Uber quadruples EPS estimates, but is growth decelerating?

Leading rideshare and delivery platform operator Uber Technologies Inc. (NYSE: UBER) reported a stellar earnings report to round out its first profitable year of operations in 14 years. Uber has achieved its goal of disrupting the transportation sector while fulfilling its path to profitability. While Uber showed GAAP profits in previous quarters in 2023, they were mostly due to the unrealized gains in its equity stake holdings.

These gains had nothing to do with the core business, nor were they cash transactions that contributed to cash flow. However, its Q4 2023 earnings actually derived profits from its core operations. Uber shares rallied over 40% heading into its recent earnings report, with the NYSE: UBER">S&P 500 hitting new highs. This explains the sell-the-news initial reaction to a strong earnings report. Still, investors also ponder if the sequential quarterly drop in Mobility Bookings is an early sign of decelerating growth.

Real GAAP profitability from core operations.

The true historical milestone in Q4 2023 was that Uber genuinely made GAAP profits from its core operations in the quarter. They proudly announced GAAP profitability instead of underscoring its adjusted EBITDA when their investments were in the red. Most of this GAAP profitability, upwards of $1 billion, came from the rise in its ownership equity stakes in various companies.

Uber's ownership positions

As the stock market rises, these unrealized gains may continue to grow. But when the market plateaus or falls, the company may generate negative earnings. It's worth noting that Uber is still underwater in its equity stakes. Many of these positions were taken as a result of asset swaps or straight cash investments.

Its stake in Chinese rideshare operator Didi is down 12%. Its stake in Southeast Asia's leading rideshare operator, Grab Holdings Inc. (NASDAQ: GRAB), is down 14%. Its stake in autonomous driving technology company Aurora Innovation Inc. (NASDAQ: AUR) is down 22%. Its stake in air taxi operator Joby Aviation Inc. (NYSE: JOBY) is down 4%. Uber's stake in e-scooter and e-bike operator Lime is down 29%. The total carrying value of the equity stakes is $6.1 billion, up from $5.1 billion sequentially.

Oligopoly transforming into a Monopoly

Uber has taken such a large lead ahead of its rival Lyft Inc. (NASDAQ: LYFT) that it's not even considered an oligopoly. This is also reflected in its stock prices as Uber shares reach all-time highs in the $70s while LYFT continues to languish in the low teens. Uber's market cap stands at $146 billion versus $5 billion for Lyft. Uber has grown its lead to more than 5X Lyft's in many financial metrics.

Path to profitability achieved.

On Friday, February 7, 2024, Uber released fourth-quarter 2023 GAAP EPS of 66 cents, beating consensus analyst estimates of 16 cents by 50 cents. Revenues surged 15.4% YoY to $9.94 billion, beating analyst expectations of $9.76 billion. Adjusted EPS was $1.3 billion, rising $618 million YoY. Adjusted EPS margin as a percentage of Gross Bookings rose to 3.4%, up from 2.2% in the year-ago quarter. Cash, short-term investments and cash equivalents were $5.4 billion at the end of the quarter.

Growth metrics

Uber deems the combined dollar amount of rides and deliveries before fees and deductions are applied as Gross Bookings. In Q4 2023, Gross bookings grew 21% YOY in constant currency to $37.6 billion. Mobility Gross Bookings rose 28% YoY to $19.3 billion. Delivery Gross Bookings rose 17% YOY to $17 billion.

Delivery grew its market share in ten out of its top ten markets. The grocery delivery business grew to a $7 billion run rate, and advertising is surpassing the $1 billion annual run rate. Monthly active platform customers (MAPCs) rose 15% YOY to 150 million. Total trips grew 24% YOY to 2.6 billion. Monthly trips per MAPC grew 8% to 5.8.

A finicky sell-the-news reaction parallels Google's reaction

Uber shares initially saw profit taking the following morning under concerns of decelerating bookings growth as it sequentially down ticked from 30% in Q3 2023 to 28% in Q4 2023. The same sell-the-new reaction occurred twice in a row with Alphabet Inc. (NASDAQ: GOOGL) when its Cloud revenues growth dropped sequentially from 28% to 22% in Q3 2023 and when Advertising revenues growth dropped sequentially to 11% in Q4 2023.

Outlook for Q1 2024

Uber expected Gross Bookings for Q1 2024 of $37 billion to $38.5 billion, reflecting 20% YOY growth. Adjusted EBITDA is expected to be between $1.26 billion and $1.34 billion.

Uber CEO Dara Khosrowshahi commented, "2023 was an inflection point for Uber, proving that we can continue to generate strong, profitable growth at scale. Our audiences are larger and more engaged than ever, with our platform powering an average of nearly 26 million daily trips last year."

Analyst reactions

Needham reiterated their Buy rating on Uber and raised its price target to $90 from $71. This was driven by its better-than-expected Q4 results and Q1 2024 guidance, pushing up its adjusted EBITDA estimates for 2024 by 4% to $6 billion and 2026 estimates by 2% to $10.4 billion.

Uber Technologies analyst ratings and price targets are at MarketBeat. Uber Technologies peers and competitor stocks can be found with the MarketBeat stock screener.

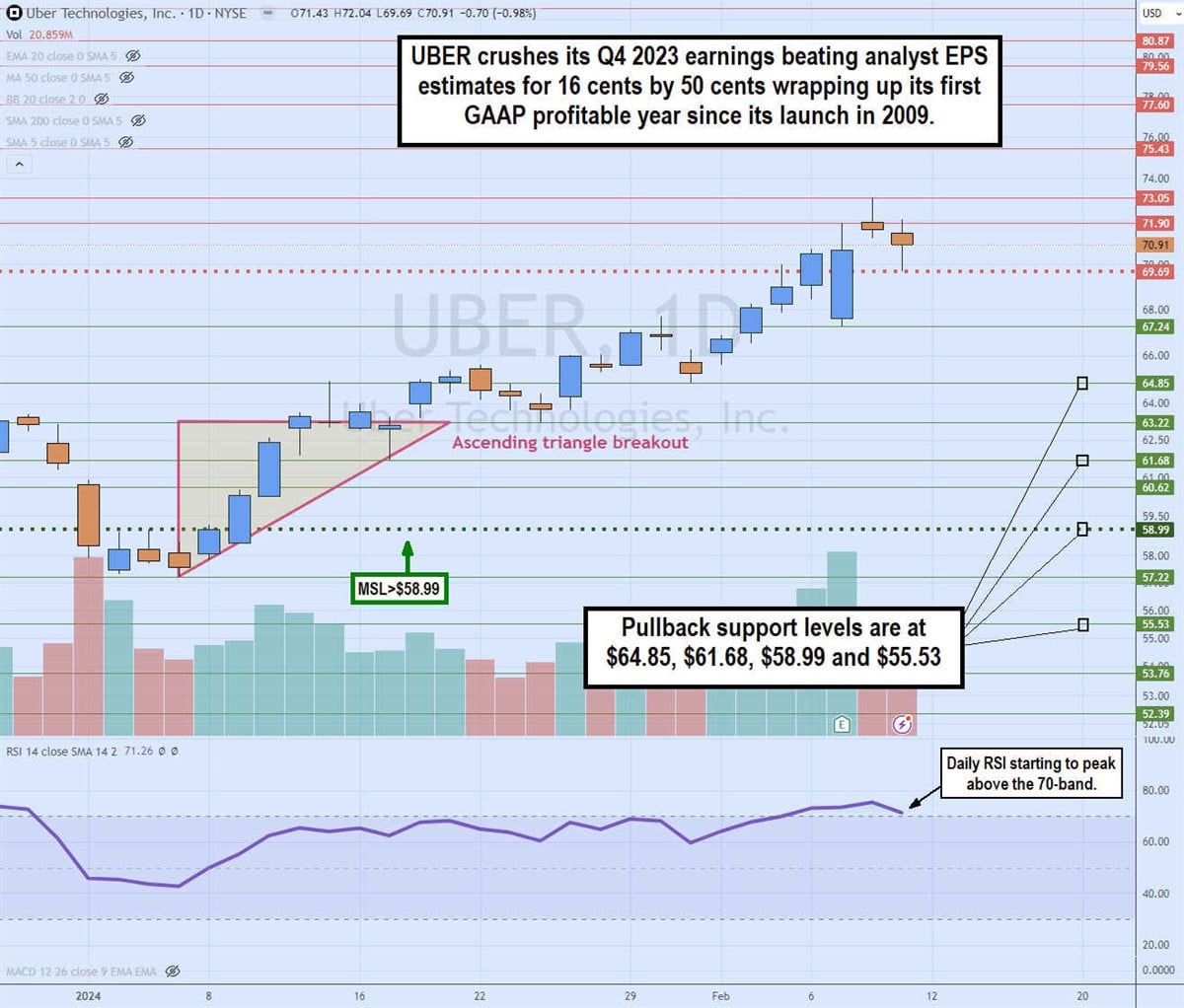

Daily ascending triangle breakout pattern

The daily candlestick chart on UBER illustrates an ascending triangle breakout pattern heading into its Q4 2023 earnings report. Uber shares rallied over 40% since its Q3 2023 earnings report heading into the Q4 release. The ascending trendline formed from the $50.22 low on January 5, 2024. The daily market structure low (MSL) breakout triggered above $58.99. Shares rallied up to the flat-top upper trendline resistance at $63.22. The daily relative strength index (RSI) rallied to the 70-band and stayed just below it as UBER shares floated higher toward the $64.85 level.

UBER launched towards all-time highs on February 1, 2024, as the RSI pierced through the 70-band heading into the earnings release. UBER initially peaked on a sell-the-new reaction following the release as shares fell to $67.24 before bouncing back up towards the $73.05 all-time high the following day. The daily market structure high (MSH) sells trigger formed at $69.69 afterward. Pullback support levels are at $64.85, $61.68, $58.99 and $55.53.

If you believe this article contains misleading, harmful, or spam content, please let us know.

Report this articleMore News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.