3 Reasons to Avoid FLEX and 1 Stock to Buy Instead

By:

StockStory

October 20, 2025 at 00:02 AM EDT

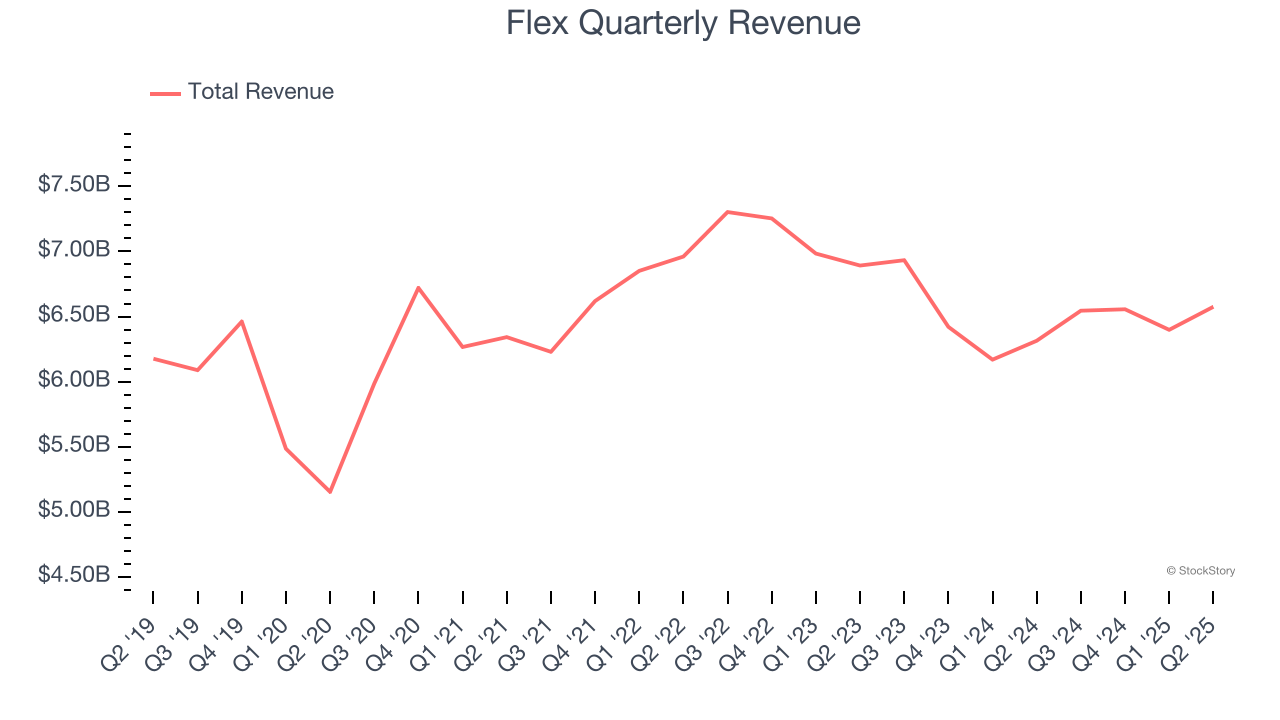

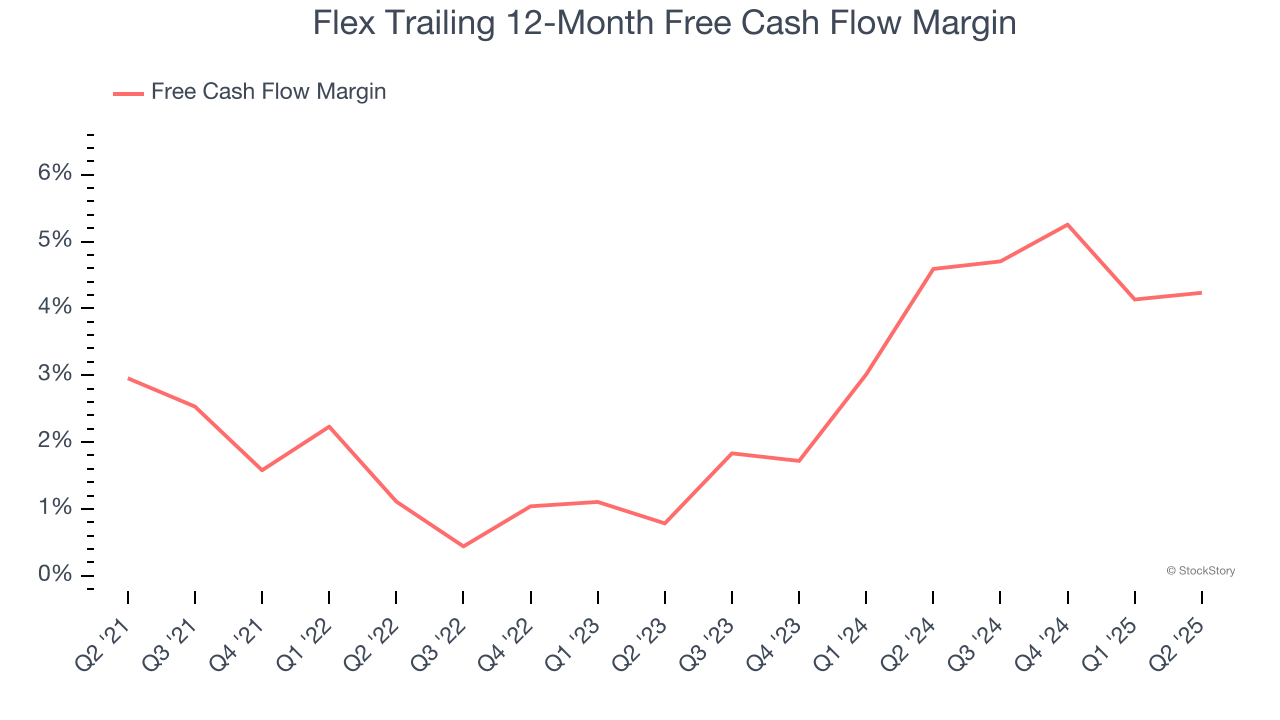

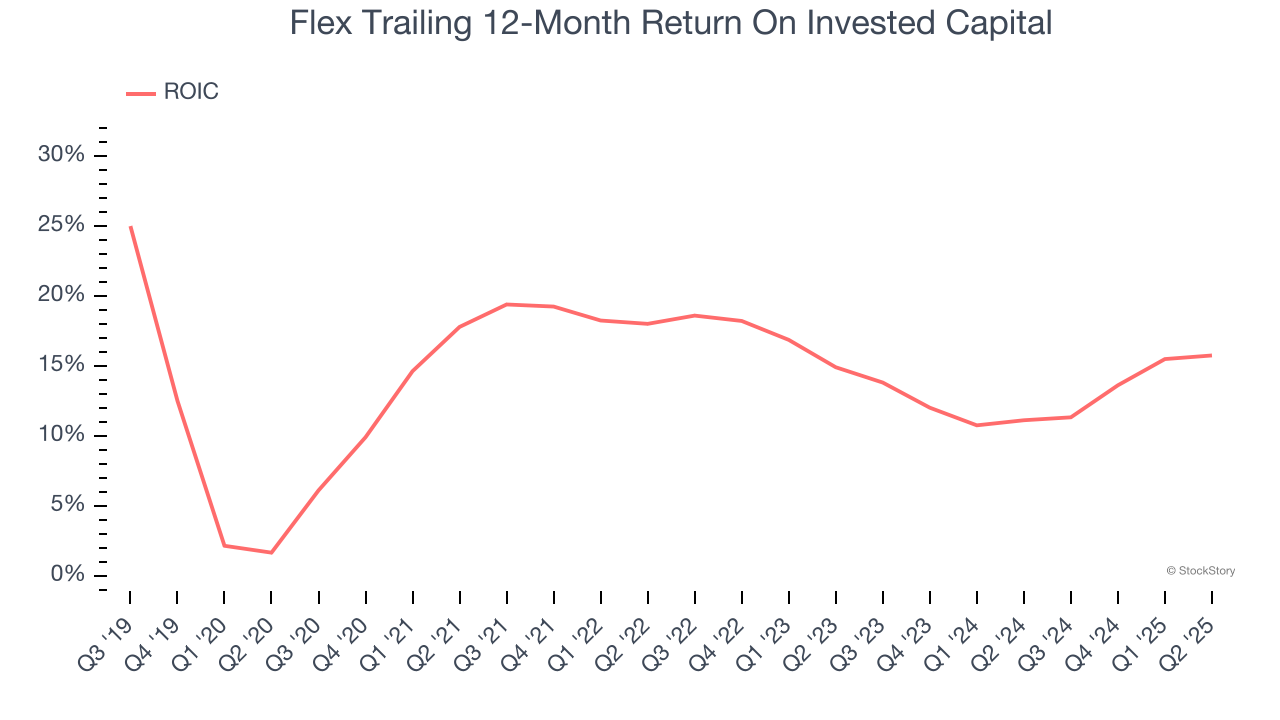

Flex has been on fire lately. In the past six months alone, the company’s stock price has rocketed 106%, reaching $63 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation. Is there a buying opportunity in Flex, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members. Why Is Flex Not Exciting?Despite the momentum, we're cautious about Flex. Here are three reasons why FLEX doesn't excite us and a stock we'd rather own. 1. Long-Term Revenue Growth DisappointsA company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Flex’s sales grew at a sluggish 2.4% compounded annual growth rate over the last five years. This fell short of our benchmarks.  2. Mediocre Free Cash Flow Margin Limits Reinvestment PotentialIf you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills. Flex has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.7%, subpar for a business services business.  3. New Investments Fail to Bear Fruit as ROIC DeclinesROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity). We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Flex’s ROIC decreased by 4.5 percentage points annually over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.  Final JudgmentFlex’s business quality ultimately falls short of our standards. After the recent rally, the stock trades at 20.3× forward P/E (or $63 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better investments elsewhere. Let us point you toward the most dominant software business in the world. Stocks We Would Buy Instead of FlexTrump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines. Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025). Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today. StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here. More NewsView More

Rocket Lab’s Big Rebound? Analysts Suggest the Dip's a Gift ↗

Today 17:19 EST

Via MarketBeat

Tickers

RKLB

Via MarketBeat

Via MarketBeat

Tickers

KRKNF

Via MarketBeat

Recent QuotesView More

Stock Quote API & Stock News API supplied by www.cloudquote.io

Quotes delayed at least 20 minutes. By accessing this page, you agree to the Privacy Policy and Terms Of Service.

© 2025 FinancialContent. All rights reserved.

|