Looking back on air freight and logistics stocks’ Q3 earnings, we examine this quarter’s best and worst performers, including United Parcel Service (NYSE: UPS) and its peers.

The growth of e-commerce and global trade continues to drive demand for expedited shipping services, presenting opportunities for air freight companies. The industry continues to invest in advanced technologies such as automated sorting systems and real-time tracking solutions to enhance operational efficiency. Despite the advantages of speed and global reach, air freight and logistics companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

The 7 air freight and logistics stocks we track reported a mixed Q3. As a group, revenues beat analysts’ consensus estimates by 2% while next quarter’s revenue guidance was 15.4% below.

In light of this news, share prices of the companies have held steady as they are up 3.5% on average since the latest earnings results.

United Parcel Service (NYSE: UPS)

Trademarking its recognizable UPS Brown color, UPS (NYSE: UPS) offers package delivery, supply chain management, and freight forwarding services.

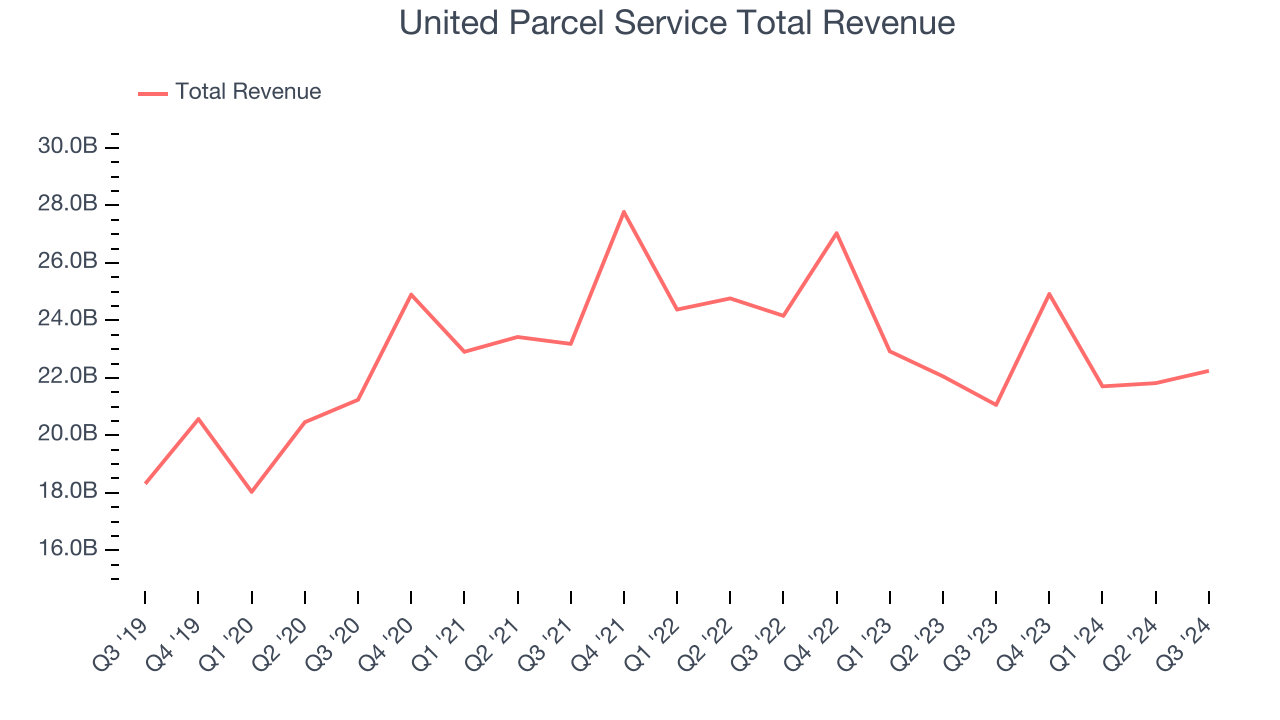

United Parcel Service reported revenues of $22.25 billion, up 5.6% year on year. This print exceeded analysts’ expectations by 0.5%. Overall, it was a strong quarter for the company with a solid beat of analysts’ EBITDA estimates.

“I want to thank all UPSers for their hard work and efforts. After a challenging 18-month period, our company returned to revenue and profit growth,” said Carol Tomé, UPS chief executive officer.

United Parcel Service pulled off the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 3.1% since reporting and currently trades at $135.40.

Is now the time to buy United Parcel Service? Access our full analysis of the earnings results here, it’s free.

Best Q3: Expeditors (NYSE: EXPD)

Expeditors (NYSE: EXPD) offers air and ocean freight as well as brokerage services.

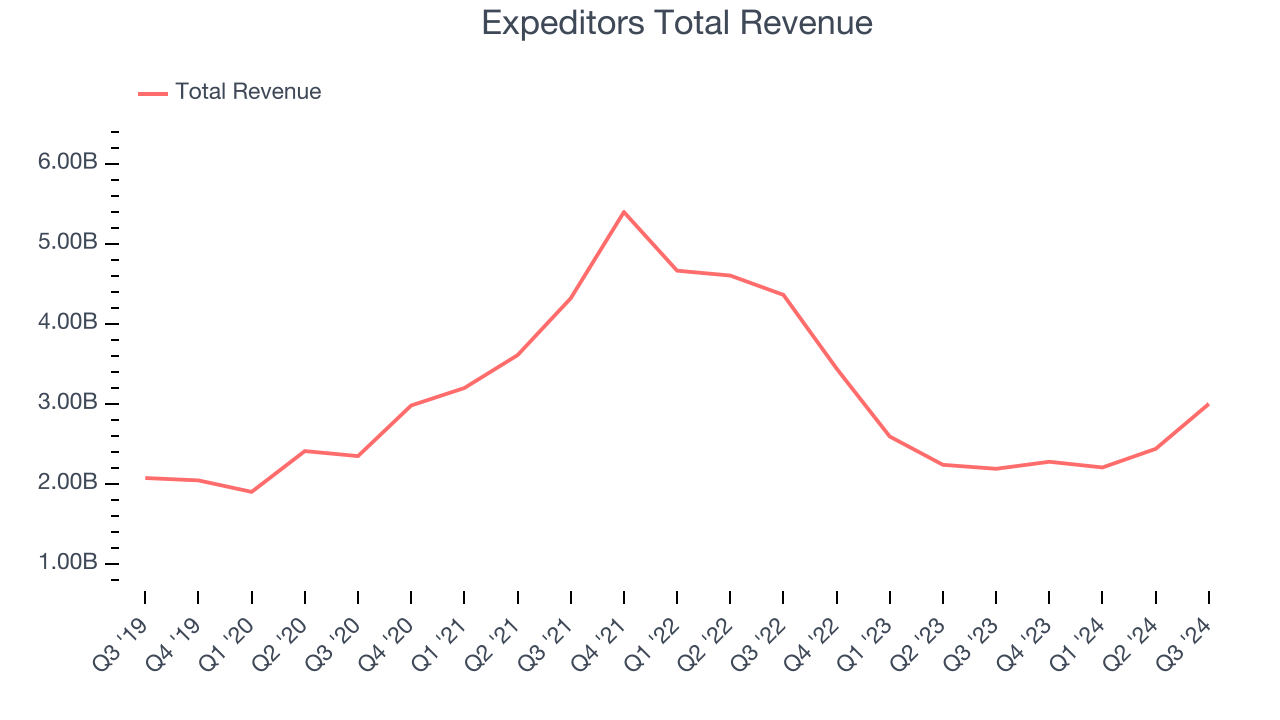

Expeditors reported revenues of $3 billion, up 37% year on year, outperforming analysts’ expectations by 21.3%. The business had an incredible quarter with a solid beat of analysts’ EBITDA estimates.

Expeditors pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems content with the results as the stock is up 1.4% since reporting. It currently trades at $121.99.

Is now the time to buy Expeditors? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: FedEx (NYSE: FDX)

Sporting one of the largest air cargo fleets in the world, FedEx (NYSE: FDX) is a global provider of parcel and cargo delivery services.

FedEx reported revenues of $21.58 billion, flat year on year, falling short of analysts’ expectations by 1.5%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

Interestingly, the stock is up 1.1% since the results and currently trades at $303.85.

Read our full analysis of FedEx’s results here.

Hub Group (NASDAQ: HUBG)

Started with $10,000, Hub Group (NASDAQ: HUBG) is a provider of intermodal, truck brokerage, and logistics services, facilitating transportation solutions for businesses worldwide.

Hub Group reported revenues of $986.9 million, down 3.7% year on year. This print missed analysts’ expectations by 7.1%. Overall, it was a softer quarter as it also produced a significant miss of analysts’ EPS estimates and full-year revenue guidance missing analysts’ expectations.

Hub Group had the weakest full-year guidance update among its peers. The stock is up 18.9% since reporting and currently trades at $52.02.

Read our full, actionable report on Hub Group here, it’s free.

C.H. Robinson Worldwide (NASDAQ: CHRW)

Engaging in contracts with tens of thousands of transportation companies, C.H. Robinson (NASDAQ: CHRW) offers freight transportation and logistics services.

C.H. Robinson Worldwide reported revenues of $4.64 billion, up 7% year on year. This number surpassed analysts’ expectations by 2.4%. It was an exceptional quarter as it also put up an impressive beat of analysts’ EBITDA estimates.

The stock is down 3% since reporting and currently trades at $106.36.

Read our full, actionable report on C.H. Robinson Worldwide here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), has fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty heading into 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.