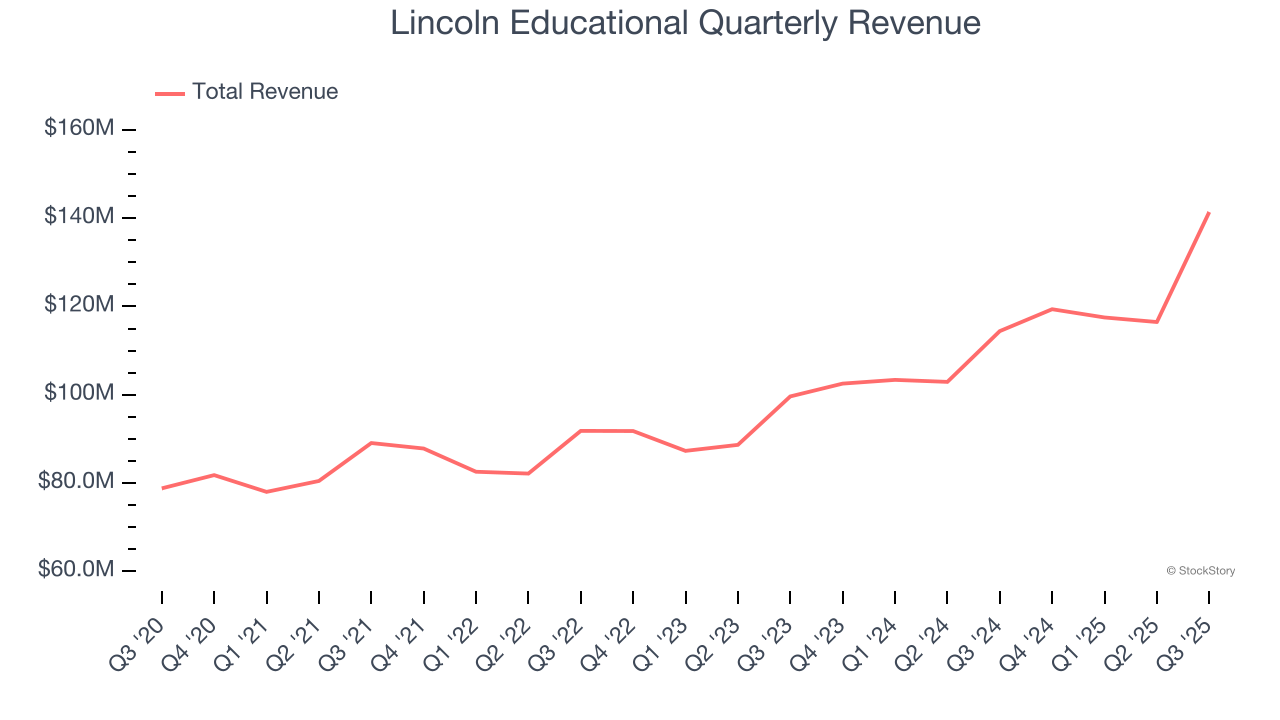

Education company Lincoln Educational (NASDAQ: LINC) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 23.6% year on year to $141.4 million. The company’s full-year revenue guidance of $507.5 million at the midpoint came in 2.8% above analysts’ estimates. Its GAAP profit of $0.12 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Lincoln Educational? Find out by accessing our full research report, it’s free for active Edge members.

Lincoln Educational (LINC) Q3 CY2025 Highlights:

- Revenue: $141.4 million vs analyst estimates of $131.5 million (23.6% year-on-year growth, 7.5% beat)

- EPS (GAAP): $0.12 vs analyst estimates of $0.02 (significant beat)

- Adjusted EBITDA: $16.9 million vs analyst estimates of $12.88 million (12% margin, 31.2% beat)

- The company lifted its revenue guidance for the full year to $507.5 million at the midpoint from $495 million, a 2.5% increase

- EBITDA guidance for the full year is $66 million at the midpoint, above analyst estimates of $61.84 million

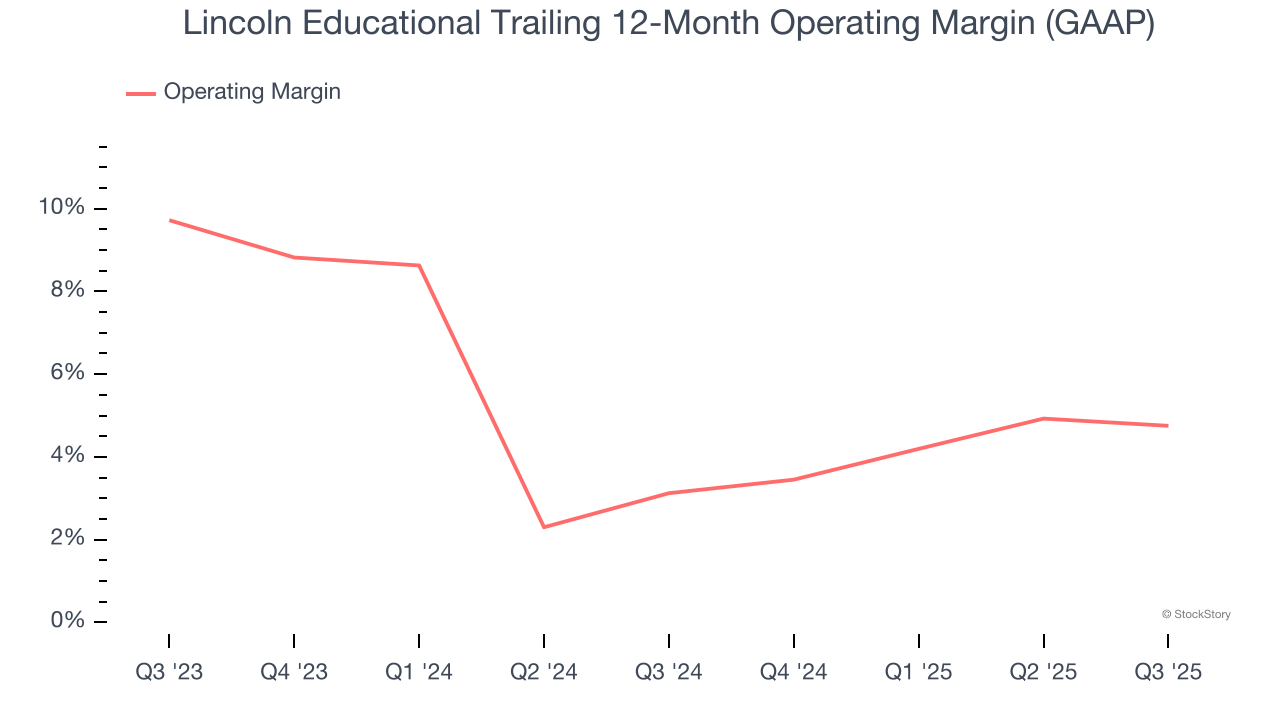

- Operating Margin: 4.4%, in line with the same quarter last year

- Free Cash Flow was $5.53 million, up from -$13.76 million in the same quarter last year

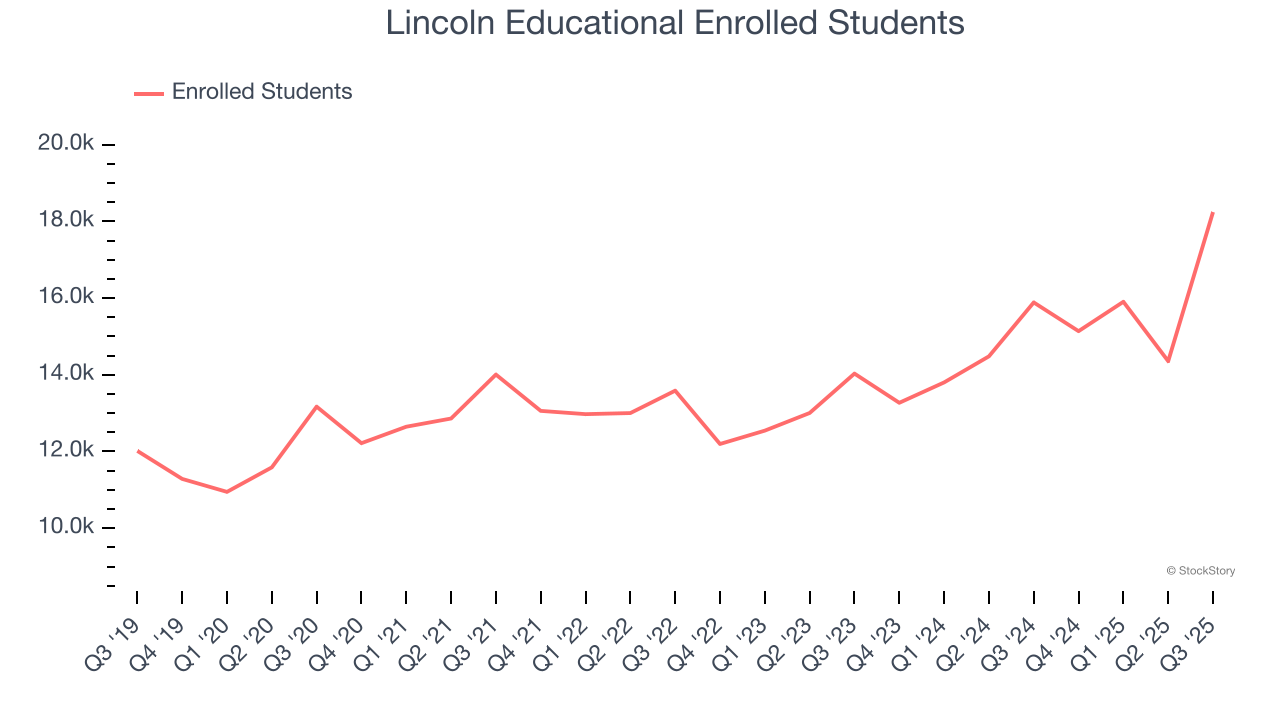

- Enrolled Students: 18,244, up 2,357 year on year

- Market Capitalization: $562.8 million

“As the demand for high-value career-focused training continues to reach new heights across America, Lincoln’s proven expertise, innovative training platforms, and campus development strategies are creating sustained levels of growth,” said Scott Shaw, President and Chief Executive Officer.

Company Overview

Established in 1946, Lincoln Educational (NASDAQ: LINC) is a provider of specialized technical training in the United States, offering career-oriented programs to provide practical skills required in the workforce.

Revenue Growth

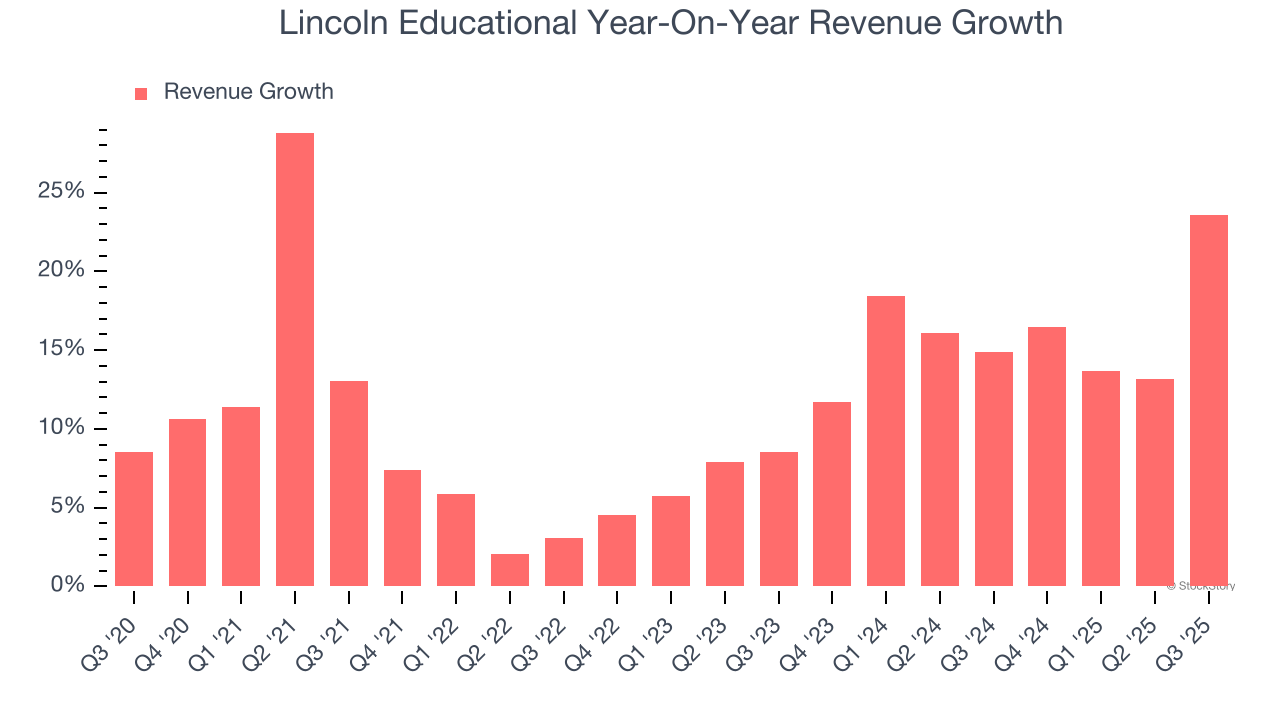

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Lincoln Educational grew its sales at a 11.6% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Lincoln Educational’s annualized revenue growth of 16.1% over the last two years is above its five-year trend, suggesting some bright spots.

We can dig further into the company’s revenue dynamics by analyzing its number of enrolled students, which reached 18,244 in the latest quarter. Over the last two years, Lincoln Educational’s enrolled students averaged 10.8% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Lincoln Educational reported robust year-on-year revenue growth of 23.6%, and its $141.4 million of revenue topped Wall Street estimates by 7.5%.

Looking ahead, sell-side analysts expect revenue to grow 7.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Lincoln Educational’s operating margin has risen over the last 12 months and averaged 4% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

This quarter, Lincoln Educational generated an operating margin profit margin of 4.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

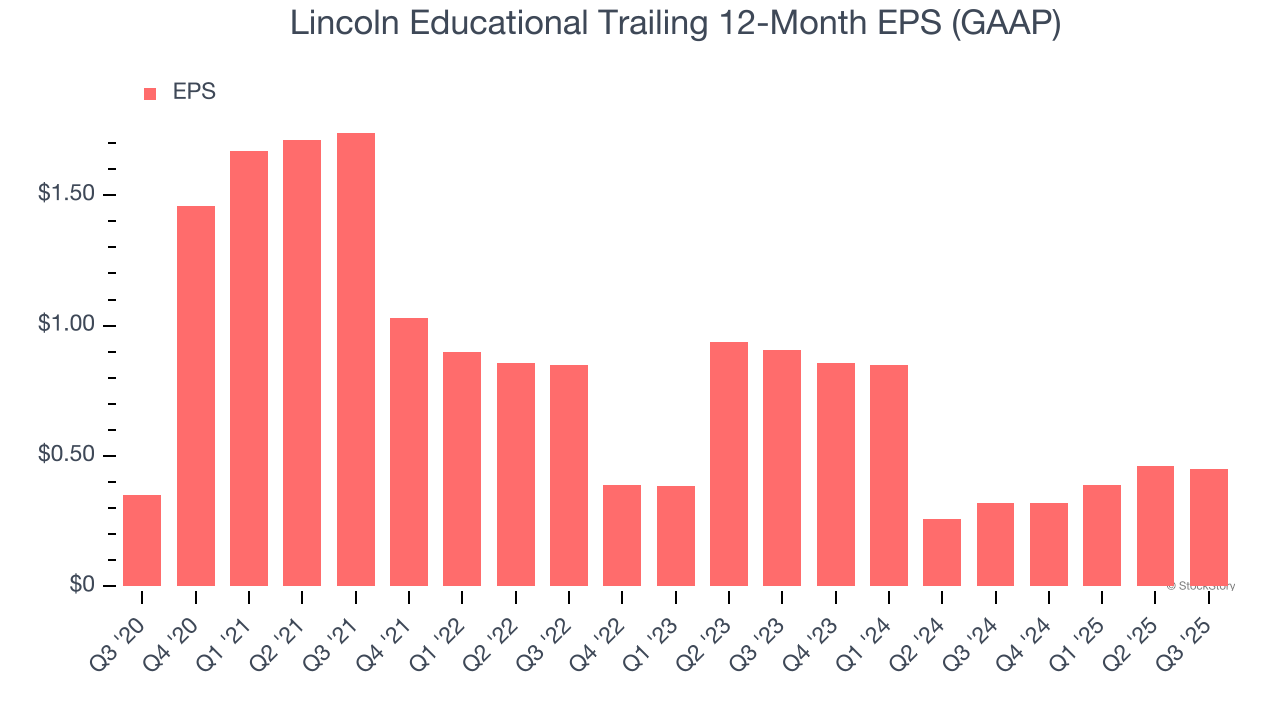

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Lincoln Educational’s EPS grew at an unimpressive 5.2% compounded annual growth rate over the last five years, lower than its 11.6% annualized revenue growth. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

In Q3, Lincoln Educational reported EPS of $0.12, down from $0.13 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Lincoln Educational’s full-year EPS of $0.45 to grow 36.7%.

Key Takeaways from Lincoln Educational’s Q3 Results

It was good to see Lincoln Educational beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 10.3% to $19.66 immediately following the results.

Lincoln Educational had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.