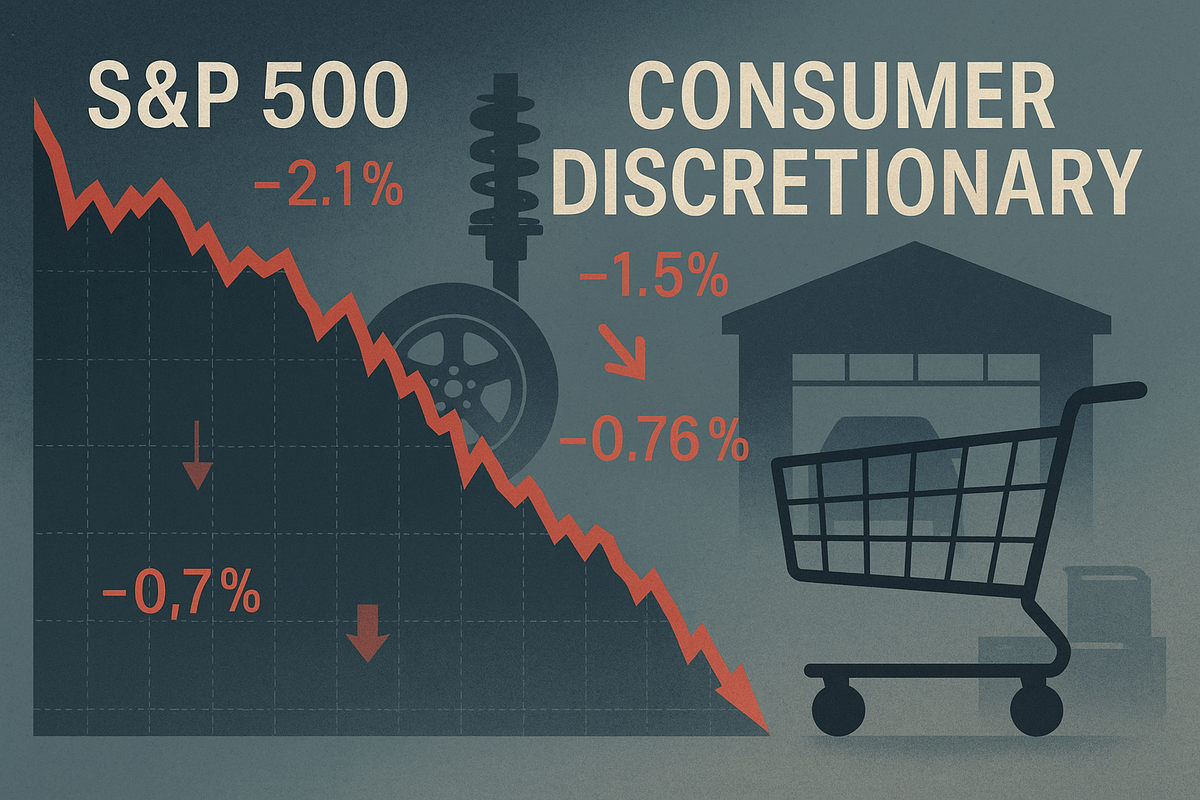

The S&P 500 Consumer Discretionary sector experienced a significant downturn today, September 23, 2025, registering a notable decline of -1.49%. This pronounced weakness was largely driven by a disappointing profit miss from automotive parts giant AutoZone (NYSE: AZO), whose fiscal fourth-quarter results sent ripples of concern through the market. The sector's performance highlights growing pressures on consumer spending and corporate profitability, signaling a potentially challenging environment for discretionary businesses moving forward.

This immediate market reaction underscores investor sensitivity to earnings performance, particularly in a sector highly susceptible to economic fluctuations. While AutoZone's sales remained robust, its inability to translate top-line growth into expected profits has raised questions about margin sustainability across the retail landscape, prompting a re-evaluation of investment strategies in the current economic climate.

What Happened and Why It Matters: AutoZone's Earnings and Sector Weakness

AutoZone (NYSE: AZO), a cornerstone of the automotive aftermarket retail industry, announced its fiscal fourth-quarter 2025 results today, which fell short of analyst expectations. The company reported diluted earnings per share (EPS) of $48.71, missing consensus estimates that ranged from $50.52 to $50.93. This marks the fifth consecutive quarter that AutoZone has failed to meet its earnings targets, a trend that is increasingly difficult for investors to overlook.

Despite the profit miss, AutoZone's revenue largely met expectations, posting $6.24 billion in sales, a 0.6% increase from the prior year (or a more robust 6.9% when adjusted for an extra week in the previous quarter). The company also demonstrated strong underlying sales momentum, with total company same-store sales increasing by 5.1%, and domestic same-store sales up 4.8%. Its domestic commercial (DIFM) segment saw an acceleration to 12.5% growth, and even domestic retail (DIY) comparable sales grew 2.2%, with discretionary categories within DIY posting their strongest gain since fiscal year 2023.

The primary culprits behind the profit shortfall were several significant cost pressures. A substantial $80 million non-cash Last-In, First-Out (LIFO) charge heavily impacted the gross profit margin, leading to a decline of 98 to 128 basis points to 51.5%. Additionally, operating, selling, general, and administrative (SG&A) expenses rose 3.0% to $2.02 billion, increasing to 32.4% of sales from 31.6% a year ago. These elevated expenses were largely attributed to strategic investments in growth initiatives, including the opening of 141 new stores and a 14.1% expansion of inventory. Unfavorable foreign exchange rates also chipped away at profitability, reducing net sales by $36 million and EBIT by $14 million, impacting EPS by $0.57.

Investor reaction to AutoZone's announcement was swift and negative, with the stock price declining by over 4% initially, settling down by 2-3.2% in regular trading. AutoZone was singled out as the "biggest laggard" in the Consumer Discretionary sector today, significantly contributing to its overall -1.49% decline. This reaction highlights a broader market concern: even strong top-line sales growth is not enough if profitability is eroding due to rising costs and strategic investments that take time to yield returns. The situation is further compounded by news from competitor Advance Auto Parts (NYSE: AAP), which announced over 500 store closures and restructuring plans today, leading to its stock being down 6.2%. This reinforces negative sentiment across the automotive retail segment and broader consumer discretionary landscape.

Economic Headwinds and Market Implications

The underperformance of the Consumer Discretionary sector, anchored by AutoZone's miss, is not an isolated event but rather a symptom of broader economic headwinds that could reshape market dynamics. The U.S. economy is at a critical juncture, with consumer spending projected to decelerate through the remainder of 2025 and into 2026. Factors such as persistent inflation, rising borrowing costs, a cooling labor market, and ongoing economic uncertainty are collectively eroding consumer confidence and purchasing power. Recent data indicating a slip in consumer sentiment for September serves as an ominous sign for an economy heavily reliant on personal consumption.

This environment suggests a challenging period for companies whose revenues depend on non-essential purchases. Investors are likely to become more discerning, favoring businesses with resilient demand, strong cost controls, and clear value propositions. While the Federal Reserve has resumed cutting rates, the lingering uncertainty surrounding monetary policy and inflation concerns continues to create market volatility, making it difficult for investors to predict future consumer behavior accurately. The impact of tariffs also remains a significant concern, increasing costs for retailers and influencing consumer spending decisions, as exemplified by AutoZone's higher prices due to tariffs.

In this evolving landscape, a clear divide may emerge between potential winners and losers. Value-oriented retailers, such as discount chains like Five Below (NASDAQ: FIVE), Dollar Tree (NASDAQ: DLTR), and Dollar General (NYSE: DG), alongside large grocers like Walmart (NYSE: WMT) and Kroger (NYSE: KR), are well-positioned. As consumers become more cost-conscious, these companies offering essential goods and competitive pricing are likely to capture a larger share of shrinking budgets. Similarly, businesses focused on experiences—such as travel, entertainment, and service-oriented sectors—may continue to see demand as consumers prioritize unique moments over material possessions. Pro-focused retailers like Home Depot (NYSE: HD), which are strategically catering to professional contractors and builders, could also thrive due to more predictable and higher-margin revenue streams.

Conversely, retailers heavily reliant on big-ticket, non-essential items or those with significant exposure to international supply chains face considerable risks. Companies selling luxury goods (outside of potentially resilient European markets), non-essential clothing, or those in the dining-out sector could see further cutbacks in consumer spending. Businesses unable to adapt to the new value-conscious consumer, or those struggling with cost management and tariff impacts (like Lululemon (NASDAQ: LULU), which has reportedly seen its stock "demolished" by tariff impacts and shrinking margins), are likely to face significant challenges. The automotive aftermarket, while generally considered recession-resistant due to essential vehicle maintenance, will still require companies like O'Reilly Automotive (NASDAQ: ORLY) to manage costs effectively to avoid similar profitability issues seen with AutoZone.

Broader Implications and Industry Reset

The recent performance of the Consumer Discretionary sector, particularly the challenges faced by AutoZone and Advance Auto Parts, underscores a broader industry reset influenced by shifting consumer behaviors and persistent economic pressures. This isn't just about one company's earnings; it's a signal for the wider retail industry. The underlying demand for vehicle maintenance and repair remains robust, driven by the increasing cost of new cars pushing consumers to extend the life of their existing vehicles. However, even in this resilient segment, profitability is under pressure due to rising operating costs, inventory management complexities like LIFO charges, and aggressive expansion strategies.

The implications for broader consumer spending trends are significant. Analysts anticipate a cooling of nominal spending growth through the end of 2025 and into 2026. Consumers are becoming more cautious and pragmatic, meticulously adjusting their budgets and prioritizing essentials and value over purely discretionary purchases. This "spending reset" reflects a shift towards long-term value and experiences, particularly among lower and middle-income demographics who are most sensitive to inflationary pressures and rising costs. While retail sales in September showed some resilience, especially in online and general merchandise categories, the overall sentiment points towards a more restrained holiday season in 2025, with projections indicating a 5% decline in consumer spending from 2024—the first notable drop since 2020. Consumers are planning to cut back on dining out, clothing, and big-ticket items.

This environment necessitates a strategic pivot for retailers across the board. Companies must focus on affordability, transparency, and delivering clear long-term value to win over increasingly discerning consumers. Those with inefficient supply chains or heavy reliance on international sourcing will need to re-evaluate their strategies to mitigate the impact of tariffs and foreign exchange volatility. The challenges faced by AutoZone, particularly its aggressive store expansion and inventory growth, highlight the delicate balance between growth initiatives and maintaining profitability in a high-cost environment. The industry will likely see further consolidation, restructuring, and a greater emphasis on operational efficiency and cost control.

Regulatory and policy implications also loom large, particularly regarding tariffs. The continuation or expansion of tariff policies will directly impact import costs, which retailers may or may not be able to pass on to consumers without affecting demand. Companies with strong domestic supply chains or those that can effectively absorb or mitigate these costs will gain a competitive advantage. Historically, periods of economic uncertainty and squeezed consumer budgets have led to a flight to value and essential goods, a pattern that appears to be re-emerging in the current market.

What to Pay Attention to Next

Looking ahead, investors and consumers alike should closely monitor several key indicators and trends. In the short term, the earnings reports of other automotive aftermarket retailers, such as O'Reilly Automotive (NASDAQ: ORLY), will be crucial. Their performance will provide further insights into whether AutoZone's challenges are company-specific or indicative of broader industry headwinds, particularly concerning margin pressures and cost management. Any updates on Advance Auto Parts' (NYSE: AAP) restructuring plans will also be important for assessing the overall health and future direction of the sector.

Beyond the automotive segment, attention should turn to broader consumer spending data, including monthly retail sales figures and consumer sentiment surveys. These will offer real-time insights into the strength of the consumer and their willingness to engage in discretionary purchases. Any significant shifts in inflation rates or the Federal Reserve's monetary policy, especially regarding future rate cuts, will also have a profound impact on borrowing costs and, consequently, consumer purchasing power.

In the long term, retailers will need to demonstrate strategic agility. Companies that can effectively pivot towards value offerings, enhance their e-commerce capabilities, and optimize their supply chains to mitigate tariff impacts and improve cost efficiency will be best positioned for success. The holiday shopping season in late 2025 will serve as a critical test for many discretionary retailers, revealing the true extent of the "spending reset" and consumer prioritization. Businesses that can innovate in customer engagement and offer compelling value propositions, whether through product bundling, loyalty programs, or unique experiences, will likely emerge stronger from this challenging period.

Conclusion

Today's performance of the S&P 500 Consumer Discretionary sector, marked by a significant decline and AutoZone's (NYSE: AZO) profit miss, serves as a potent reminder of the complex forces currently shaping financial markets. While AutoZone demonstrated robust sales growth, its inability to meet profit expectations due to substantial LIFO charges, increased operating expenses, and unfavorable foreign exchange rates highlights the critical importance of margin management in an inflationary and cost-pressured environment. This event is not merely an isolated corporate disappointment but a bellwether for the broader retail industry, signaling a period of heightened scrutiny on profitability and operational efficiency.

Moving forward, the market will likely continue to differentiate between companies that can effectively navigate a landscape characterized by cautious consumers, persistent tariffs, and evolving economic policies. The "spending reset" is encouraging consumers to prioritize value, essentials, and experiences, creating both challenges and opportunities for businesses. Investors should closely watch for signs of adaptability among retailers, particularly their ability to control costs, optimize supply chains, and resonate with a more discerning customer base.

The coming months will be crucial for assessing the resilience of the Consumer Discretionary sector. Companies that demonstrate robust financial health, strategic foresight, and an unwavering focus on delivering value will be best positioned to thrive amidst these headwinds. Conversely, those unable to adapt to these shifting dynamics may face continued struggles. This period demands vigilance and strategic planning from both companies and investors as the retail industry recalibrates for a new economic reality.

This content is intended for informational purposes only and is not financial advice