General Mills (NYSE: GIS) can provide a hedge if volatility continues to plague the S&P 500. The company is amid a business transformation telegraphed in its price action, which is set up for a significant reversal after more than a year of lackluster performance.

The transformation includes selling its yogurt business, which will lighten the portfolio and shore up the fortress balance sheet. This will allow management to focus on core markets, international growth, and local gems that drive margin while providing steady capital returns.

The bonus is the stock beta. General Mills has trades with a 5-year beat of 0.1 and a 2-year beta of -.2, suggesting little to no correlation to the S&P 500; if the broad market falls, General Mills trends will be unaffected and may even get an added boost from a flight to safety.

General Mills Post Earnings Dip Is A Buying Opportunity That Won’t Last Long

General Mills share prices fell following the FQ1 release, opening a buying opportunity that will likely last only a short time. The results and guidance were good, with Q1 performance being better than expected, and guidance was reaffirmed. The problem is that Q1 strength didn’t carry through to the guidance, suggesting the remainder of the year could be tepid relative to expectations. However, the $4.85 billion in revenue is down only 1% compared to last year, outperforming by 100 basis points, and aligns with the outlook for turnaround, resumed organic growth, and capital returns, which counts over the long term.

The margin news is just as mixed, with margins contracting but less than expected, leaving earnings down compared to last year but better than forecast. The salient detail is that although net earnings are down 14%, the $580 million is sufficient to sustain the fortress balance sheet and the capital return. The $1.07 in adjusted earnings gives a 55% quarterly dividend payout ratio, which is sustainable and expected to improve as the year progresses. It also leaves room for share repurchases, which have been aggressive.

The guidance is good enough. The company forecasts sequential improvement in revenue and earnings and YOY organic growth to return by the end of the year, not including the sale of the yogurt business. That is expected to close in 2025 and will impact reported results for the following twelve months by approximately 3% on a diluted basis.

General Mills Capital Return Is Top-Tier and Expected to Accelerate

General Mills' financial condition is rock solid and allows for substantial capital return, including dividends and share buybacks. The dividend is attractive at 3.25% and only 16x earnings, a high-yield value compared to the broad market and leading consumer staples peers like Hormel (NYSE: HRL), Hershey (NYSE: HSY), and Kellanova (NYSE: K), which trade at 20x, 21x, and nearly 22x their earnings outlooks, respectively.

Balance sheet highlights from Q1 include reduced cash, increased debt, and reduced equity, but repurchases and treasury stock offset those factors. The company repurchased $300 million of shares during the quarter, reducing the average count by 4.65% year over year and increasing the treasury holdings by nearly 20%. Repurchases have slowed compared to last year due to the contraction of revenue and earnings, and they may not accelerate soon. However, buybacks are likely to continue at a float-reducing pace through the year’s end, and the company plans to use proceeds from the yogurt sale to boost activity once closed.

General Mills Share Price Supported by an Expectation for Lower Interest Rates

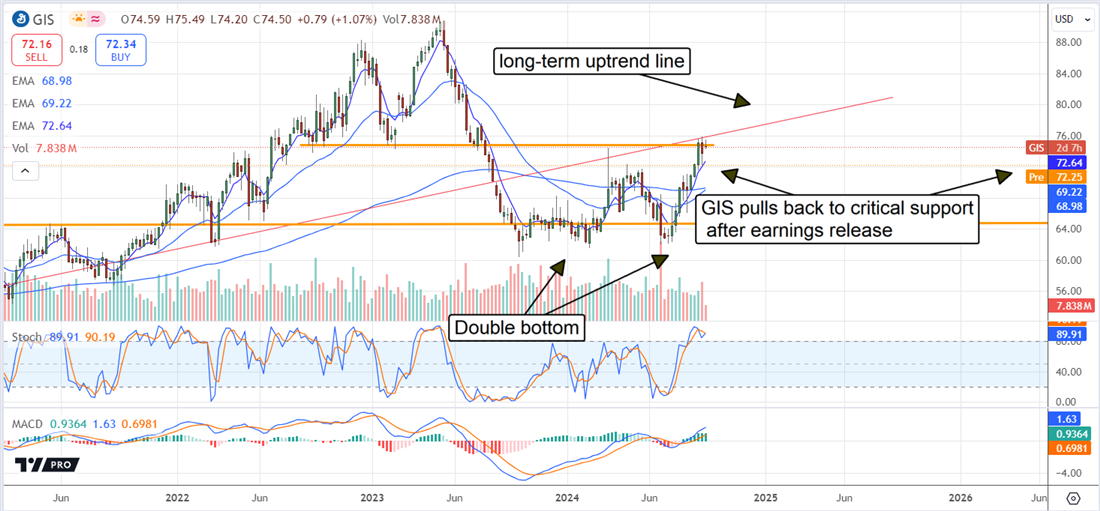

General Mills' share price has steadily risen since mid-July, when the CPI report sparked a massive broad-market sell-off after signaling a high probability that the FOMC would lower interest rates this year. The signal is that risk-off investment dollars, once focused on higher-yielding bonds, have turned to quality dividend growth stocks like General Mills, which still present value and yield for investors today.

The technical action since July suggests a double-bottom reversal pattern is now in play, and price action has retreated to a critical support target. The critical target is the 30-day EMA, which aligns with highs earlier this year. If support is confirmed at this level, investors can expect GIS stock to continue higher and complete the reversal by year’s end. If not, GIS stock could fall to the $70 level or lower before hitting solid support.