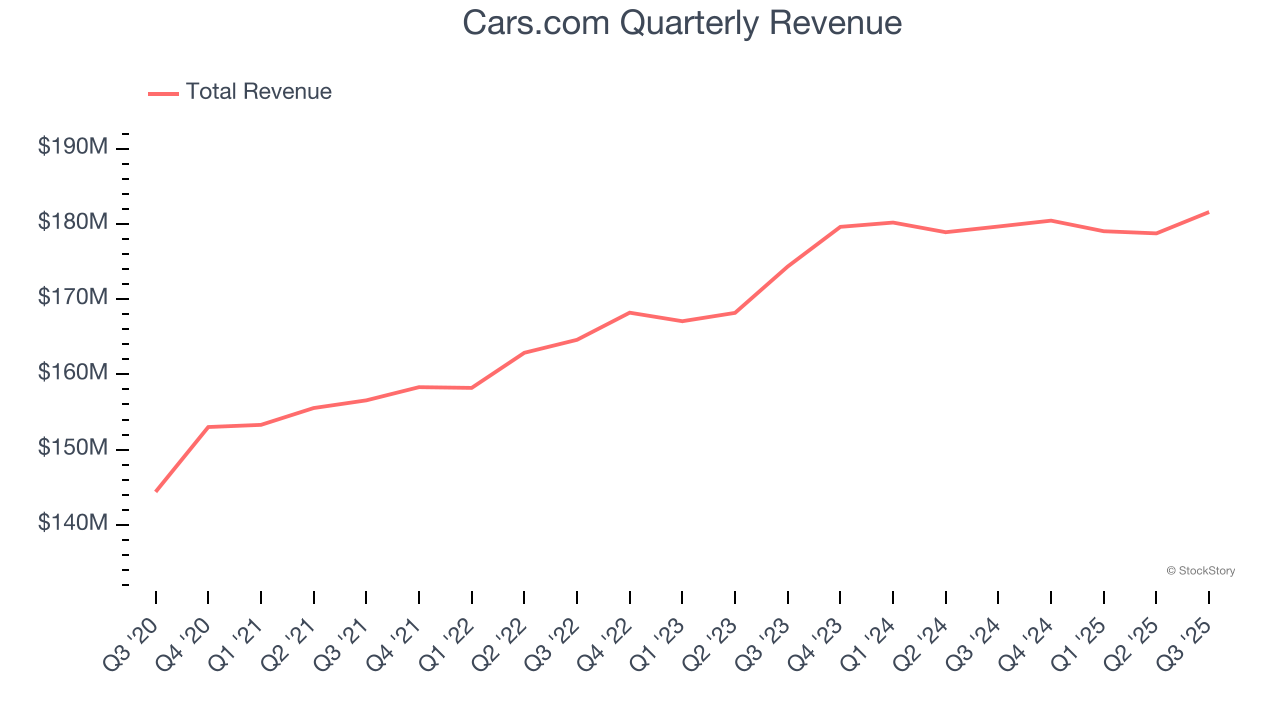

Online new and used car marketplace Cars.com (NYSE: CARS) met Wall Streets revenue expectations in Q3 CY2025, with sales up 1.1% year on year to $181.6 million. Its non-GAAP profit of $0.48 per share was in line with analysts’ consensus estimates.

Is now the time to buy Cars.com? Find out by accessing our full research report, it’s free for active Edge members.

Cars.com (CARS) Q3 CY2025 Highlights:

- Revenue: $181.6 million vs analyst estimates of $181.4 million (1.1% year-on-year growth, in line)

- Adjusted EPS: $0.48 vs analyst estimates of $0.49 (in line)

- Adjusted EBITDA: $54.63 million vs analyst estimates of $53.51 million (30.1% margin, 2.1% beat)

- Operating Margin: 9.3%, up from 6.4% in the same quarter last year

- Free Cash Flow Margin: 29%, up from 10.2% in the previous quarter

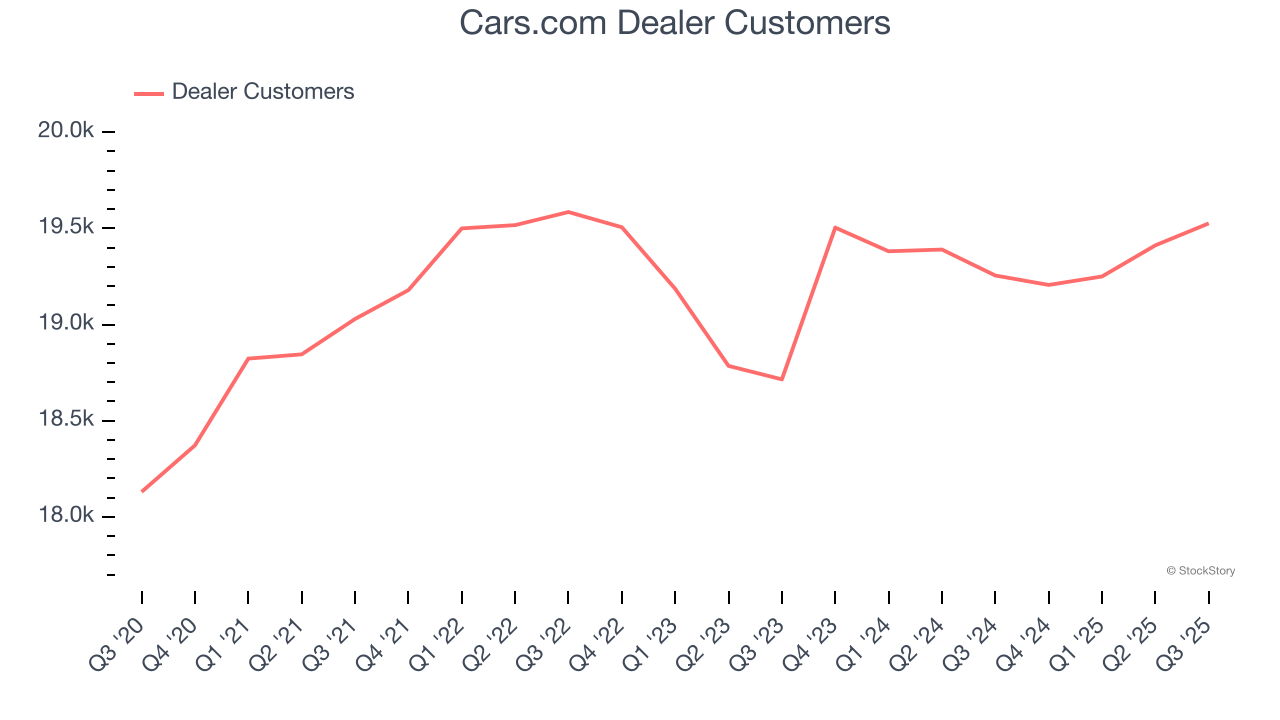

- Dealer Customers: 19,526, up 271 year on year

- Market Capitalization: $639.6 million

Company Overview

Originally started as a joint venture between several media companies including The Washington Post and The New York Times, Cars.com (NYSE: CARS) is a digital marketplace that connects new and used car buyers and sellers.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Cars.com grew its sales at a sluggish 3.8% compounded annual growth rate. This was below our standard for the consumer internet sector and is a rough starting point for our analysis.

This quarter, Cars.com grew its revenue by 1.1% year on year, and its $181.6 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, similar to its three-year rate. This projection is underwhelming and implies its products and services will face some demand challenges.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Dealer Customers

Buyer Growth

As an online marketplace, Cars.com generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Cars.com struggled with new customer acquisition over the last two years as its dealer customers were flat at 19,526. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Cars.com wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

Luckily, Cars.com added 271 dealer customers in Q3, leading to 1.4% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating buyer growth just yet.

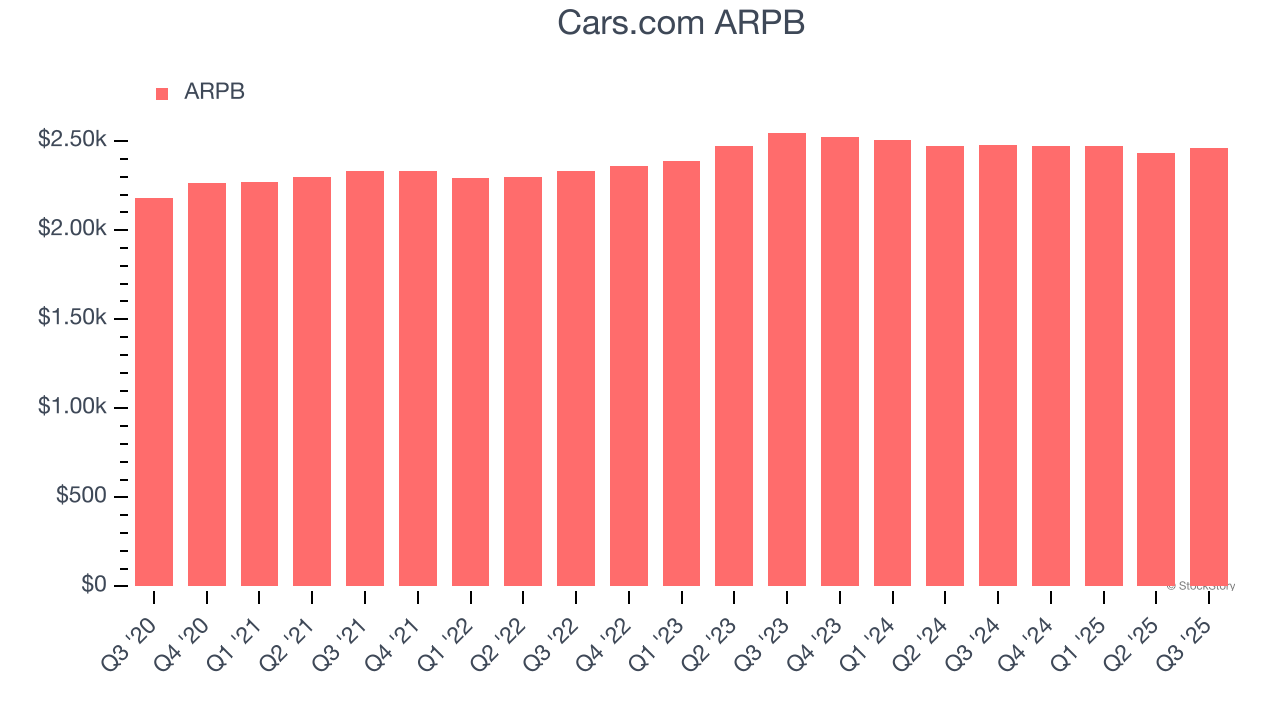

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the company earns in transaction fees from each buyer. ARPB also gives us unique insights into a user’s average order size and Cars.com’s take rate, or "cut", on each order.

Cars.com’s ARPB has been roughly flat over the last two years. This raises questions about its platform’s health when paired with its inability to grow dealer customers. If Cars.com wants to increase its buyers, it must either develop new features or provide some existing ones for free.

This quarter, Cars.com’s ARPB clocked in at $2,460. It was flat year on year, worse than the change in its dealer customers.

Key Takeaways from Cars.com’s Q3 Results

It was encouraging to see Cars.com beat analysts’ EBITDA expectations this quarter.Zooming out, we think this was a decent quarter. The stock traded up 5.3% to $10.93 immediately following the results.

Is Cars.com an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.