Independent Bank (INDB) Reports Earnings Tomorrow: What To Expect

By:

StockStory

October 14, 2025 at 23:03 PM EDT

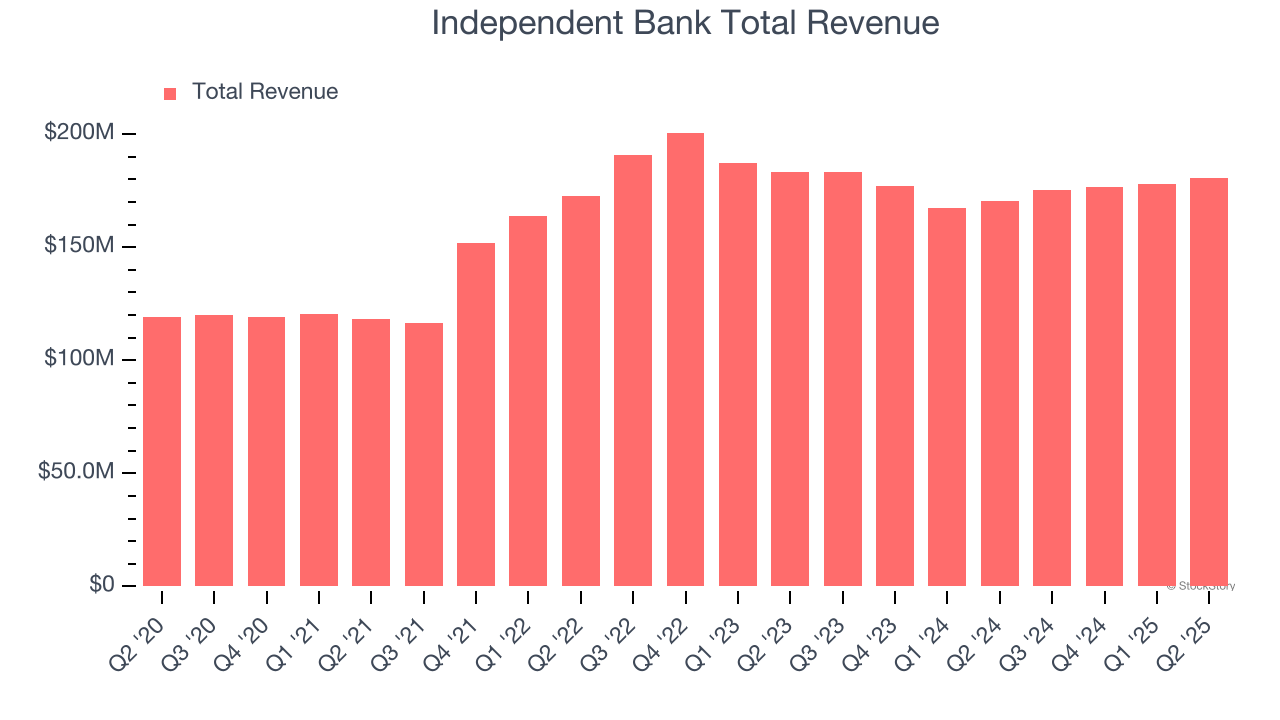

Regional banking company Independent Bank (NASDAQ: INDB) will be announcing earnings results this Thursday after the bell. Here’s what to expect. Independent Bank beat analysts’ revenue expectations by 1.7% last quarter, reporting revenues of $180.6 million, up 6.1% year on year. It was a satisfactory quarter for the company, with an impressive beat of analysts’ net interest income estimates but a narrow beat of analysts’ EPS estimates. Is Independent Bank a buy or sell going into earnings? Read our full analysis here, it’s free for active Edge members. This quarter, analysts are expecting Independent Bank’s revenue to grow 39% year on year to $243.6 million, a reversal from the 4.5% decrease it recorded in the same quarter last year. Adjusted earnings are expected to come in at $1.54 per share.  Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. Independent Bank has only missed Wall Street’s revenue estimates once over the last two years, exceeding top-line expectations by 0.8% on average. Looking at Independent Bank’s peers in the banks segment, some have already reported their Q3 results, giving us a hint as to what we can expect. FB Financial delivered year-on-year revenue growth of 94.2%, beating analysts’ expectations by 4.2%, and Citigroup reported revenues up 9.3%, topping estimates by 4.6%. Read our full analysis of FB Financial’s results here and Citigroup’s results here. Investors in the banks segment have had fairly steady hands going into earnings, with share prices down 1.5% on average over the last month. Independent Bank is down 1.5% during the same time and is heading into earnings with an average analyst price target of $80.75 (compared to the current share price of $69.84). P.S. While everyone's chasing Nvidia, we found a hidden AI semiconductor winner trading at a fraction of the price. See our #1 pick before Wall Street catches on. StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here. More NewsView More

Five Below and Dollar Tree Earnings Signal a Shopper Shift ↗

Today 7:15 EST

Via MarketBeat

Ulta’s Stock May Be Set for a Glow-Up—20% Upside Ahead? ↗

December 06, 2025

Via MarketBeat

Tickers

ULTA

Gates Foundation Sells MSFT Stock—Should Investors Be Worried? ↗

December 06, 2025

Via MarketBeat

Tickers

MSFT

MarketBeat Week in Review – 12/1 - 12/5 ↗

December 06, 2025

Rocket Lab’s Big Rebound? Analysts Suggest the Dip's a Gift ↗

December 05, 2025

Via MarketBeat

Tickers

RKLB

Recent QuotesView More

Stock Quote API & Stock News API supplied by www.cloudquote.io

Quotes delayed at least 20 minutes. By accessing this page, you agree to the Privacy Policy and Terms Of Service.

© 2025 FinancialContent. All rights reserved.

|