Even though Frost Bank (currently trading at $122 per share) has gained 10.3% over the last six months, it has lagged the S&P 500’s 29.3% return during that period. This might have investors contemplating their next move.

Is CFR a buy right now? Or is its underperformance reflective of its business quality?

Why Does CFR Stock Spark Debate?

Tracing its roots back to 1868 when it was founded during Texas's post-Civil War reconstruction era, Cullen/Frost Bankers (NYSE: CFR) operates Frost Bank, a Texas-based financial institution providing commercial and consumer banking, wealth management, and insurance services.

Two Things to Like:

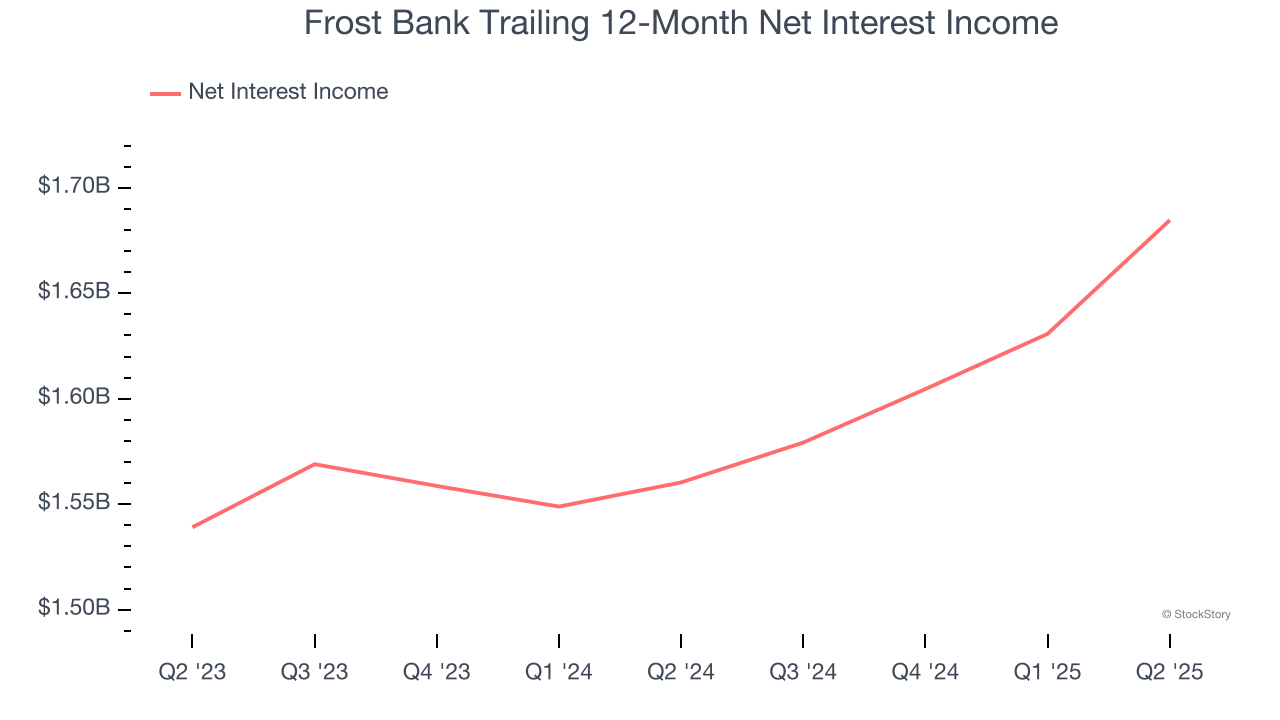

1. Net Interest Income Skyrockets, Fueling Growth Opportunities

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Frost Bank’s net interest income has grown at a 12.1% annualized rate over the last five years, better than the broader banking industry and faster than its total revenue.

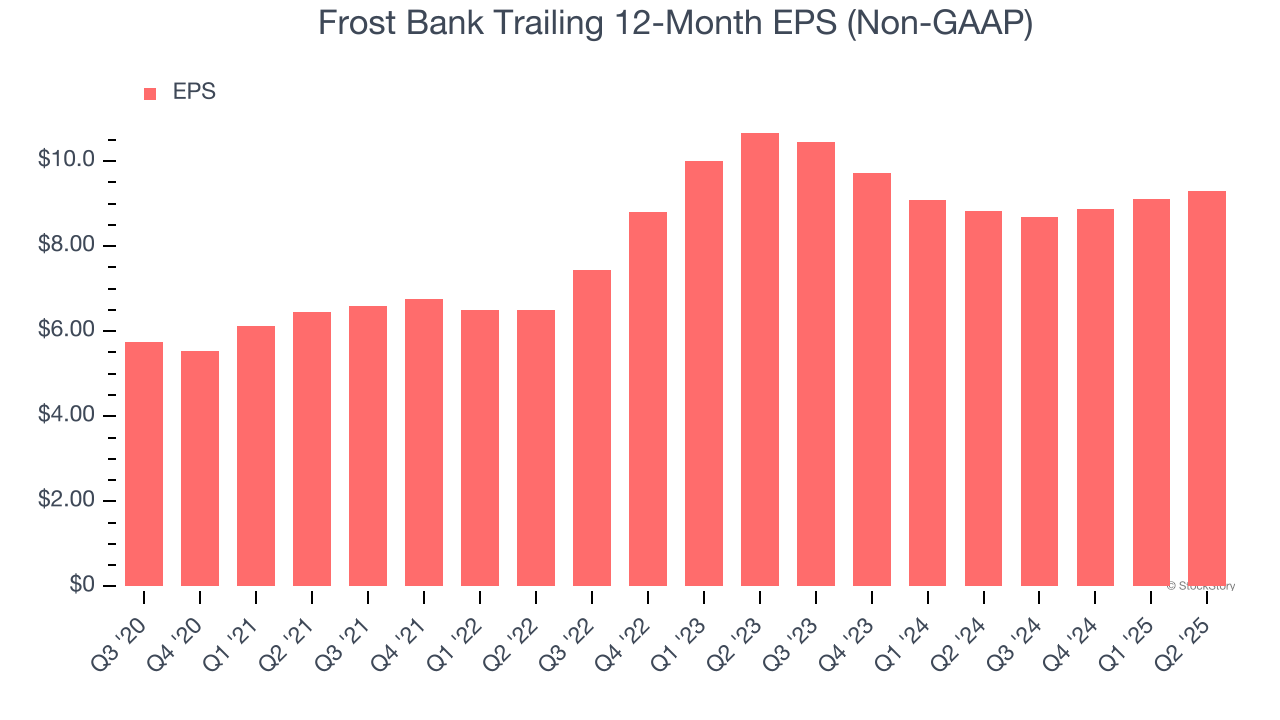

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Frost Bank’s EPS grew at an astounding 10.6% compounded annual growth rate over the last five years, higher than its 7.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

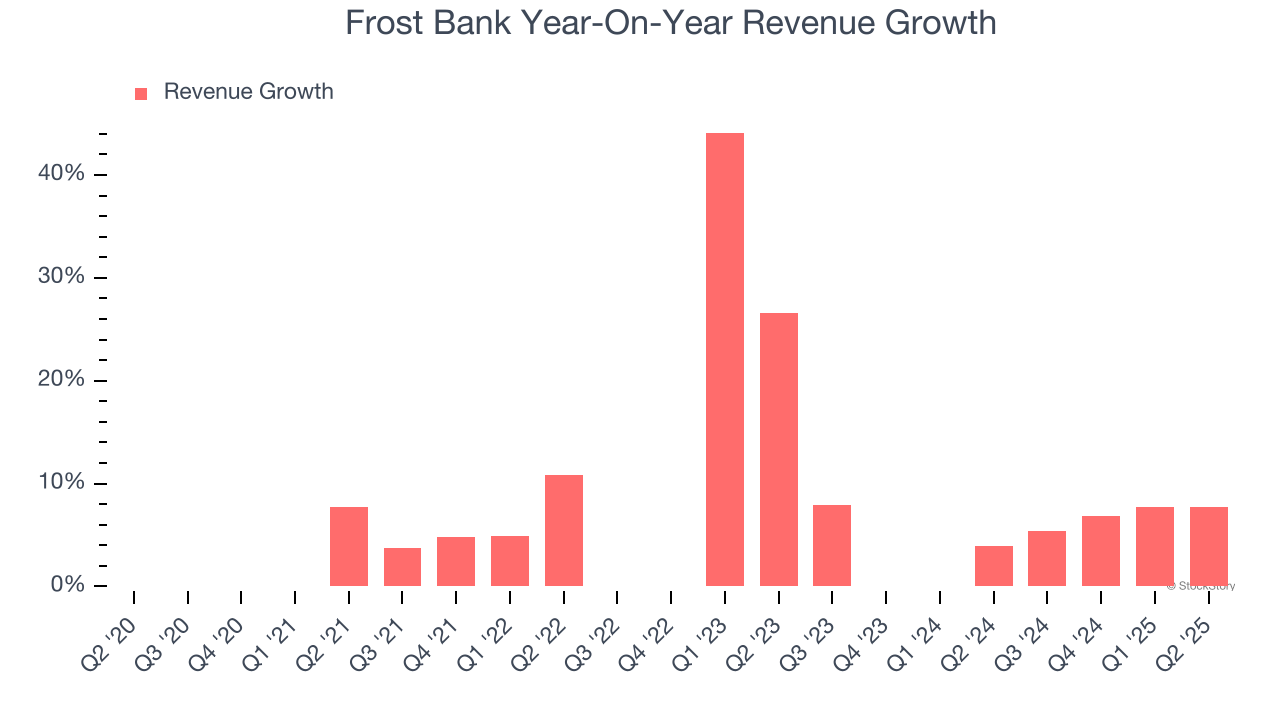

Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Frost Bank’s recent performance shows its demand has slowed as its annualized revenue growth of 4.7% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Final Judgment

Frost Bank’s positive characteristics outweigh the negatives. With its shares underperforming the market lately, the stock trades at 1.8× forward P/B (or $122 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

Stocks We Like Even More Than Frost Bank

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.