Since September 2020, the S&P 500 has delivered a total return of 98.1%. But one standout stock has more than doubled the market - over the past five years, JPMorgan Chase has surged 228% to $315.97 per share. Its momentum hasn’t stopped as it’s also gained 28.8% in the last six months thanks to its solid quarterly results, beating the S&P by 10.2%.

Is now the time to buy JPMorgan Chase, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is JPMorgan Chase Not Exciting?

Despite the momentum, we don't have much confidence in JPMorgan Chase. Here are three reasons there are better opportunities than JPM and a stock we'd rather own.

1. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect JPMorgan Chase’s net interest income to rise by 2.4%, a deceleration versus its 7.8% annualized growth for the past two years. This projection is below its 7.8% annualized growth rate for the past two years.

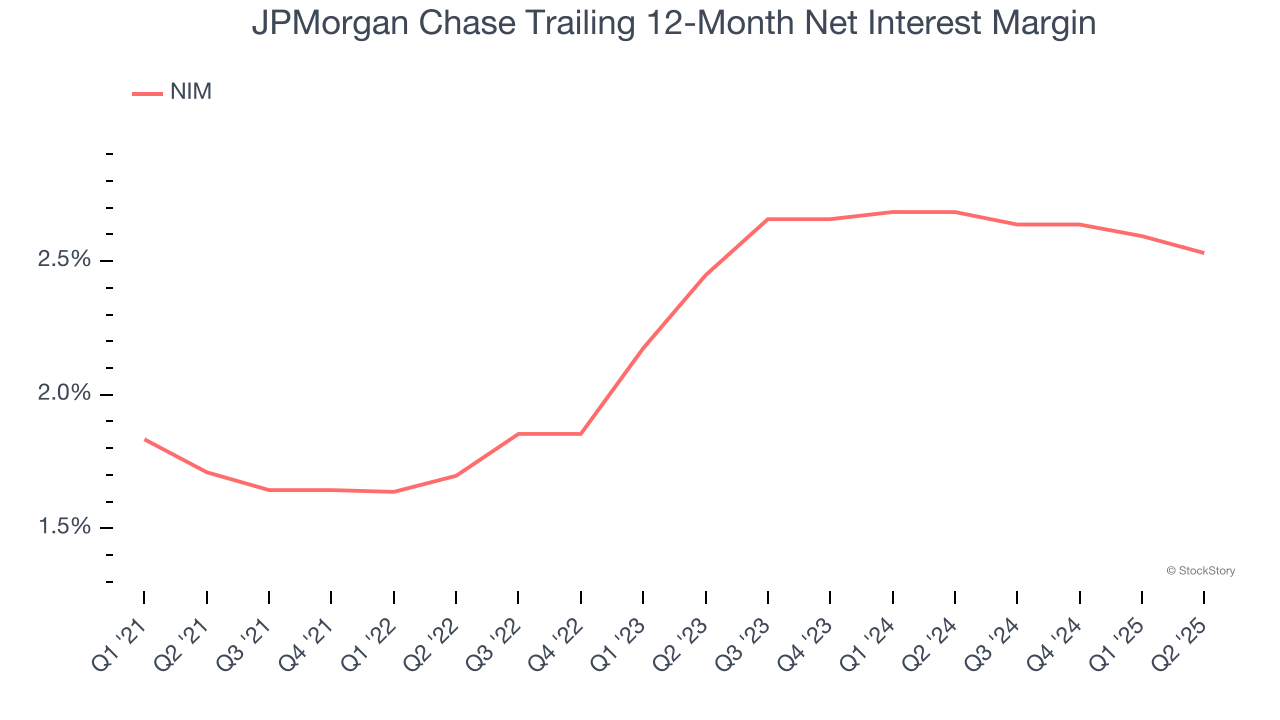

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, we can see that JPMorgan Chase’s net interest margin averaged a poor 2.6%. This metric is well below other banks, signaling its loans aren’t very profitable.

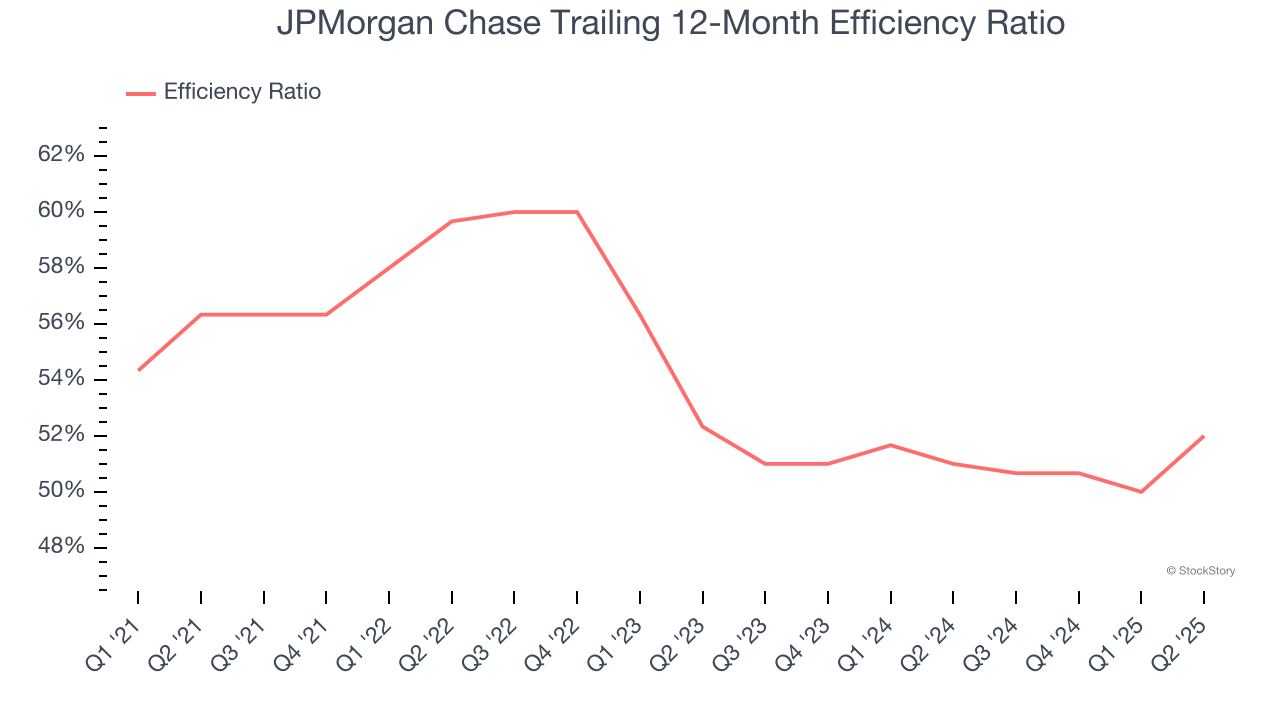

3. Efficiency Ratio Expected to Falter

Topline growth is certainly important, but the overall profitability of this growth matters for the bottom line. For banks, we look at efficiency ratio, which is non-interest expense (salaries, rent, IT, marketing, excluding interest paid out to depositors) as a percentage of total revenue.

Investors place greater emphasis on efficiency ratio movements than absolute values, understanding that expense structures reflect revenue mix variations. Lower ratios represent better operational performance since they show banks generating more revenue per dollar of expense.

For the next 12 months, Wall Street expects JPMorgan Chase to become less profitable as it anticipates an efficiency ratio of 54.6% compared to 52% over the past year.

Final Judgment

JPMorgan Chase isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 2.5× forward P/B (or $315.97 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of JPMorgan Chase

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.