Bloomin' Brands, Inc. (BLMN) in Tampa, Fla., owns casual, upscale, and fine dining restaurants, operating through the two broad U.S. and international segments. Its restaurant portfolio has four primary segments: Outback Steakhouse, Carrabba’s Italian Grill, Bonefish Grill, and Fleming’s Prime Steakhouse & Wine Bar.

Despite inflationary headwinds, BLMN posted higher sales and higher profits in its fiscal first quarter. The company boosted its sales through digital channels and used technology to enhance its efficiency. Also, BLMN’s Outback Steakhouse segment unveiled a new prototype and opened one of the first restaurants following its design in Charlotte's Steele Creek area. The Australian-themed dining chain plans to build 75-100 restaurants in the United States and incorporate the latest prototype elements in its existing locations.

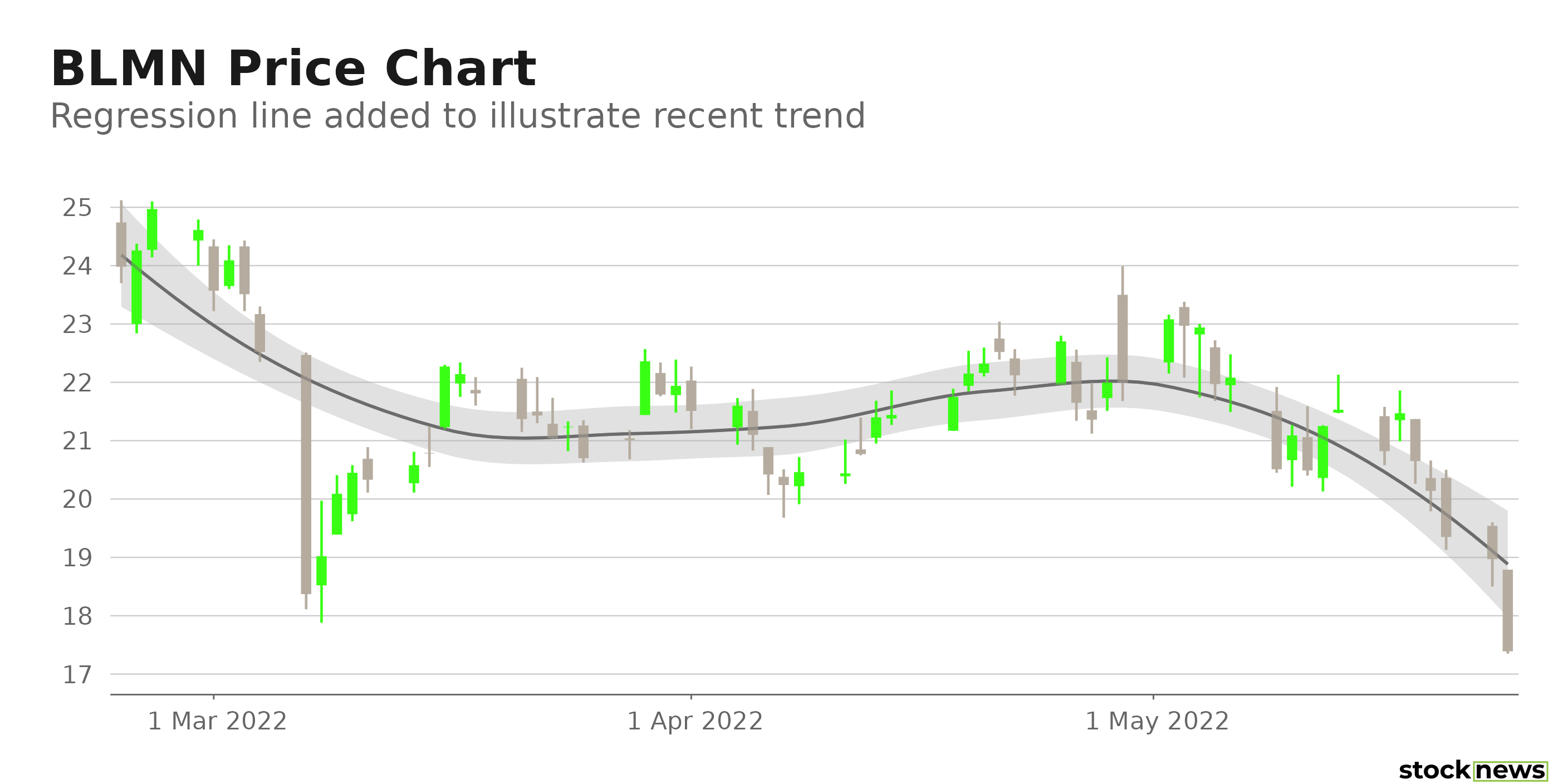

However, BLMN’s stock has declined 9.6% in price year-to-date and 14.2% over the past month to close yesterday’s trading session at $18.97. But the stock appears undervalued at its current price. In terms of its forward non-GAAP P/E, BLMN is currently trading at 7.62x, which is 32.6% lower than the 11.30x industry average. The stock’s 0.38 forward Price/Sales multiple is 55.9% lower than the 0.87 industry average. And in terms of its forward Price/Cash Flow, it is trading at 4.13x, which is 52.8% lower than the 8.76x industry average.

Here are the factors that might affect BLMN’s performance in the near term:

Sound Financials

For its fiscal first quarter, ended March 27, 2022, BLMN’s total revenues increased 15.5% year-over-year to $1.14 billion. Its income from operations rose 17.9% from the prior-year quarter to $107.26 million. And its net income attributable to BLMN and adjusted EPS improved 9.7% and 11.1%, respectively, from the same period the prior year to $75.51 million and $0.80.

Favorable Profit Margins

BLMN’s 6.11% trailing 12-month levered FCF margin is 63% higher than the 3.75% industry average. Its trailing 12-month ROE, ROTC, and ROA of 134.60%, 8.92%, and 6.94%, respectively, are 668.2%, 20%, and 14.5% higher than their industry averages of 17.52%, 7.43%, and 6.06%.

Stable Growth Story

BLMN’s revenue and EBITDA have grown at 1.1% and 10.3% respective CAGRs over the past three years. While its net income, EPS, and levered FCF have grown at CAGRs of 28%, 22.4%, and 27.6%, respectively, over the past three years.

Wall Street Analysts Sees Potential Upside

Among the six Wall Street analysts rating the stock, four have rated it Buy, while two have rated it Hold. The $30.17, 12-month median price target indicates a 59% potential upside. The price targets range from a low of $24.00 to a high of $36.00.

POWR Ratings Reflect Promising Prospects

BLMN’s strong fundamentals are reflected in its POWR Ratings. The stock has an overall B rating, which equates to Buy in our proprietary rating system. The POWR Ratings are calculated by considering 118 different factors, with each factor weighted to an optimal degree.

BLMN has a Value grade of A in sync with its attractive valuations. The stock has a B grade for Quality, consistent with its wide profit margins.

Among the 44-stock Restaurants industry, BLMN is ranked #9. The industry is rated B.

Click here to see the additional POWR Ratings for BLMN (Growth, Momentum, Stability, and Sentiment).

Bottom Line

The company has shown resilience in the face of rising inflation. Furthermore, its new prototype for the Outback Steakhouse segment should be profitable for the company. Also, the stock seems to be trading at a discount, and Street analysts see significant upside potential in the stock. Hence, I think BLMN might be a solid addition to one’s portfolio now.

How Does Bloomin' Brands, Inc. (BLMN) Stack Up Against its Peers?

While BLMN has an overall POWR Rating of B, one might consider looking at its industry peers, Good Times Restaurants Inc. (GTIM) and Nathan’s Famous, Inc. (NATH), which has an overall A (Strong Buy) rating, and Arcos Dorados Holdings Inc. (ARCO) and The ONE Group Hospitality, Inc. (STKS), which have an overall B (Buy) rating.

BLMN shares were trading at $17.35 per share on Tuesday afternoon, down $1.62 (-8.54%). Year-to-date, BLMN has declined -16.26%, versus a -17.76% rise in the benchmark S&P 500 index during the same period.

About the Author: Anushka Dutta

Anushka is an analyst whose interest in understanding the impact of broader economic changes on financial markets motivated her to pursue a career in investment research.

The post Bloomin’ Brands: Attractive Valuation Make This Stock a Buy Now appeared first on StockNews.com