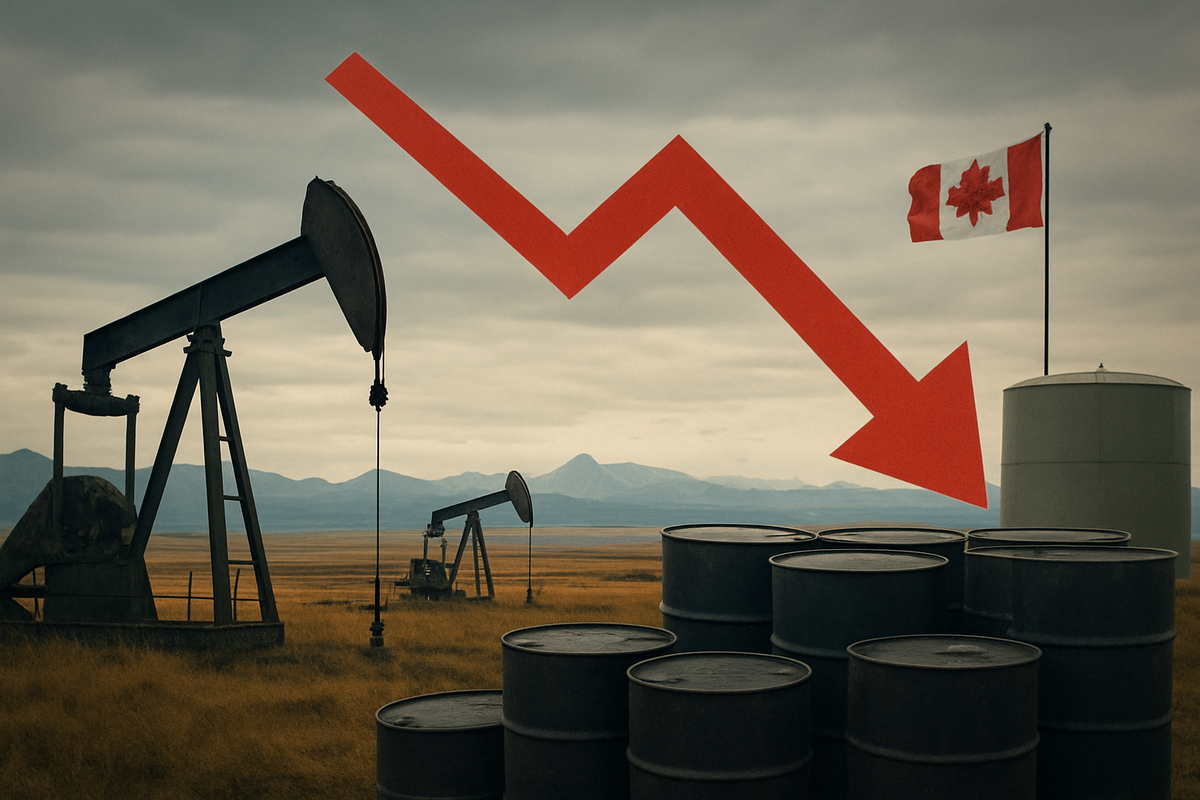

Canadian crude oil prices have recently plummeted to their weakest levels since March, sending ripples of concern through the nation's energy sector and provincial treasuries. This significant downturn is primarily a consequence of a burgeoning global oversupply of crude and a concurrent surge in oil production from Alberta, creating a challenging environment for one of Canada's most vital industries. The immediate implications are stark: a direct hit to Alberta's royalty-dependent budget, a drag on the national GDP, and a palpable "chill" in investment across the oil patch, signaling a period of intensified fiscal strain and strategic re-evaluation.

The price slump is rooted in a complex interplay of international and domestic factors. Globally, the International Energy Agency (IEA) has projected a widening gap between supply and demand, with global supply expected to outstrip demand by a record 4 million barrels per day in the coming year. This oversupply has been significantly influenced by the Organization of the Petroleum Exporting Countries and its allies (OPEC+), which, despite warnings of a looming glut, have agreed to consistent output increases throughout 2025. For instance, OPEC+ boosted output by 137,000 barrels per day starting in October and continued accelerated hikes in May and June. Simultaneously, weak global demand, fueled by economic anxieties in major economies like the United States and China, further exacerbates the oversupply issue. Domestically, Canada's oil-rich province of Alberta has seen its own production surge, with oilsands output reaching 4.19 million barrels per day in March 2025, up from 4.04 million in 2024. This increased domestic output, combined with the global market conditions, has intensified the downward pressure on Canadian crude prices.

A Detailed Look at the Downturn: Prices, Timeline, and Key Players

The "recent tumble" in Canadian crude oil prices refers to a period where benchmark prices have fallen considerably from earlier 2025 levels. The North American benchmark, West Texas Intermediate (WTI), fell from approximately US$70 at the start of 2025 to less than US$60 by November 2025. Specifically, WTI dropped to as low as US$60.45 per barrel by April 4, 2025, and continued to shed over 20% by early May, reaching nearly US$55 per barrel. As of December 3, 2025, WTI crude oil futures edged higher toward US$59 per barrel but had fallen 2.31% over the past month. Western Canadian Select (WCS), Canada's heavy crude blend, typically trades at a discount to WTI due to quality and transportation costs. This WCS discount to WTI widened significantly, reaching its weakest point relative to the U.S. benchmark since March 2025, settling at US$12.75 below WTI on December 1, 2025, and further widening to US$13 below WTI by December 3, 2025.

The timeline leading up to this downturn is marked by several key events throughout 2025. Early in the year, WTI began around US$70, but by March, Canadian crude started showing relative weakness. April proved critical, with fears of a "tariff-driven recession" and a "surprise announcement" from OPEC+ to increase production, reversing earlier cuts and raising oversupply concerns. May saw OPEC+ continue to accelerate output hikes, further intensifying global oversupply fears, alongside the U.S. administration's threatened 10% tariffs on Canadian oil and gas exports, which created significant market uncertainty. By September, OPEC+, led by Saudi Arabia and Russia, agreed to boost production by 137,000 barrels per day, contributing to warnings from the IEA that global supply could exceed demand by as much as 500,000 barrels per day.

Key players in this unfolding scenario include OPEC+, whose production decisions significantly influence global supply; major Canadian oil companies such as Suncor Energy (TSX: SU), Imperial Oil (TSX: IMO), Cenovus Energy (TSX: CVE), and Canadian Natural Resources (TSX: CNQ), who are directly impacted by price fluctuations; and governments, particularly the U.S. government, whose trade policies have created market uncertainty, and the Canadian provincial governments (e.g., Alberta), which face substantial financial challenges due to reliance on oil revenues. The initial market reactions beyond just price changes included workforce reductions (e.g., Imperial Oil eliminating 900 jobs), a "chill in investment" across the sector, and a significant hit to Canadian energy stocks, with the TSX energy index closing down 8.7% on April 4, 2025. Despite the downturn, Canadian oilsands producers have largely maintained or even increased output due to the long-lived nature of their assets and improved pipeline capacity, notably with the Trans Mountain Pipeline expansion providing crucial new market access.

Companies Navigating the Storm: Winners and Losers

The tumbling Canadian crude oil prices and the widening Western Canadian Select (WCS) differential present a mixed bag for public companies within the Canadian oil and gas sector. While most upstream producers face significant headwinds, integrated companies and midstream operators demonstrate varying degrees of resilience.

Upstream Producers, whose revenues are directly tied to the realized price of their crude, are typically the biggest losers. Companies like Cenovus Energy (TSX: CVE) and Canadian Natural Resources (TSX: CNQ), with significant exposure to WCS-based pricing and upstream operations, will see their revenue directly decline as both the overall crude price falls and the discount for Canadian heavy oil widens. Profit margins will be severely squeezed, potentially leading to losses, as extraction and transportation costs remain relatively constant. This scenario often triggers significant capital expenditure cuts, deferring new projects to preserve liquidity. While CNQ has demonstrated resilience with a strong balance sheet, a sustained widening of the differential beyond typical ranges would still negatively impact their robust profit and record production levels.

Integrated Companies, which combine upstream (production) and downstream (refining and marketing) operations, are generally better positioned to mitigate losses. Companies such as Imperial Oil (TSX: IMO) and Suncor Energy (TSX: SU) benefit from their refining assets, which can capitalize on cheaper, discounted WCS crude as feedstock. While their upstream revenue would decline, the downstream segment could see improved margins, partially offsetting the upstream losses and providing a hedge against commodity price volatility. For instance, Imperial Oil reported increased profit in Q1 2025 despite lower upstream production, partly due to a narrowing WTI/WCS spread benefiting upstream, while downstream remained profitable. If the differential widened, the downstream segment would benefit from cheaper feedstock, demonstrating its resilience. Suncor, with approximately 40% exposure to WCS pricing and a similar contribution from Synthetic Crude Oil (SCO) which trades at par with WTI, also leverages its refining operations to stabilize overall profitability.

Midstream Operators, primarily involved in transportation and storage, often operate on fee-for-service models, making them relatively more resilient. Companies like Enbridge (TSX: ENB), with diversified pipeline networks, generate stable income regardless of crude oil prices or differentials. Their revenues are largely based on contracted volumes and fees. While a prolonged period of extremely low prices could lead to production curtailments and eventually impact throughput volumes, midstream operators are generally considered "safer" investments during commodity price volatility. TC Energy (TSX: TRP), having strategically exited its oil pipeline business to focus on natural gas and power generation, would experience minimal direct impact from tumbling Canadian crude oil prices and widening WCS differentials, as its focus is now on gas pipelines. The recent start-up of the Trans Mountain Expansion (TMX) pipeline, however, is a key development that has been working to narrow the WCS differential, offering some relief to Canadian heavy oil producers and supporting the long-term viability of crude transportation.

Wider Significance: Trends, Ripple Effects, and Policy

The tumbling prices of Canadian crude oil, driven by a global supply glut and surging Alberta production, carry significant wider implications for the energy industry, Canada's economy, international trade relationships, and future policy decisions. This event highlights crucial broader industry trends, creates ripple effects on both competitors and partners, necessitates regulatory and policy considerations for Canada, and draws parallels with historical market fluctuations.

This downturn is part of a larger narrative of global oil market dynamics, characterized by a persistent supply glut and slowing global demand due to economic uncertainty. The quality differential between WCS and global benchmarks like WTI continues to be a persistent factor, with WCS consistently trading at a discount due exacerbated by higher natural gas prices (increasing refining costs for sour crudes) and an influx of heavier OPEC barrels. While the Trans Mountain Expansion Project (TMEP) has significantly increased export capacity, surging Alberta production can still lead to rationing of export pipeline systems. The co-dependence between the US and Canadian oil industries is also critical, with nearly 98% of Canada's exported oil processed by US refineries. Any strategic shift by Canada to diversify exports could significantly threaten US energy security.

The ripple effects are profound. For Canadian producers, low prices mean reduced profits, spending cuts, and a "chill" in investment. For the Canadian economy, especially Alberta, the net effect is negative, with provincial budgets facing significant blows; a US$1 drop in WTI can translate to a C$750 million hit to Alberta's treasury. While US refineries have historically benefited from discounted Canadian oil, potential US tariffs could erode margins. Globally, OPEC+ continues its strategy of maintaining market share by keeping prices low, disincentivizing investment in higher-cost regions. Conversely, consumers generally benefit from lower gasoline prices.

This situation presents several critical regulatory and policy implications for Canada. Past periods of extreme price differentials have seen the Alberta government implement mandatory production cuts, a tool that remains available. There's ongoing tension between the federal government's climate change policies (e.g., emissions caps) and provincial reliance on oil and gas revenues. The 2025 federal budget signals a pivot away from a strict emissions cap towards reducing emissions per barrel, seen as less damaging to jobs and royalties. The long-term need for robust and diverse pipeline infrastructure remains paramount to ensure Canadian oil can reach global markets efficiently, reducing transportation-related discounts. Regulatory uncertainty has historically dissuaded investment, prompting calls for a "significant policy reset." Furthermore, the threat of US tariffs underscores the need for Canada to diversify its export markets beyond its overwhelming reliance on the US.

Historically, the current situation bears similarities to the 2018 production curtailment when Alberta faced a record-high price differential due to insufficient pipeline capacity, leading to mandatory production cuts. The early 2020 COVID-19 pandemic also saw widening differentials due to unprecedented demand disruptions. These events contrast sharply with the "super-cycle" of the 2000s, driven by booming demand. The 1970s oil crises also saw federal government intervention through price controls and investment in oilsands. Natural disasters like wildfires have also repeatedly caused temporary disruptions and price impacts.

What Comes Next: Navigating the Future of Canadian Oil

The Canadian crude oil industry is navigating a complex and evolving landscape, characterized by current price volatility, a global supply surplus, and increasing production, particularly from Alberta's oilsands. The future outlook for the sector involves both significant challenges and strategic opportunities, necessitating adaptation from both companies and government.

In the short term, Canadian crude oil prices are expected to remain under pressure. Global crude oil prices are forecast to decline in 2025, with West Texas Intermediate (WTI) projected to average US$66.00 per barrel and Western Canadian Select (WCS) at US$55.00 per barrel, reflecting an anticipated US$11.00 per barrel differential. This discount could widen further if U.S. import tariffs on Canadian petroleum increase. Despite price challenges, Alberta's oilsands production is projected to reach a record annual average of 3.5 million barrels per day (b/d) in 2025, a 5% increase from 2024, driven by producers optimizing existing assets and lowering break-even costs to around US$27 per barrel. The operational Trans Mountain Pipeline expansion (TMX) is crucial, rerouting Canadian oil flows towards Asia and helping to compress the WCS discount, though export capacity could again become a concern as early as next year due to projected production growth.

Looking long term, WTI prices are expected to gradually strengthen to US$76.50 by 2034, with WCS reaching US$63.50 per barrel, though this forecast relies heavily on global demand for petroleum liquid fuels, which faces uncertainty due to environmental policies. Alberta's total oil production is projected to grow to 4.7 million barrels per day by 2034, primarily from the continuous optimization of existing facilities. The industry's long-term viability is intertwined with its ability to reduce greenhouse gas emissions, with Canada committed to achieving net-zero emissions by 2050, requiring the oil and gas sector to target 31% below 2005 levels by 2030.

Strategic pivots and adaptations for companies include intense cost discipline, focusing on efficiency, and significant investment in decarbonization technologies like Carbon Capture, Utilization, and Storage (CCUS) and hydrogen production. The Pathways Alliance, comprising major oilsands companies, is committed to achieving net-zero emissions from oilsands production by 2050 via CCUS projects. For governments, recent policy adjustments, such as reportedly scrapping a planned emissions cap on the oil and gas sector in exchange for strengthened industrial carbon pricing and support for CCUS projects, aim to spur energy sector investment. Both levels of government are also focused on market diversification to reduce reliance on the U.S. market, with efforts to develop infrastructure for new markets in Asia and Europe.

Comprehensive Wrap-up: Assessing the Market and Investor Outlook

The recent tumble in Canadian crude prices, driven by a global glut and surging Alberta production, has underscored the industry's inherent volatility and its profound impact on Canada's economy. The key takeaways are clear: a persistent global oversupply, coupled with weakening demand, has depressed WTI prices and widened the WCS differential. This has led to immediate financial strains on Alberta's budget, a dampening effect on the national GDP, and a "chill" in investment across the oil patch.

Moving forward, the market will likely remain characterized by continued price volatility, influenced heavily by OPEC+ decisions, global economic health, and geopolitical developments. However, the Trans Mountain Pipeline expansion (TMX) is a critical game-changer, providing enhanced takeaway capacity and crucial access to Pacific markets, which should help mitigate historical price discounts for Canadian crude. The industry's long-term viability is increasingly tied to its commitment to decarbonization efforts, with significant investments in CCUS and hydrogen production becoming essential for maintaining competitiveness in a carbon-constrained world.

The lasting impact of these challenges is driving a fundamental transformation within the Canadian energy sector. There is an intensified focus on cost efficiency, operational resilience, and technological innovation to balance economic contribution with environmental stewardship. This strategic pivot aims to ensure long-term viability, positioning Canada's energy sector at a critical juncture where growth and sustainability must converge.

For investors, the coming months demand a vigilant and strategic approach:

- Monitor Global Supply and Demand: Closely track decisions by OPEC+ regarding production quotas, as well as supply growth from major non-OPEC producers. Be mindful of global economic indicators and recession fears, which directly influence oil demand.

- Watch Geopolitical Developments: Pay attention to U.S. trade policy and any escalating geopolitical tensions, as these can introduce significant price volatility and directly impact market sentiment.

- Assess Canadian Export Infrastructure: The performance and operational ramp-up of the Trans Mountain Pipeline expansion (TMX) will be crucial for Canadian crude differentials. Similarly, monitor progress on new LNG export facilities on the West Coast, which could provide a substantial boost to natural gas producers.

- Evaluate Company Fundamentals: Favor companies demonstrating robust financial health, a strong focus on cost optimization, and disciplined capital expenditure plans. Dividend-paying energy stocks with solid balance sheets might offer a degree of stability amidst market fluctuations.

- Consider Natural Gas Opportunities: The natural gas segment of the Canadian energy market appears to have strong tailwinds, particularly from burgeoning LNG exports and domestic demand driven by data center development.

- Prioritize ESG and Innovation: Look for companies actively investing in environmental, social, and governance (ESG) initiatives, particularly those developing and adopting decarbonization technologies. These companies are better positioned for long-term sustainability and may mitigate regulatory and reputational risks.

- Keep an Eye on Broader Economic Indicators: General economic growth, inflation rates, and the monetary policy decisions of the Bank of Canada and the U.S. Federal Reserve will continue to shape the overall investment climate and energy demand.

By carefully evaluating these factors, investors can better position themselves to navigate the evolving Canadian crude oil market in the coming months and capitalize on emerging opportunities while mitigating risks.

This content is intended for informational purposes only and is not financial advice