Illinois Tool Works trades at $258.77 and has moved in lockstep with the market. Its shares have returned 9% over the last six months while the S&P 500 has gained 9.7%.

Is there a buying opportunity in Illinois Tool Works, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.We're swiping left on Illinois Tool Works for now. Here are three reasons why you should be careful with ITW and a stock we'd rather own.

Why Is Illinois Tool Works Not Exciting?

Founded by Byron Smith, an investor who held over 100 patents, Illinois Tool Works (NYSE: ITW) manufactures engineered components and specialized equipment for numerous industries.

1. Long-Term Revenue Growth Disappoints

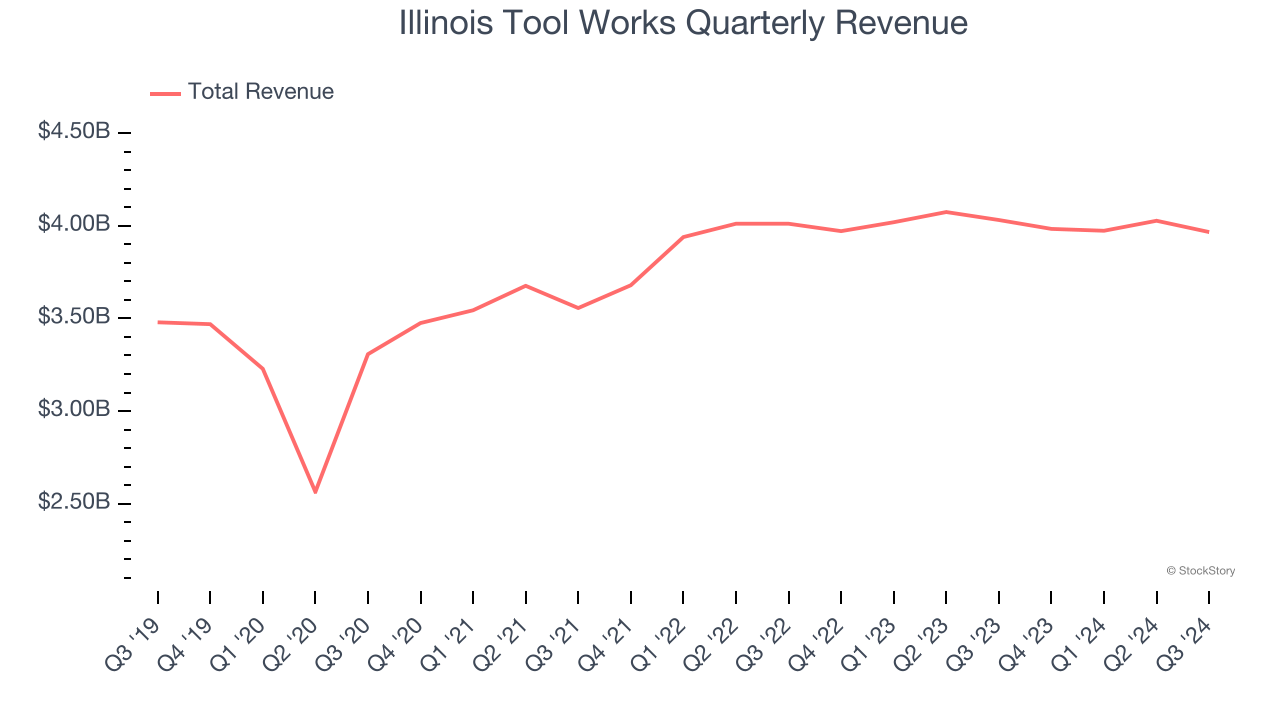

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Illinois Tool Works’s 2.3% annualized revenue growth over the last five years was sluggish. This was below our standards.

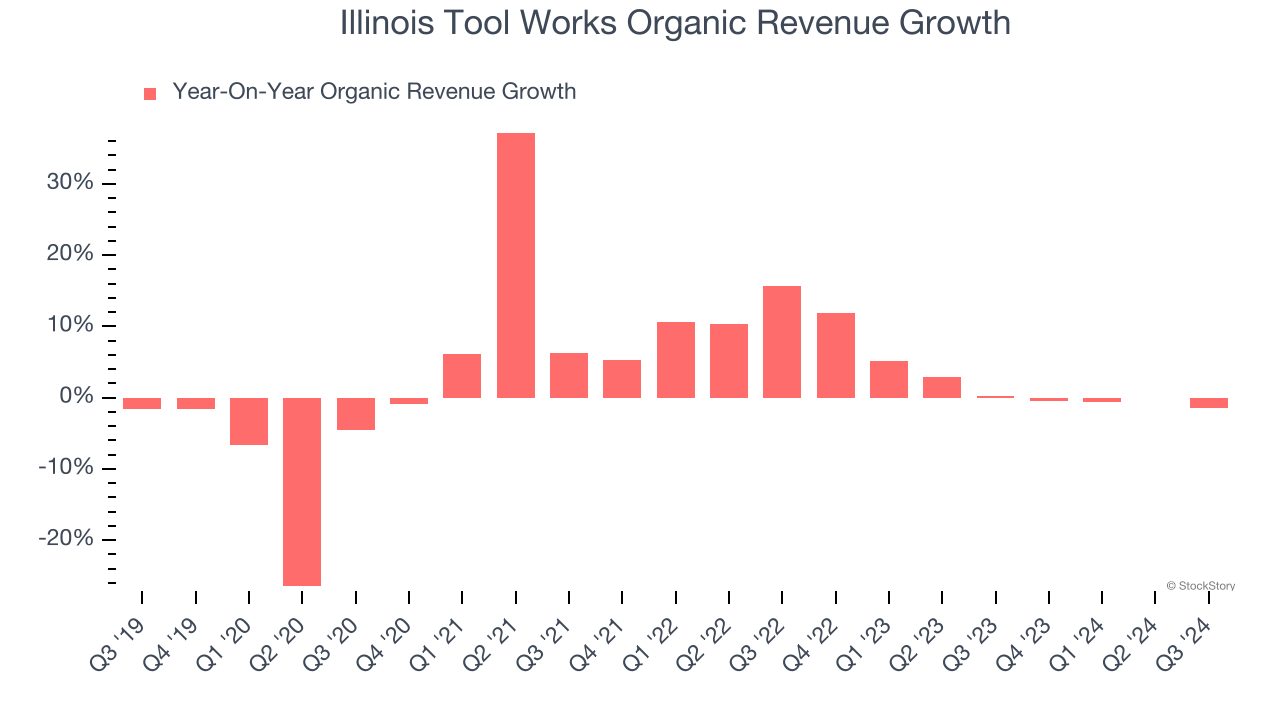

2. Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand General Industrial Machinery companies by analyzing their organic revenue. This metric gives visibility into Illinois Tool Works’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Illinois Tool Works’s organic revenue averaged 2.2% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

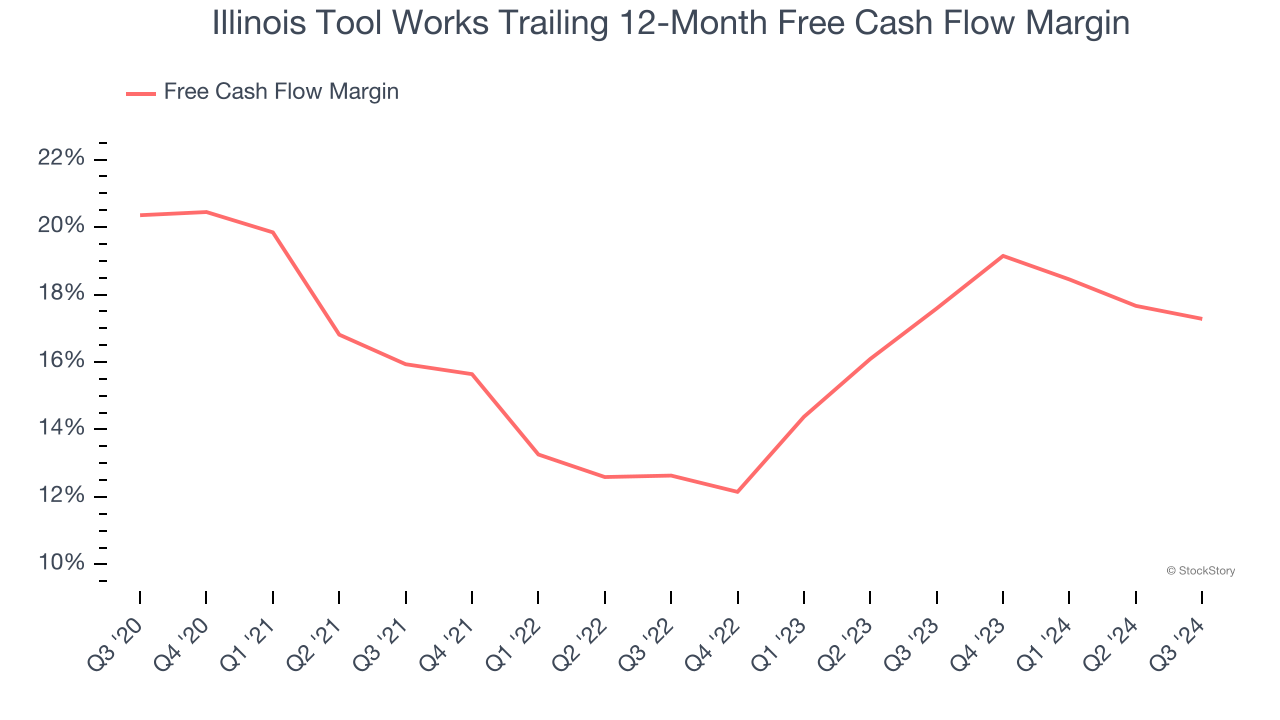

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Illinois Tool Works’s margin dropped by 3.1 percentage points over the last five years. If its declines continue, it could signal higher capital intensity. Illinois Tool Works’s free cash flow margin for the trailing 12 months was 17.3%.

Final Judgment

Illinois Tool Works isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 24.5× forward price-to-earnings (or $258.77 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. We’d suggest looking at TransDigm, a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Illinois Tool Works

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.