3 Reasons PLXS is Risky and 1 Stock to Buy Instead

By:

StockStory

October 30, 2025 at 00:00 AM EDT

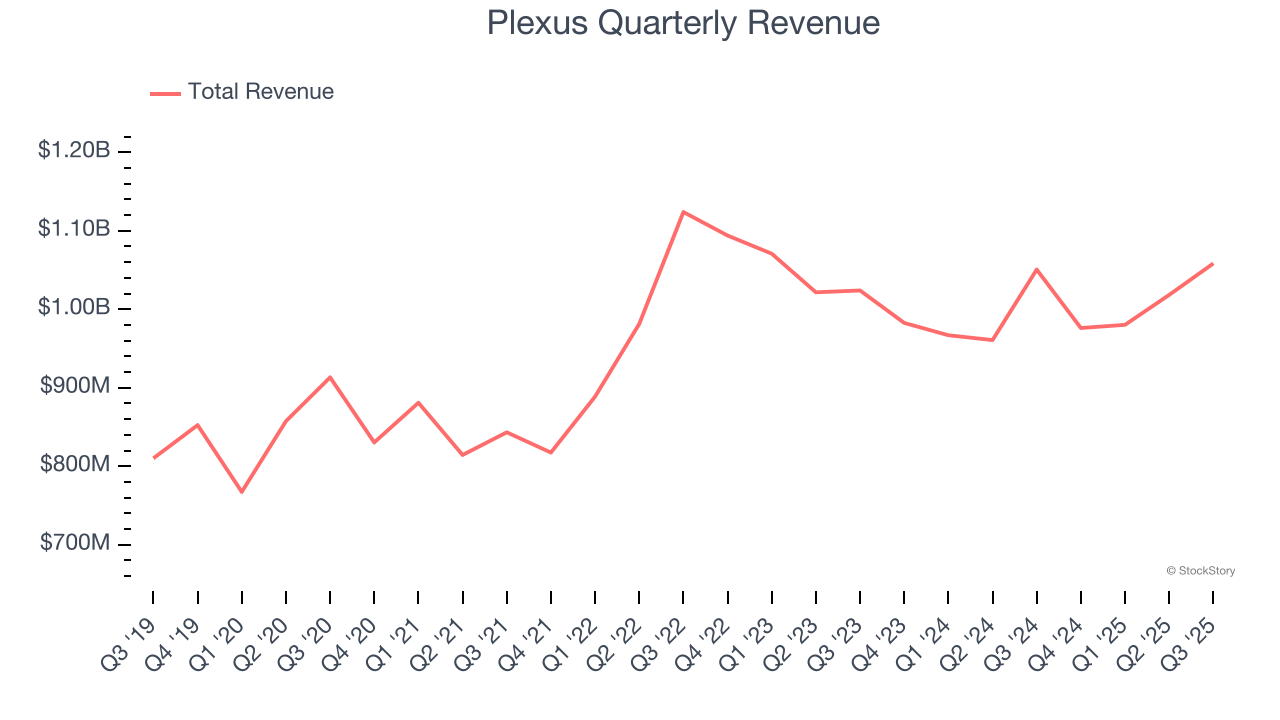

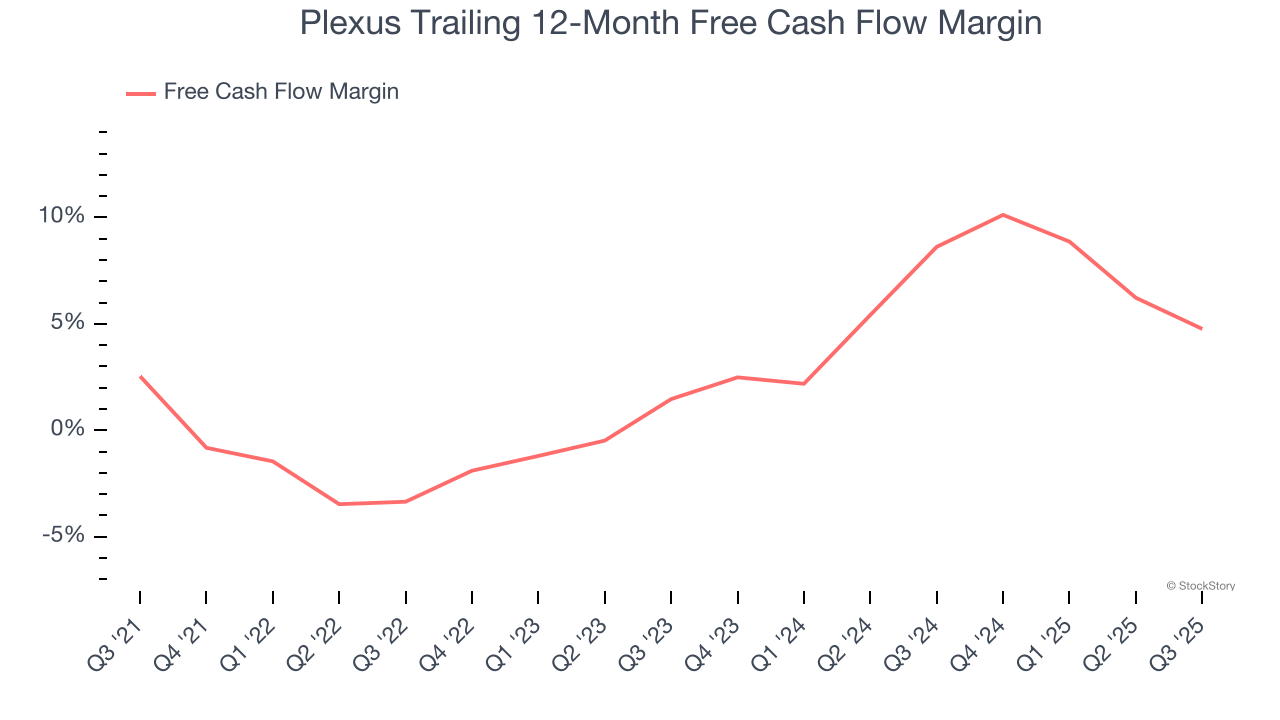

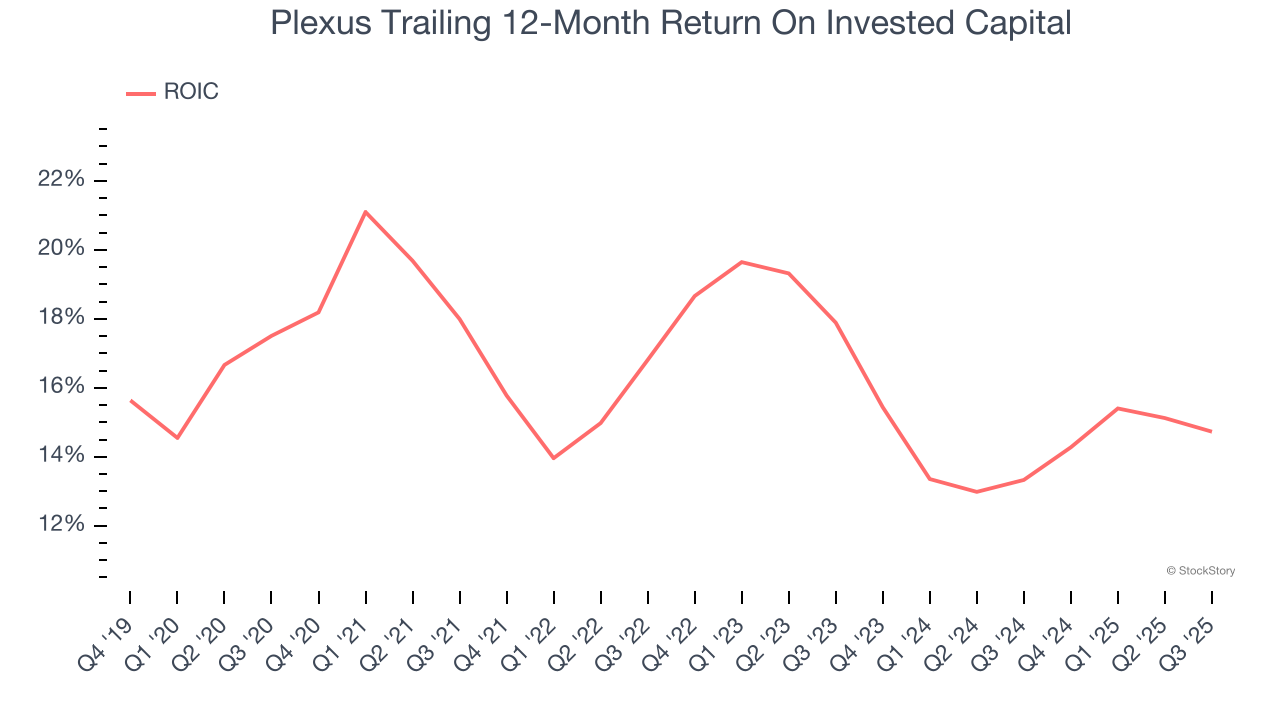

Even though Plexus (currently trading at $139.47 per share) has gained 13.9% over the last six months, it has lagged the S&P 500’s 23.8% return during that period. This may have investors wondering how to approach the situation. Is there a buying opportunity in Plexus, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members. Why Do We Think Plexus Will Underperform?We're sitting this one out for now. Here are three reasons why PLXS doesn't excite us and a stock we'd rather own. 1. Long-Term Revenue Growth DisappointsA company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Plexus’s 3.5% annualized revenue growth over the last five years was tepid. This was below our standard for the business services sector.  2. Mediocre Free Cash Flow Margin Limits Reinvestment PotentialFree cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king. Plexus has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.9%, subpar for a business services business.  3. New Investments Fail to Bear Fruit as ROIC DeclinesA company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity). We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Plexus’s ROIC averaged 3.4 percentage point decreases each year. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.  Final JudgmentPlexus falls short of our quality standards. With its shares lagging the market recently, the stock trades at 18.9× forward P/E (or $139.47 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most dominant software business in the world. High-Quality Stocks for All Market ConditionsWhen Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses. Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025). Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today. StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here. More NewsView More

Rubrik’s Massive Rebound: Why the Next Leg Higher Could Be Fast ↗

December 07, 2025

Five Below and Dollar Tree Earnings Signal a Shopper Shift ↗

December 07, 2025

Via MarketBeat

Ulta’s Stock May Be Set for a Glow-Up—20% Upside Ahead? ↗

December 06, 2025

Via MarketBeat

Tickers

ULTA

Gates Foundation Sells MSFT Stock—Should Investors Be Worried? ↗

December 06, 2025

Via MarketBeat

Tickers

MSFT

MarketBeat Week in Review – 12/1 - 12/5 ↗

December 06, 2025

Recent QuotesView More

Stock Quote API & Stock News API supplied by www.cloudquote.io

Quotes delayed at least 20 minutes. By accessing this page, you agree to the Privacy Policy and Terms Of Service.

© 2025 FinancialContent. All rights reserved.

|