It's been another outstanding year for the Nasdaq-100 Index (QQQ), with the ETF up more than 28% year-to-date, despite lapping a 47% return in 2020. This solid performance has been helped by a 67% return for Alphabet (GOOG) and a 53% return from Microsoft (MSFT), with both continuing to melt higher in December. However, with several names putting up strong returns, it's becoming harder to find value in the tech space, with some weaker names being value traps. In this update, we'll look at two steady earnings growers trading at attractive valuations that are worthy of consideration:

(Source: TC2000.com)

The Nasdaq-100 has been in a steady uptrend since March 2020, but two names that haven't really participated in the relentless rally are Norton LifeLock (NLOK) and CGI Group (GIB). These two names are up 9% and 24% since August 2020, lagging behind the QQQ's 43% return. The good news is that this underperformance has left both names very reasonably valued, with CGI Group trading at 17x FY2023 earnings estimates and NLOK trading at less than 14x FY2023 earnings estimates. These represent meaningful discounts to their historical earnings multiples of 20 and 17, respectively. Let's take a closer look below:

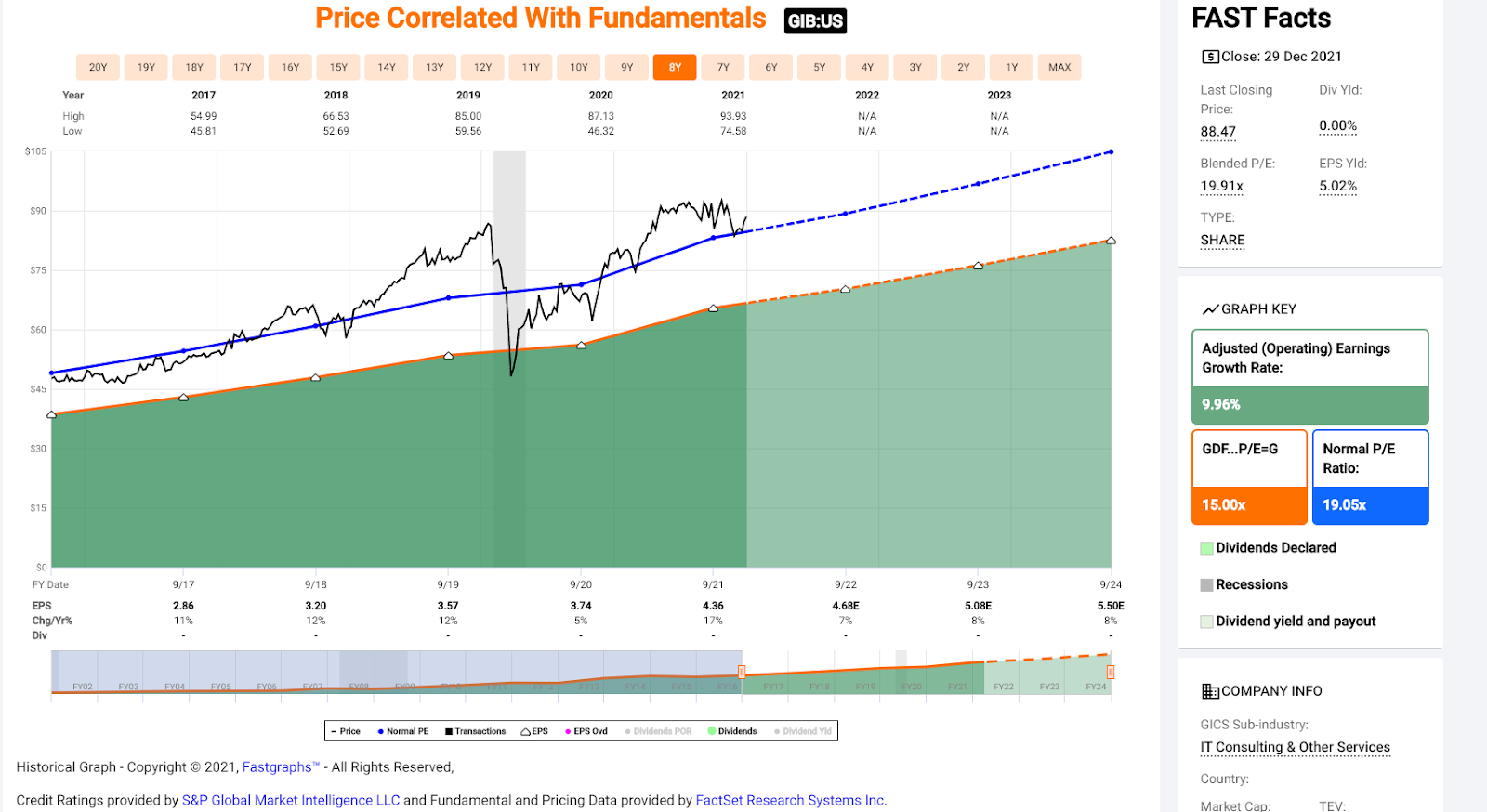

Beginning with CGI Group, it is a multinational informational technology consulting & systems integration firm based out of Canada. The company has enjoyed steady growth in annual earnings per share over the past several years, growing annual EPS from $3.13 in FY2015 to estimates of $4.61 in FY2022. While this 7% growth rate certainly pales in comparison to the industry average, the stock is attractively valued, trading at just 17x FY2023 earnings estimates of $5.08 at a share price of $88.00.

(Source: FASTGraphs.com)

During its most recent quarter, it saw 3% revenue growth year-over-year, or 6% on a constant currency basis. While this mid-single-digit growth rate leaves a lot to be desired, EPS was up 15% year-over-year, with EBIT margins up 80 basis points to 7.8%. Meanwhile, the company has continued to reduce its net debt, with net debt to market cap expected to dip below 25% last year, a major improvement from the height of the pandemic.

With a new acquisition under the company's belt after acquiring Unico, a technology consultancy and systems integrator in Australia, and scooping up Cognicase Management Consulting in October, the company should have a strong year ahead and continues to invest in its business to gain market share. Based on what I believe to be a fair earnings multiple of 21, I see a fair value for the stock of $107.00. Generally, I prefer at least a 25% discount to fair value, suggesting that the stock would become interesting on any dip below $80.50.

(Source: TC2000.com)

Finally, looking at the technical picture, we can see that CGI has spent the past several months consolidating, allowing its monthly moving average to play catch-up. Outside of the market crash in Q1 2020, pullbacks to this moving average have presented great buying opportunities, and I wouldn't expect this time to be any different. So, if we do see CGI pullback below $80.50, where it would trade at less than 16x FY2023 earnings estimates and test this moving average, I would view this as a low-risk area to start a position.

Norton LifeLock is the next stock worth keeping an eye on, an American software company formerly known as Symantec. The company has a market cap of $15BB, is a global leader in consumer cyber safety, and is also a steady earnings growth story. This is evidenced by the company's ability to nearly double earnings since FY2015 despite heated competition in the space (FY2022 annual EPS estimates of $1.73 vs. $0.97 in FY2015).

(Source: FASTGraphs.com)

During Norton's most recent quarter, the company reported 11% revenue growth and 19% earnings growth, benefiting from a 200-basis point increase in operating margins. The company also saw meaningful growth in its direct customer count in fiscal Q2 2022, adding 178,000 members sequentially and 2.6MM members since fiscal Q2 2021. In addition to its core offerings, Norton recently launched AntiTrack, a privacy offering that helps people protect their digital footprints from websites that track online activity and personal data. This allows for faster browsing, tracker cookie blocking, and anti-fingerprint capabilities.

In addition to AntiTrack, the new family plan also allows parents to be alerted if their children's device heads outside of what are determined to be safe zones or receive automatic check-in alerts from the location of their child's device. While this may seem over-reaching, it should see a strong sell-through, with this being one of the only offerings on the market to help monitor one's children by their device.

As shown in the chart above, NLOK is expected to see 20% annual EPS growth in FY2022 and has seen a strong turnaround since FY2018. This would mark a new all-time high for annual EPS, with further gains ahead in FY2023. Despite this meaningful recovery from a sharp earnings slowdown in FY2019 ($0.60 vs. $1.67), NLOK looks very reasonably valued, trading at less than 14x FY2023 earnings estimated. Based on what I believe to be a conservative earnings multiple of 17, this points to upside to $32.50, more than 25% upside from current levels.

(Source: TC2000.com)

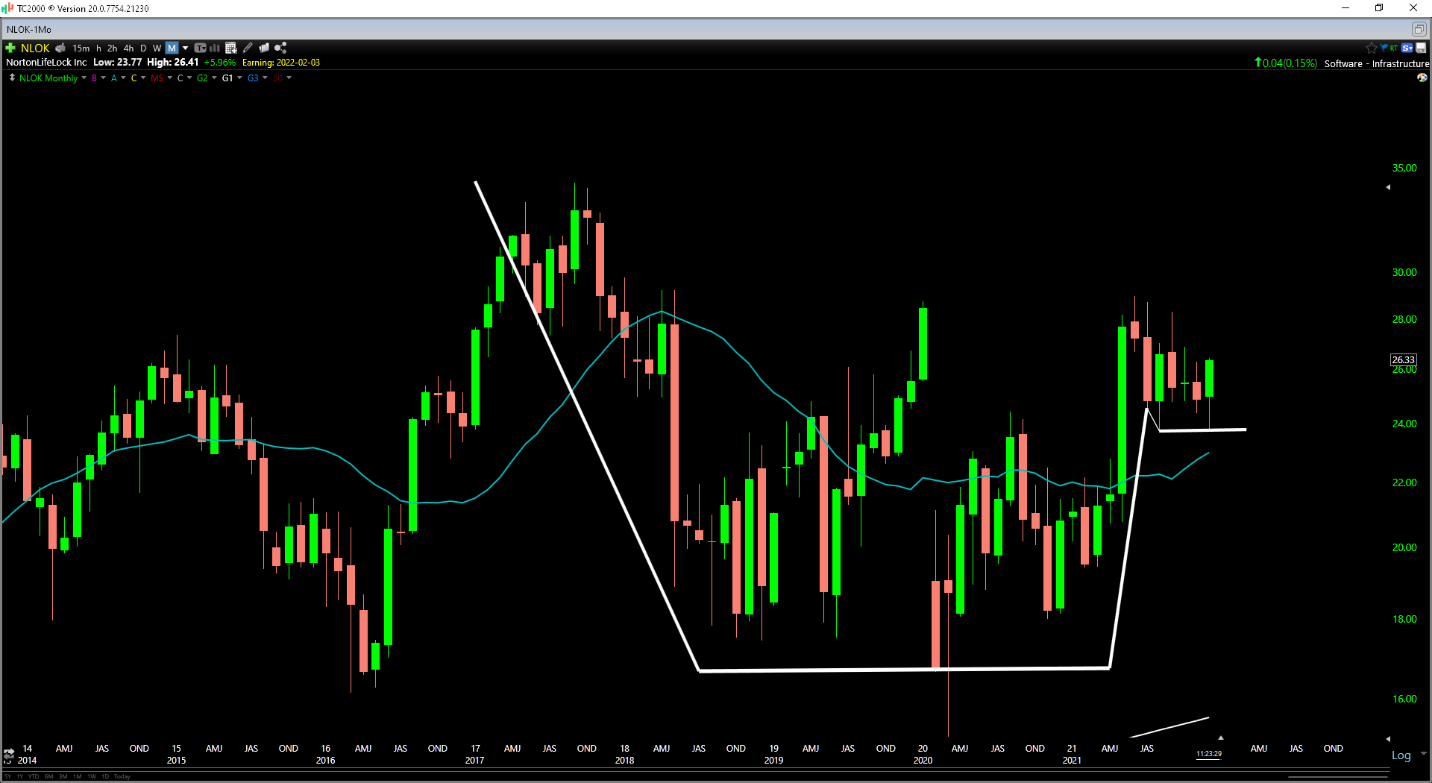

Looking at NLOK's technical chart, we can see that the stock appears to be building a massive cup & handle base and appears to turn up within this handle as of December's monthly close. With momentum back in favor of the stock, and meaningful upside to fair value, I would view any pullbacks below $25.75 as low-risk buying opportunities.

NLOK and GIB may not be the most exciting growth stories in the tech space, but they are two opportunities to buy steady earnings growth at a reasonable price, which is not easy after another solid year for the Nasdaq-100. With both NLOK and GIB trading at attractive valuations and looking like they have limited downside from a technical standpoint, I would view any pullbacks below $80.50 and $25.75 as low-risk areas to start a position in each name.

Disclosure: I have no positions in any stocks mentioned

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

MSFT shares were trading at $341.03 per share on Thursday afternoon, down $0.92 (-0.27%). Year-to-date, MSFT has gained 54.61%, versus a 29.63% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 2 Tech Stocks With Promising Prospects in 2022 appeared first on StockNews.com