Unpacking Q3 Earnings: Montrose (NYSE:MEG) In The Context Of Other Waste Management Stocks

Earnings results often indicate what direction a company will take in the months ahead. With Q3 behind us, let’s have a look at Montrose (NYSE: MEG) and its peers.

Waste management companies can possess licenses permitting them to handle hazardous materials. Furthermore, many services are performed through contracts and statutorily mandated, non-discretionary, or recurring, leading to more predictable revenue streams. However, regulation can be a headwind, rendering existing services obsolete or forcing companies to invest precious capital to comply with new, more environmentally-friendly rules. Lastly, waste management companies are at the whim of economic cycles. Interest rates, for example, can greatly impact industrial production or commercial projects that create waste and byproducts.

The 8 waste management stocks we track reported a softer Q3. As a group, revenues missed analysts’ consensus estimates by 2.1%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 8.9% since the latest earnings results.

Montrose (NYSE: MEG)

Founded to protect a tree-lined two-lane road, Montrose (NYSE: MEG) provides air quality monitoring, environmental laboratory testing, compliance, and environmental consulting services.

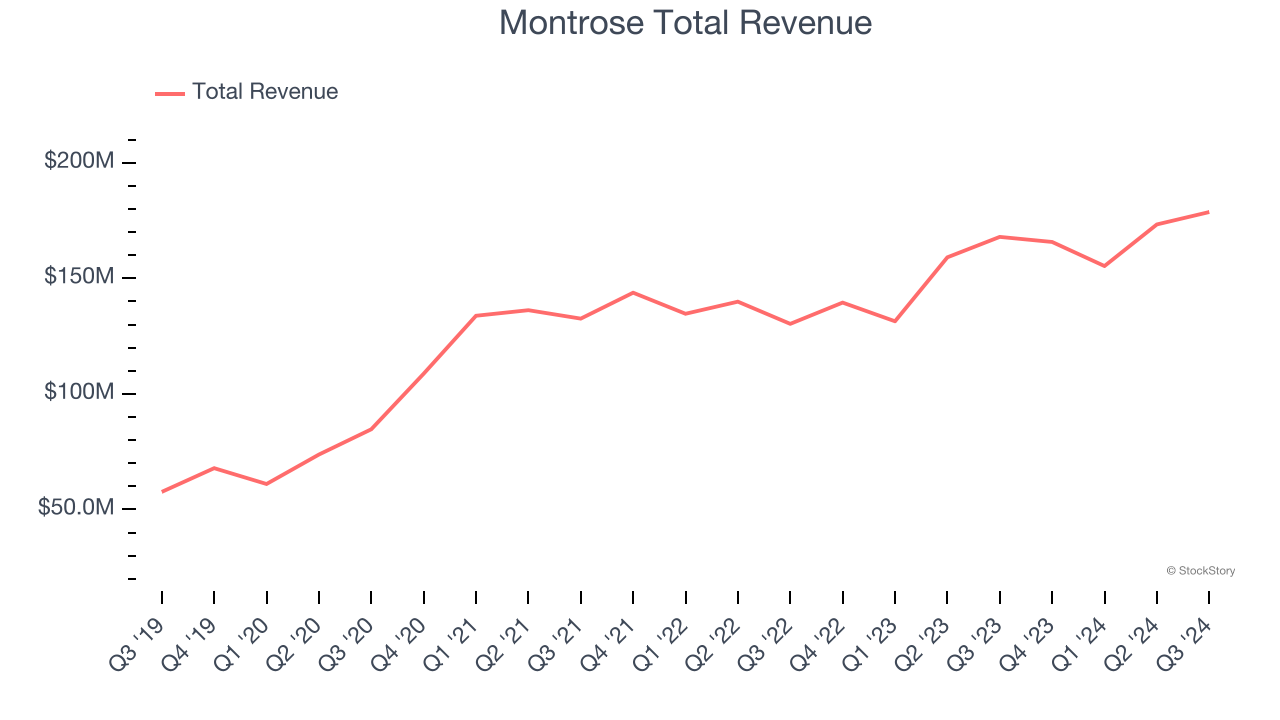

Montrose reported revenues of $178.7 million, up 6.4% year on year. This print fell short of analysts’ expectations by 3.7%. Overall, it was a mixed quarter for the company with an impressive beat of analysts’ adjusted operating income estimates but a significant miss of analysts’ organic revenue estimates.

Montrose Chief Executive Officer and Director, Vijay Manthripragada, commented, "We are pleased to report another quarter of strong performance with record results driven by continued demand for our comprehensive suite of integrated solutions. Record quarterly revenues and Consolidated Adjusted EBITDA1, as well as the 190 basis points of margin improvement, evidence the alignment of our in-demand, higher-margin offerings with our strategic and financial goals. Our strong track record of organic growth, including ongoing cross-selling success, alongside the successful integration of recent acquisitions, continue to demonstrate the strategic advantages provided by our business model. "

Montrose pulled off the highest full-year guidance raise of the whole group. Still, the market seems discontent with the results. The stock is down 8.2% since reporting and currently trades at $20.79.

Is now the time to buy Montrose? Access our full analysis of the earnings results here, it’s free.

Best Q3: Republic Services (NYSE: RSG)

Processing several million tons of recyclables annually, Republic (NYSE: RSG) provides waste management services for residences, companies, and municipalities.

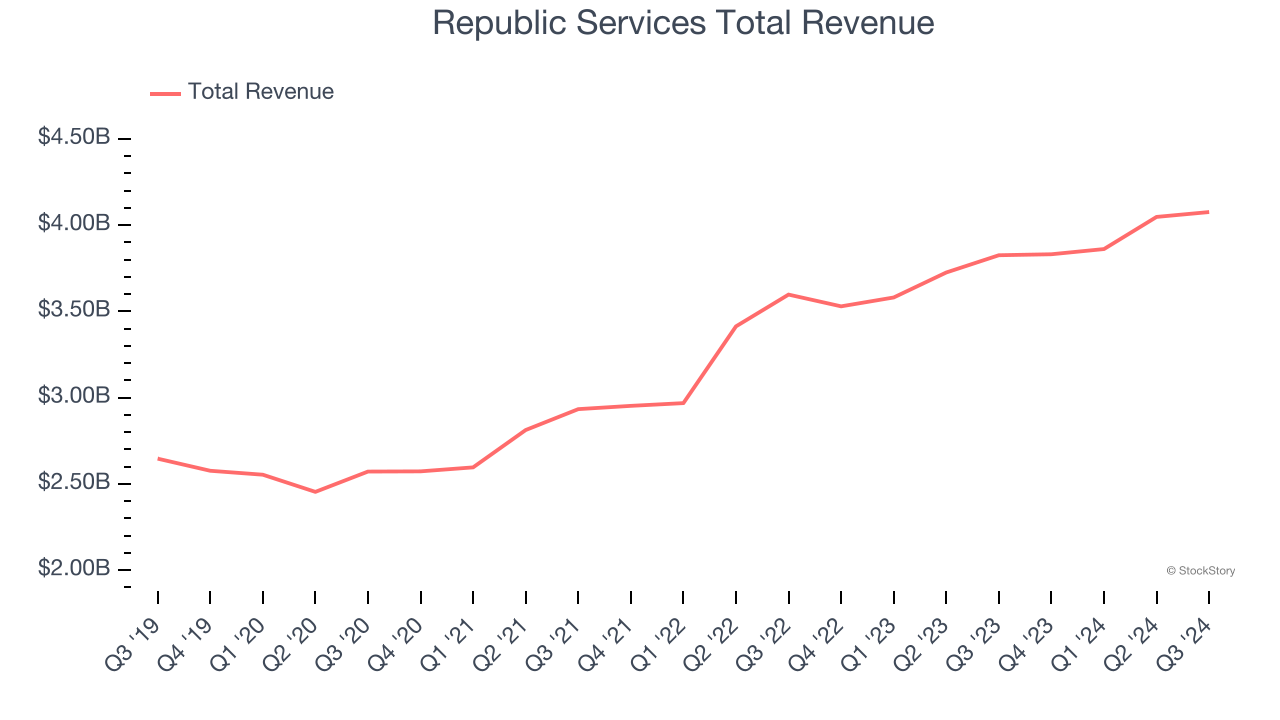

Republic Services reported revenues of $4.08 billion, up 6.5% year on year, falling short of analysts’ expectations by 1.1%. The business performed better than its peers, but it was unfortunately a mixed quarter with a solid beat of analysts’ adjusted operating income estimates but a slight miss of analysts’ sales volume estimates.

The market seems happy with the results as the stock is up 8.2% since reporting. It currently trades at $221.

Is now the time to buy Republic Services? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Quest Resource (NASDAQ: QRHC)

Recycling corporate waste to help companies be more sustainable, Quest Resource (NASDAQ: QRHC) is a provider of waste and recycling services.

Quest Resource reported revenues of $72.77 million, up 3.3% year on year, falling short of analysts’ expectations by 5.6%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

As expected, the stock is down 31% since the results and currently trades at $5.68.

Read our full analysis of Quest Resource’s results here.

Waste Management (NYSE: WM)

Headquartered in Houston, Waste Management (NYSE: WM) is a provider of comprehensive waste management services in North America.

Waste Management reported revenues of $5.89 billion, up 13% year on year. This print beat analysts’ expectations by 0.9%. More broadly, it was a slower quarter as it recorded a significant miss of analysts’ adjusted operating income and EPS estimates.

The stock is up 6.8% since reporting and currently trades at $223.92.

Read our full, actionable report on Waste Management here, it’s free.

Clean Harbors (NYSE: CLH)

Established in 1980, Clean Harbors (NYSE: CLH) provides environmental and industrial services like hazardous and non-hazardous waste disposal and emergency spill cleanups.

Clean Harbors reported revenues of $1.53 billion, up 12% year on year. This result topped analysts’ expectations by 1.6%. Aside from that, it was a slower quarter as it produced full-year EBITDA guidance missing analysts’ expectations.

Clean Harbors pulled off the biggest analyst estimates beat among its peers. The stock is down 10.4% since reporting and currently trades at $236.24.

Read our full, actionable report on Clean Harbors here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.