Welding and cutting equipment manufacturer ESAB (NYSE: ESAB) will be reporting earnings tomorrow before the bell. Here’s what to look for.

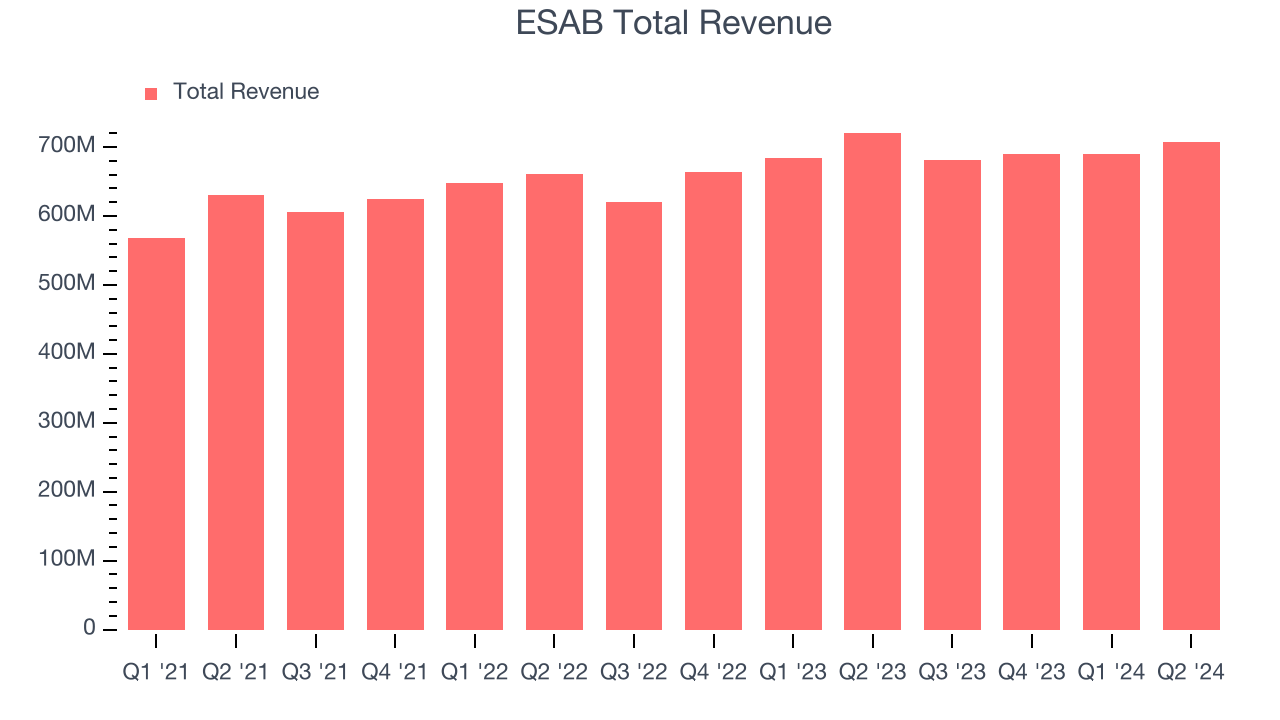

ESAB beat analysts’ revenue expectations by 2.6% last quarter, reporting revenues of $707.1 million, down 1.9% year on year. It was a strong quarter for the company, with an impressive beat of analysts’ EBITDA estimates.

Is ESAB a buy or sell going into earnings? Read our full analysis here, it’s free.

This quarter, analysts are expecting ESAB’s revenue to decline 8.9% year on year to $620.4 million, a reversal from the 9.8% increase it recorded in the same quarter last year. Adjusted earnings are expected to come in at $1.12 per share.

Heading into earnings, analysts covering the company have grown increasingly bearish with revenue estimates seeing 5 downward revisions over the last 30 days (we track 7 analysts). ESAB has a history of exceeding Wall Street’s expectations, beating revenue estimates every single time over the past two years by 7.5% on average.

Looking at ESAB’s peers in the industrial machinery segment, some have already reported their Q3 results, giving us a hint as to what we can expect. Snap-on posted flat year-on-year revenue, beating analysts’ expectations by 7.8%, and John Bean reported revenues up 12.4%, topping estimates by 2.6%. Snap-on traded up 9.4% following the results while John Bean was also up 17.8%.

Read our full analysis of Snap-on’s results here and John Bean’s results here.

Investors in the industrial machinery segment have had fairly steady hands going into earnings, with share prices down 1.1% on average over the last month. ESAB is up 3.5% during the same time and is heading into earnings with an average analyst price target of $116 (compared to the current share price of $110.04).

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.