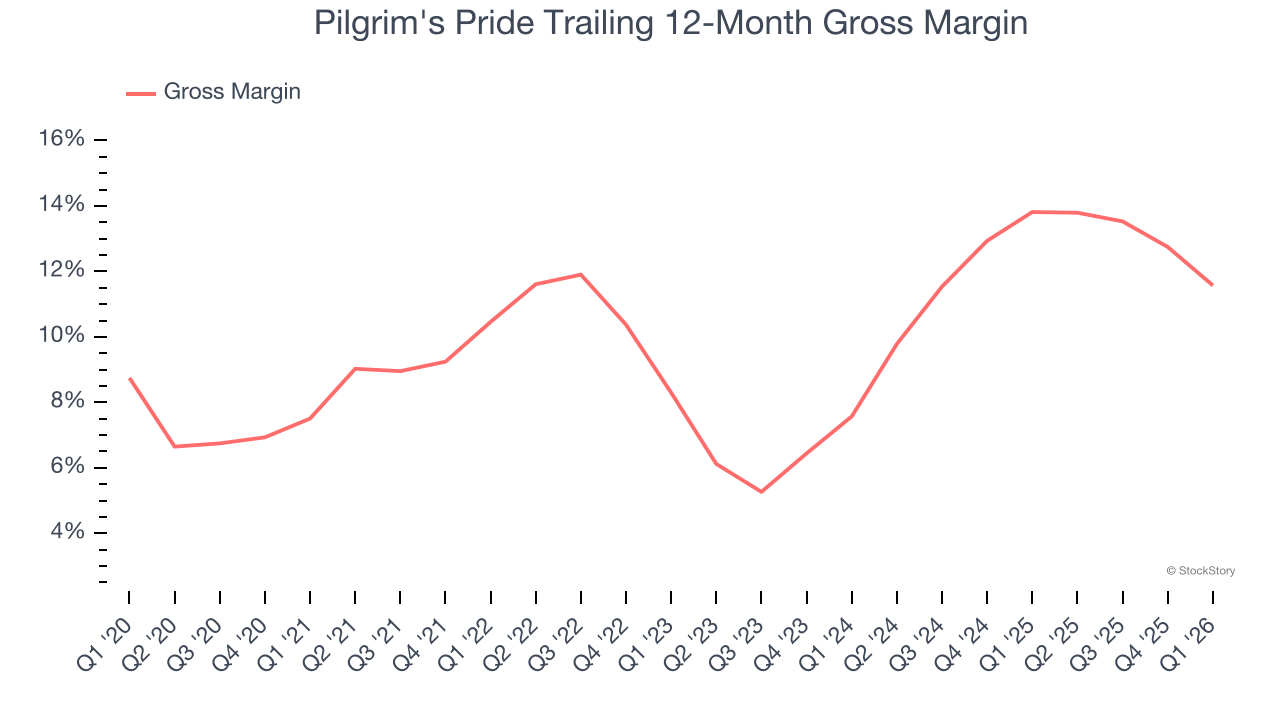

2. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Pilgrim's Pride has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 12.7% gross margin over the last two years. That means Pilgrim's Pride paid its suppliers a lot of money ($87.32 for every $100 in revenue) to run its business.

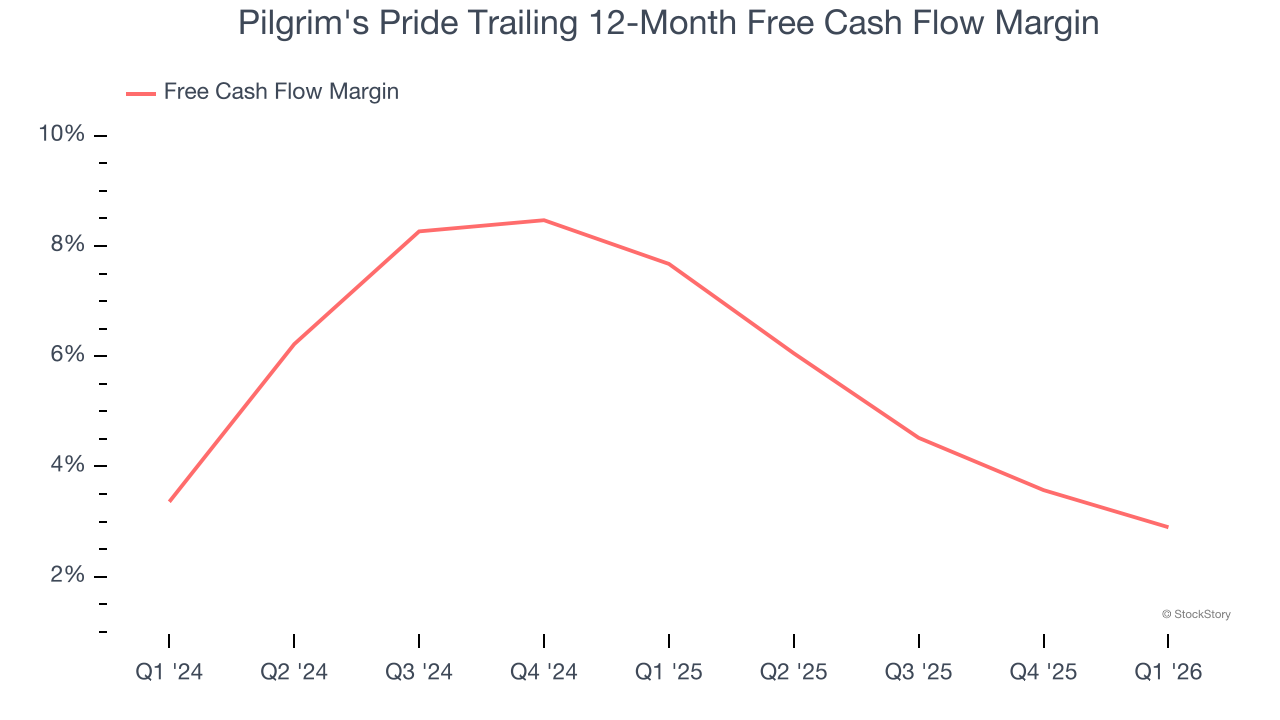

3. Free Cash Flow Margin Dropping

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Pilgrim's Pride’s margin dropped by 4.8 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity. Pilgrim's Pride’s free cash flow margin for the trailing 12 months was 2.9%.

Final Judgment

Pilgrim's Pride isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 8× forward P/E (or $27.77 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We’re pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.