Steel wire manufacturer Insteel (NYSE: IIIN) will be reporting results this Thursday before the bell. Here’s what to look for.

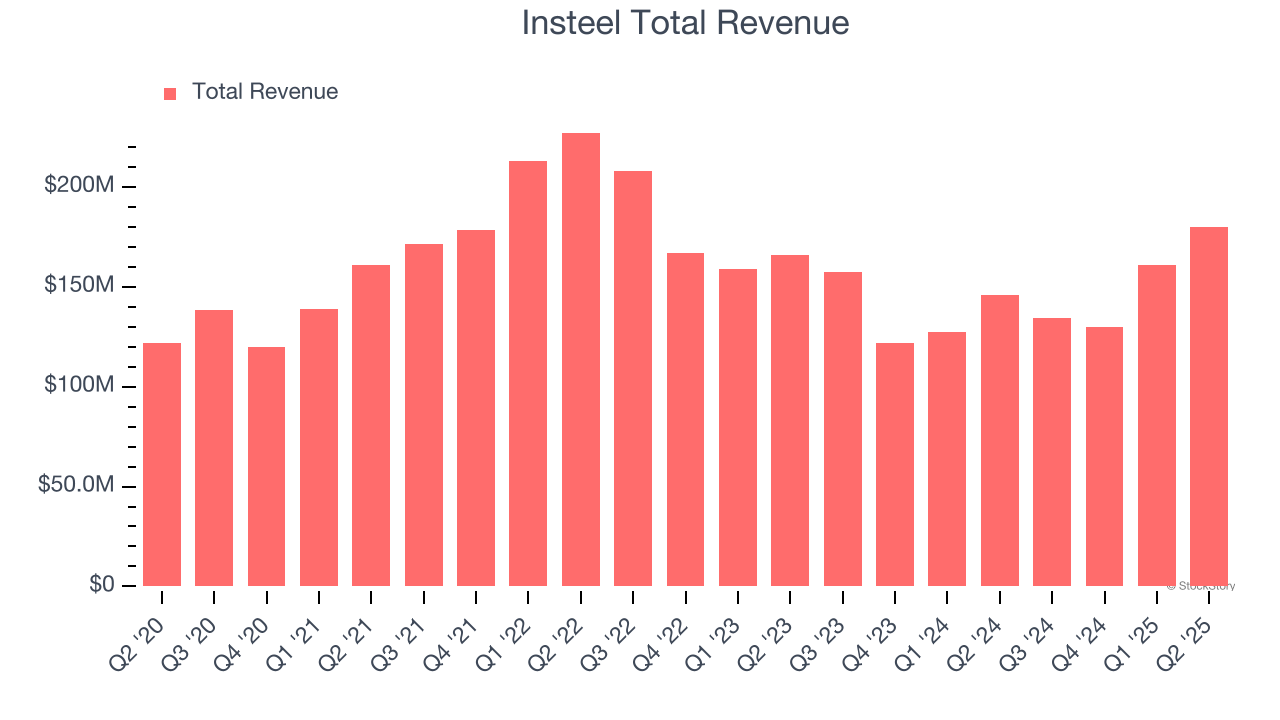

Insteel beat analysts’ revenue expectations by 2.2% last quarter, reporting revenues of $179.9 million, up 23.4% year on year. It was an exceptional quarter for the company, with an impressive beat of analysts’ EBITDA estimates and a beat of analysts’ EPS estimates.

Is Insteel a buy or sell going into earnings? Read our full analysis here, it’s free for active Edge members.

This quarter, analysts are expecting Insteel’s revenue to grow 34.7% year on year to $181 million, a reversal from the 14.7% decrease it recorded in the same quarter last year. Adjusted earnings are expected to come in at $0.79 per share.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. Insteel has a history of exceeding Wall Street’s expectations, beating revenue estimates every single time since going public by 6.6% on average.

Looking at Insteel’s peers in the building products segment, some have already reported their Q3 results, giving us a hint as to what we can expect. Apogee delivered year-on-year revenue growth of 4.6%, beating analysts’ expectations by 2.1%, and AZZ reported revenues up 2%, falling short of estimates by 2.1%. Apogee traded down 4.5% following the results while AZZ was also down 4.9%.

Read our full analysis of Apogee’s results here and AZZ’s results here.

There has been positive sentiment among investors in the building products segment, with share prices up 2.2% on average over the last month. Insteel is down 3.2% during the same time and is heading into earnings with an average analyst price target of $39 (compared to the current share price of $37.40).

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.