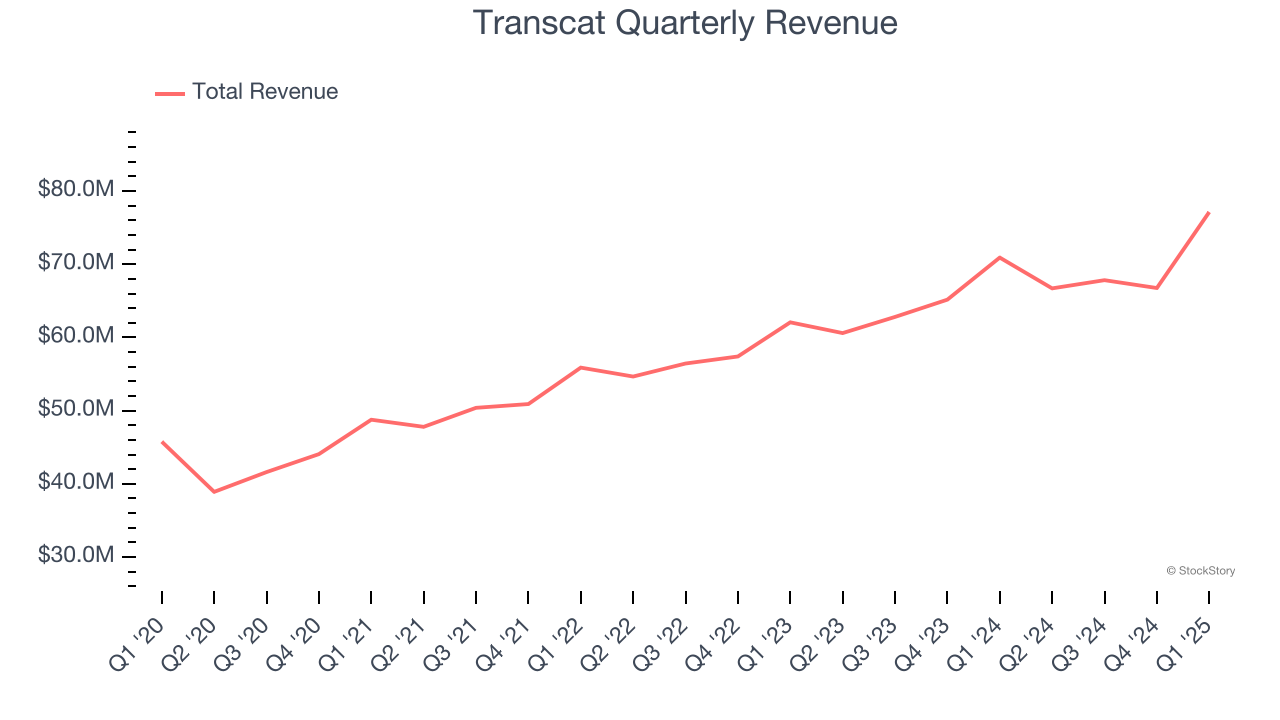

Measurement equipment distributor Transcat (NASDAQ: TRNS) announced better-than-expected revenue in Q1 CY2025, with sales up 8.8% year on year to $77.13 million. Its non-GAAP profit of $0.64 per share was 3.8% above analysts’ consensus estimates.

Is now the time to buy Transcat? Find out by accessing our full research report, it’s free.

Transcat (TRNS) Q1 CY2025 Highlights:

- Revenue: $77.13 million vs analyst estimates of $76.4 million (8.8% year-on-year growth, 1% beat)

- Adjusted EPS: $0.64 vs analyst estimates of $0.62 (3.8% beat)

- Adjusted EBITDA: $12.75 million vs analyst estimates of $11 million (16.5% margin, 15.9% beat)

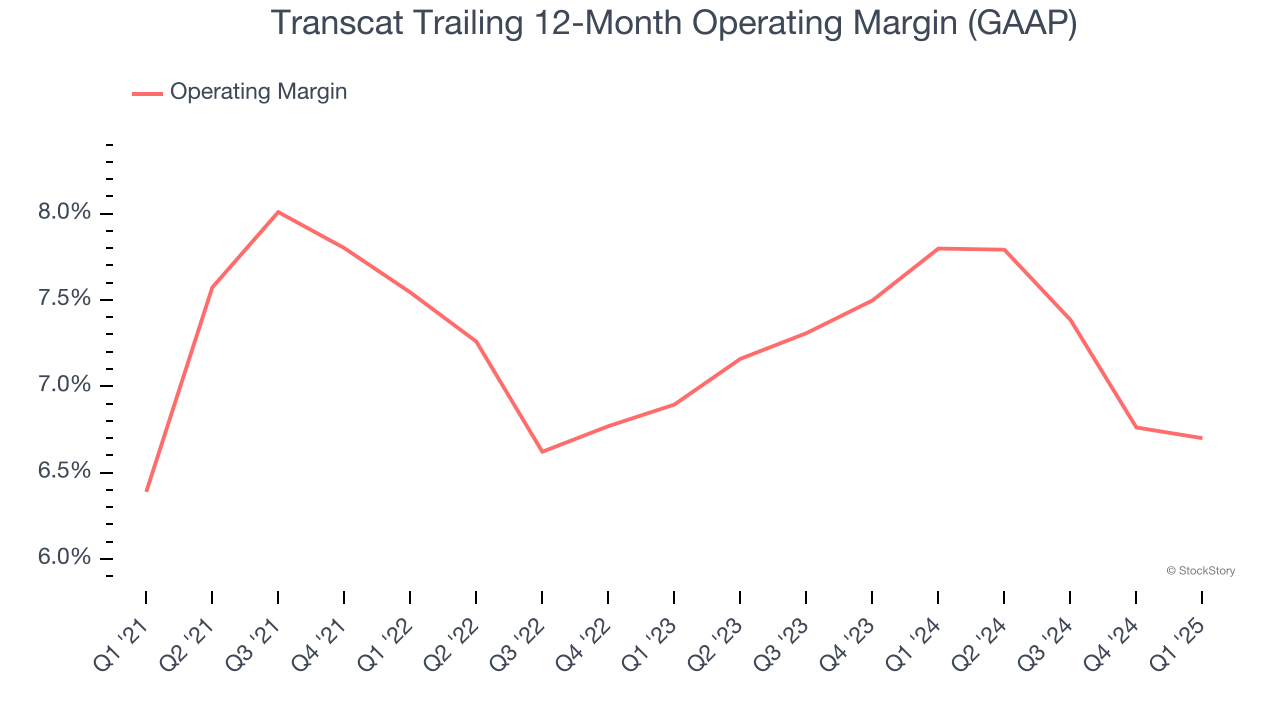

- Operating Margin: 9%, in line with the same quarter last year

- Free Cash Flow Margin: 10.3%, up from 2.2% in the same quarter last year

- Market Capitalization: $756.4 million

“Consolidated revenue grew 9% in the fiscal fourth quarter as strength in the Calibration business drove double-digit Service revenue growth and margin expansion,” said Lee D. Rudow, President and CEO of Transcat.

Company Overview

Serving the pharmaceutical, industrial manufacturing, energy, and chemical process industries, Transcat (NASDAQ: TRNS) provides measurement instruments and supplies.

Sales Growth

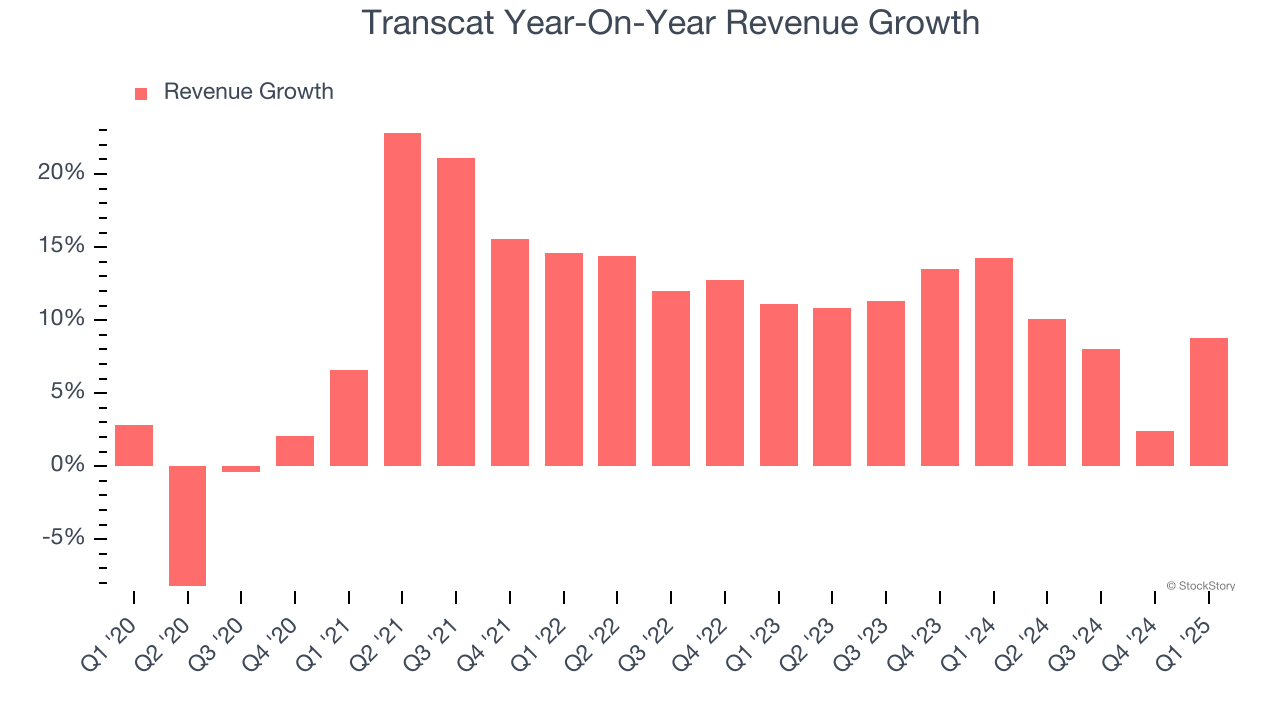

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Transcat’s sales grew at a solid 10% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Transcat’s annualized revenue growth of 9.9% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Transcat reported year-on-year revenue growth of 8.8%, and its $77.13 million of revenue exceeded Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, similar to its two-year rate. This projection is commendable and suggests the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Transcat was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.1% was weak for an industrials business.

Looking at the trend in its profitability, Transcat’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Transcat generated an operating profit margin of 9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

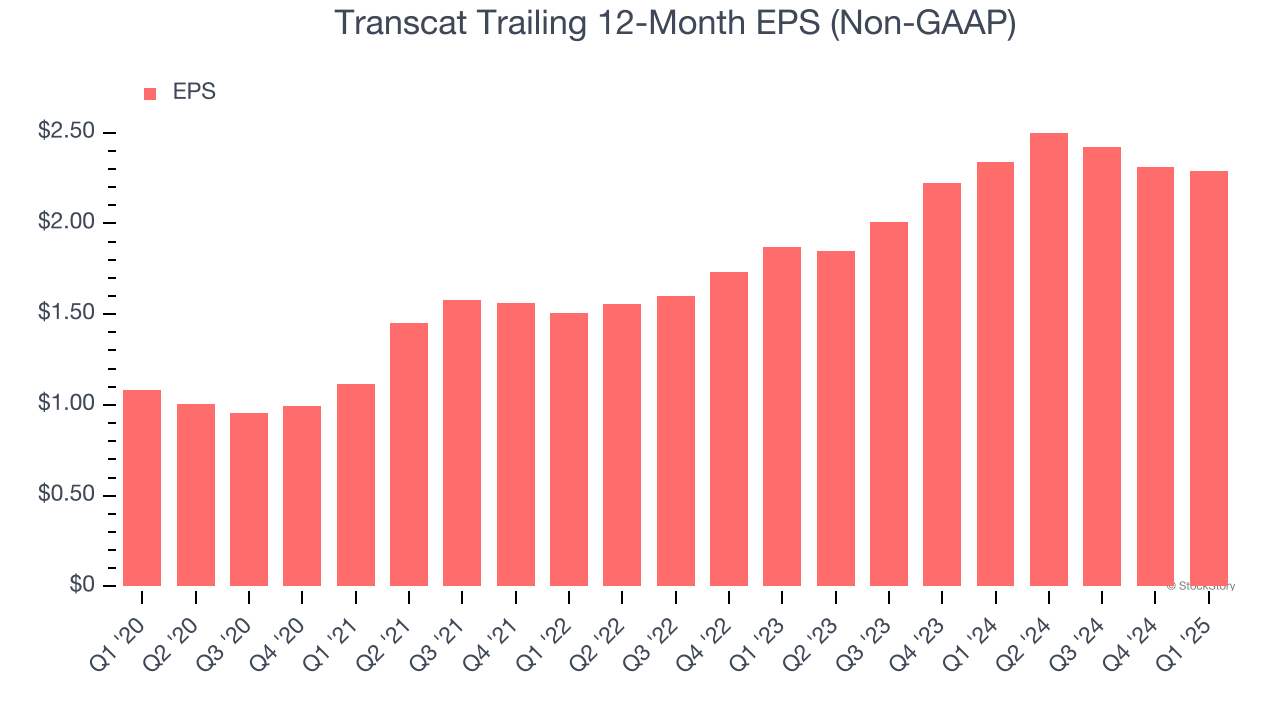

Transcat’s EPS grew at a spectacular 16.2% compounded annual growth rate over the last five years, higher than its 10% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t expand and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Transcat, its two-year annual EPS growth of 10.7% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, Transcat reported EPS at $0.64, down from $0.66 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 3.8%. Over the next 12 months, Wall Street expects Transcat’s full-year EPS of $2.29 to grow 13.3%.

Key Takeaways from Transcat’s Q1 Results

We were impressed by how significantly Transcat blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 7.3% to $87 immediately after reporting.

Transcat put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.