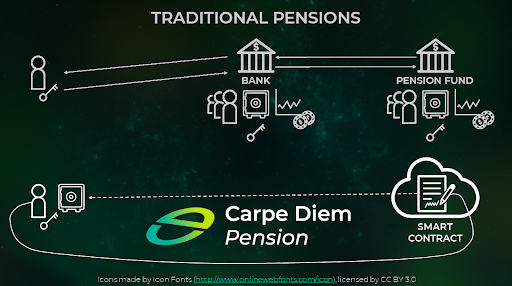

Bottighofen, Switzerland, 27th February 2024, ZEX PR WIRE, On January 1st, 2024, Carpe Diem Pension came to life. This is a new way to build an alternative pension without the need for intermediates (banks & pension funds). It operates autonomously through the CDP token on the Pulse blockchain.

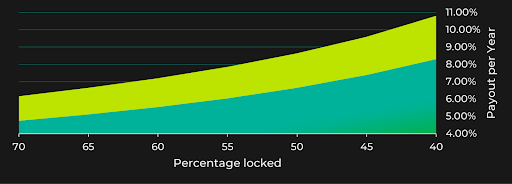

People build up their pension collateral by making a monthly deposit in CDP. The accrued collateral is bound to their accounts and cannot be withdrawn. This permanent collateral cannot be touched by anyone, meaning that it cannot be used by the program to pay out others, or to gamble on investments. At the time of writing, the yearly payout percentage is about 9%. This is paid from the yearly inflation rate of 4.32%. As not all CDP is locked, the payout percentage is higher than the inflation rate. There’s no need for a company to make profits or for new people entering the system to pay out users.

Besides being based on blockchain technology, Carpe Diem Pension invented a brand-new model for handling deposits and payouts in a robust and sustainable manner.

Robus

The program cannot be changed and runs on a giant and transparent blockchain network. This results in more resilience, predictability, and credibility.

Fair

A blockchain account is needed to participate. This account isn’t tied to personal details. Therefore, it is impossible for the program to discriminate certain groups or individuals. Every blockchain account is treated equally in the program.

Safe

Deposits in CDP aren’t going anywhere. They are locked forever and can’t be touched by anyone. This means that it cannot be used to pay out other users, nor can it be used to make investments where you have little to no influence over.

Sustainable

The program pays out through the creation of new CDP tokens. The inflation is 4.32% a year and all of it is distributed as payout to users.

No Minimum Age

Users decide themselves at what age they retire. By making a monthly deposit, they increase their pension collateral, which generates a pay out, effective immediately. When users are content with the height of this pay out, they can decide to retire. A larger monthly deposit means that it is possible to retire earlier.

Retire Wealthy

It is possible to retire with a higher pension income than your initial income. Work hard, retire wealthy.

Multi-generational

Pension incomes can be multi-generational. Hand the blockchain account over to family, and they receive your built-up pension income.

Unique referral program

For people involved in affiliate marketing, Carpe Diem Pension might be very interesting. First, let’s outline the current situation: An income can be generated through affiliate marketing by making sales for companies. For example, one can refer people to buy a lava lamp on Amazon and get a certain percentage of the sale.

It can be quite lucrative, especially when marketers manage to attract a lot of people and keep referring to new products constantly.

However, when one stops actively referring others, the income stream decreases or even stops entirely. Often, affiliate marketing is described as a way to generate a passive income, but in reality, it often isn’t “passive”.

Bottom line: each sale grants you a direct sales cut.

With the referral program of Carpe Diem Pension, marketers do not receive a direct sales cut, but instead are awarded with Pension shares. One share acts the same as one CDP token deposited by users: it generates a permanent passive payout. Marketers receive 10% in shares of the CDP tokens deposited through their link.

Marketers increase their pension payout by making more sales. When they halt their affiliate business, they receive their built-up pension payout forever.

CDP as a hybrid investment and pension fund

Pension operations, such as deposit and payout, work through the CDP token. This token is traded on the open market, and can therefore fluctuate in price against the Dollar/Euro/etc.. If the price in Dollars goes up over time, the collateral in Dollars goes up as well. This has a direct effect on the payout.

When people buy and deposit CDP forever, it reduces supply and increases demand. Usually, this results in the price going up. When people start their retirement, the payout is just a small percentage each month, which means that there isn’t a huge immediate boost of supply.

It should be noted that investing in cryptocurrencies isn’t without risk. However, trusting traditional pension funds isn’t without risk either. One can mitigate risk through diversification.

Silvan Liklikuwata, the Founder of Carpe Diem Pension, said: “My personal goal is to work hard, and save 40% of my income for retirement (half of it through Carpe Diem Pension), so I can become financially independent and retire early when I am still full of life. As a musician, I want to have the ability to go into the swiss alps and get inspirations for my art and compositions. Not having to worry about an income frees my mind, so I can really contribute to the world.”

How to start

Start building your Carpe Diem Pension today. Visit the quick start guide here:

https://docs.carpediempension.com/guide/quick-start

Questions can be asked in the Telegram group (https://t.me/CarpeDiemCDP), in Discord (https://discord.com/invite/carpediem) or by e-mail (info@carpediempension.com).

About Carpe Diem Pension

Carpe Diem Pension is a self-managed pension fund on PulseChain. Users deposit CDP tokens to get and increase a permanent passive pension payout in CDP.