With a market cap of $52.7 billion, Corteva, Inc. (CTVA) is an agriculture company, serving markets across North America, Latin America, Asia Pacific, Europe, the Middle East, and Africa. The company operates through two main segments: Seed and Crop Protection, developing advanced seed genetics, traits, and crop protection products to help improve farm productivity and resilience.

Companies worth more than $10 billion are generally labeled as “large-cap” stocks and Corteva fits this criterion perfectly. It also provides herbicides, insecticides, nitrogen stabilizers, and digital farming solutions that support farmers in optimizing crop yield and profitability.

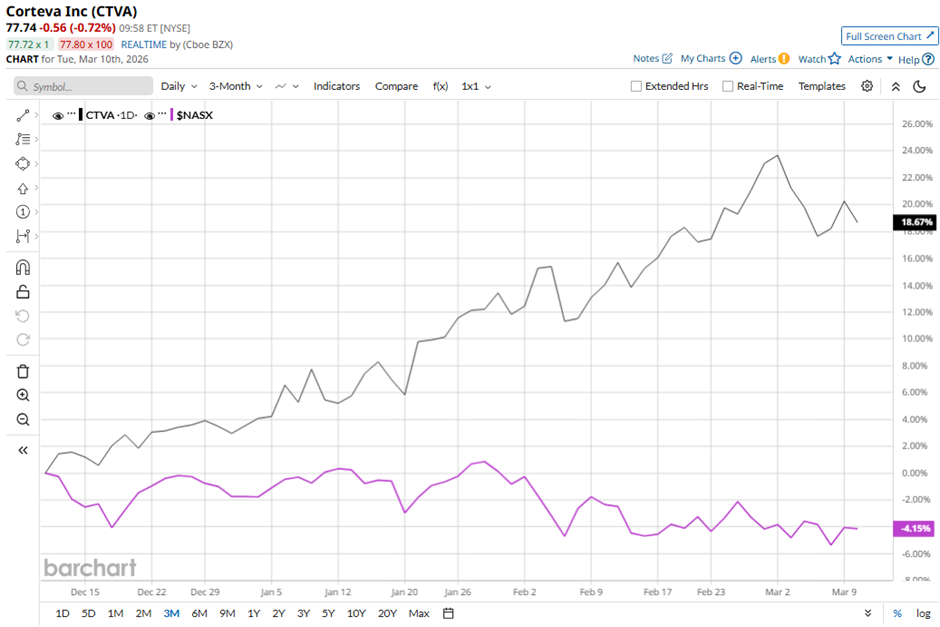

Shares of the Indianapolis, Indiana-based company have decreased 3.9% from its 52-week high of $80.90. Corteva's shares have increased 18.6% over the past three months, outpacing the Nasdaq Composite’s ($NASX) 4% decline over the same time frame.

CTVA stock is up 15.1% on a YTD basis, outperforming NASX’s 2.3% drop. However, longer term, shares of the agricultural technology company have returned 28.1% over the past 52 weeks, lagging behind NASX’s 30% return over the same time frame.

The stock has been trading above its 50-day moving average since late November 2025.

Shares of Corteva rose marginally following its Q4 2025 results on Feb. 3 as adjusted EPS of $0.22 matched Wall Street expectations. The company also highlighted strong full-year performance, reporting $1.20 billion in income ($1.75 per share) on $17.40 billion in sales, while operating cash flow jumped 51% to $3.5 billion and free cash flow rose 69% to $2.9 billion.

In addition, management maintained a 2026 outlook of $4 billion to $4.2 billion in operating EBITDA and $3.45 to $3.70 in operating EPS, supporting investor confidence despite quarterly revenue of $3.91 billion falling short of the consensus estimate.

In comparison, rival CF Industries Holdings, Inc. (CF) has surpassed CTVA stock. Shares of CF Industries have surged 42% over the past 52 weeks and 41.6% on a YTD basis.

Despite CTVA stock’s underperformance over the past year, analysts are moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from the 22 analysts covering the stock, and the mean price target of $83.35 is a premium of 7.3% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart