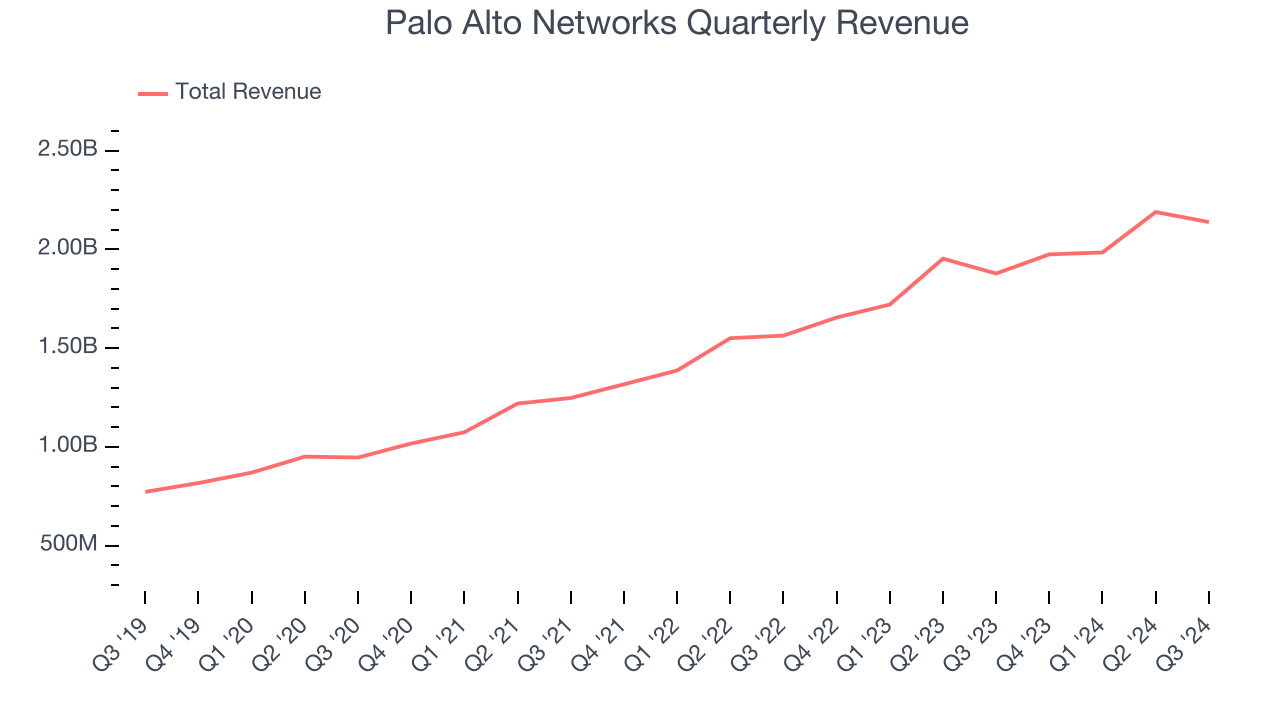

Cybersecurity provider Palo Alto Networks (NASDAQ: PANW) beat Wall Street’s revenue expectations in Q3 CY2024, with sales up 13.9% year on year to $2.14 billion. The company expects next quarter’s revenue to be around $2.24 billion, close to analysts’ estimates. Its non-GAAP profit of $1.56 per share was 5.8% above analysts’ consensus estimates.

Is now the time to buy Palo Alto Networks? Find out by accessing our full research report, it’s free.

Palo Alto Networks (PANW) Q3 CY2024 Highlights:

- Revenue: $2.14 billion vs analyst estimates of $2.12 billion (13.9% year-on-year growth, 0.8% beat)

- Adjusted EPS: $1.56 vs analyst estimates of $1.48 (5.8% beat)

- The company slightly lifted its revenue guidance for the full year to $9.15 billion at the midpoint from $9.13 billion (slight beat)

- Management raised its full-year Adjusted EPS guidance to $6.32 at the midpoint, a 1.3% increase (slight beat)

- Operating Margin: 13.4%, up from 11.5% in the same quarter last year

- Market Capitalization: $127 billion

"Our Q1 results reinforced our conviction in our differentiated platformization strategy," said Nikesh Arora, chairman and CEO of Palo Alto Networks.

Company Overview

Founded in 2005 by cybersecurity engineer Nir Zuk, Palo Alto Networks (NASDAQ: PANW) makes hardware and software cybersecurity products that protect companies from cyberattacks, breaches, and malware threats.

Network Security

Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks. The migration of businesses to the cloud and employees working remotely in insecure environments is increasing demand modern cloud-based network security software, which offers better performance at lower cost than maintaining the traditional on-premise solutions, such as expensive specialized firewall hardware.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Luckily, Palo Alto Networks’s sales grew at a decent 22.1% compounded annual growth rate over the last three years. Its growth was slightly above the average software company and shows its offerings resonate with customers.

This quarter, Palo Alto Networks reported year-on-year revenue growth of 13.9%, and its $2.14 billion of revenue exceeded Wall Street’s estimates by 0.8%. Company management is currently guiding for a 13.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 14% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and implies the market is baking in success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s expensive for Palo Alto Networks to acquire new customers as its CAC payback period checked in at 65.8 months this quarter. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from Palo Alto Networks’s Q3 Results

It seemed like a pretty solid quarter, with revenue beating slightly and full year guidance for revenue and EPS both lifted a bit. Both guidance metrics also came in a bit above expectations. It wasn't enough for the market though, and this is not the first example of a software company this quarter that showed similar results followed by a move down in the stock. Shares traded down 4.5% to $374.97 immediately following the results.

Is Palo Alto Networks an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.