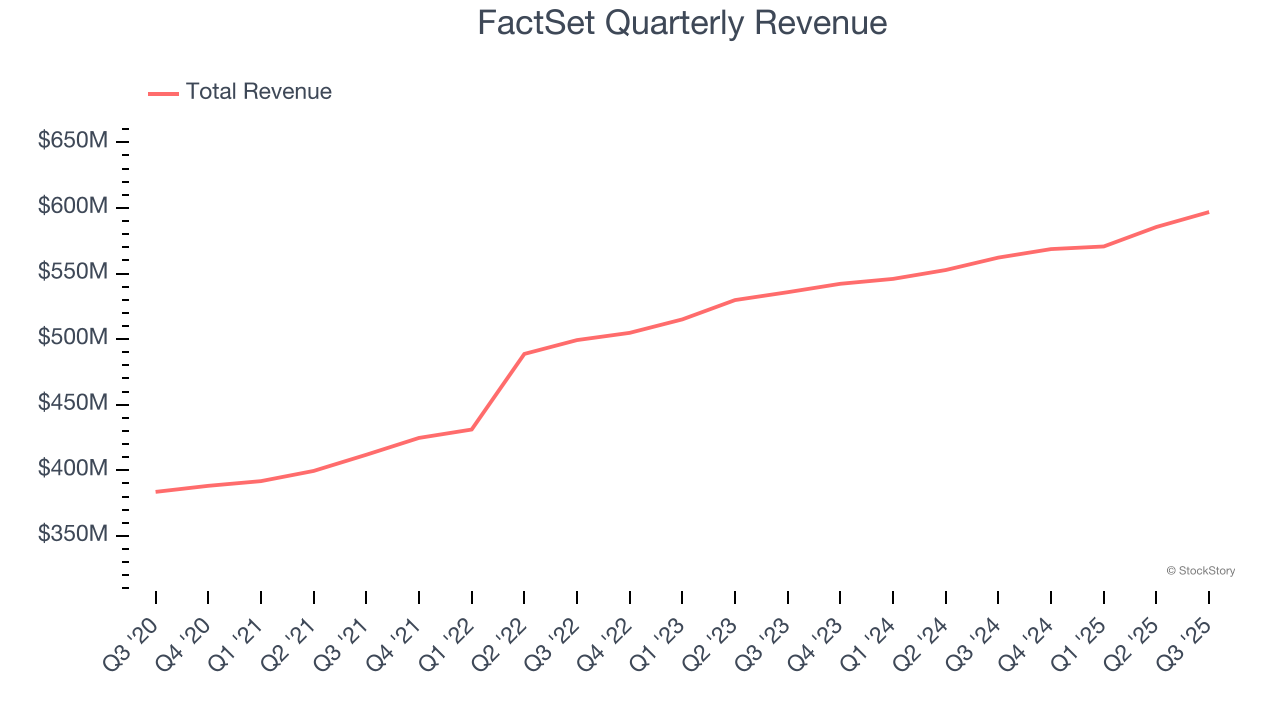

Financial data provider FactSet (NYSE: FDS) announced better-than-expected revenue in Q3 CY2025, with sales up 6.2% year on year to $596.9 million. On the other hand, the company’s full-year revenue guidance of $2.44 billion at the midpoint came in 0.6% below analysts’ estimates. Its non-GAAP profit of $4.05 per share was 1.9% below analysts’ consensus estimates.

Is now the time to buy FactSet? Find out by accessing our full research report, it’s free.

FactSet (FDS) Q3 CY2025 Highlights:

- Revenue: $596.9 million vs analyst estimates of $593.4 million (6.2% year-on-year growth, 0.6% beat)

- Pre-tax Profit: $189 million (31.7% margin, 61.3% year-on-year growth)

- Adjusted EPS: $4.05 vs analyst expectations of $4.13 (1.9% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $17.25 at the midpoint, missing analyst estimates by 5.6%

- Market Capitalization: $12.7 billion

“FactSet’s strong fourth quarter performance reflects the power of our differentiated data, open platform, and client-centric culture,” said Sanoke Viswanathan, CEO of FactSet.

Company Overview

Founded in 1978 when financial data was still primarily delivered through paper reports, FactSet (NYSE: FDS) provides financial data, analytics, and technology solutions that investment professionals use to research, analyze, and manage their portfolios.

Revenue Growth

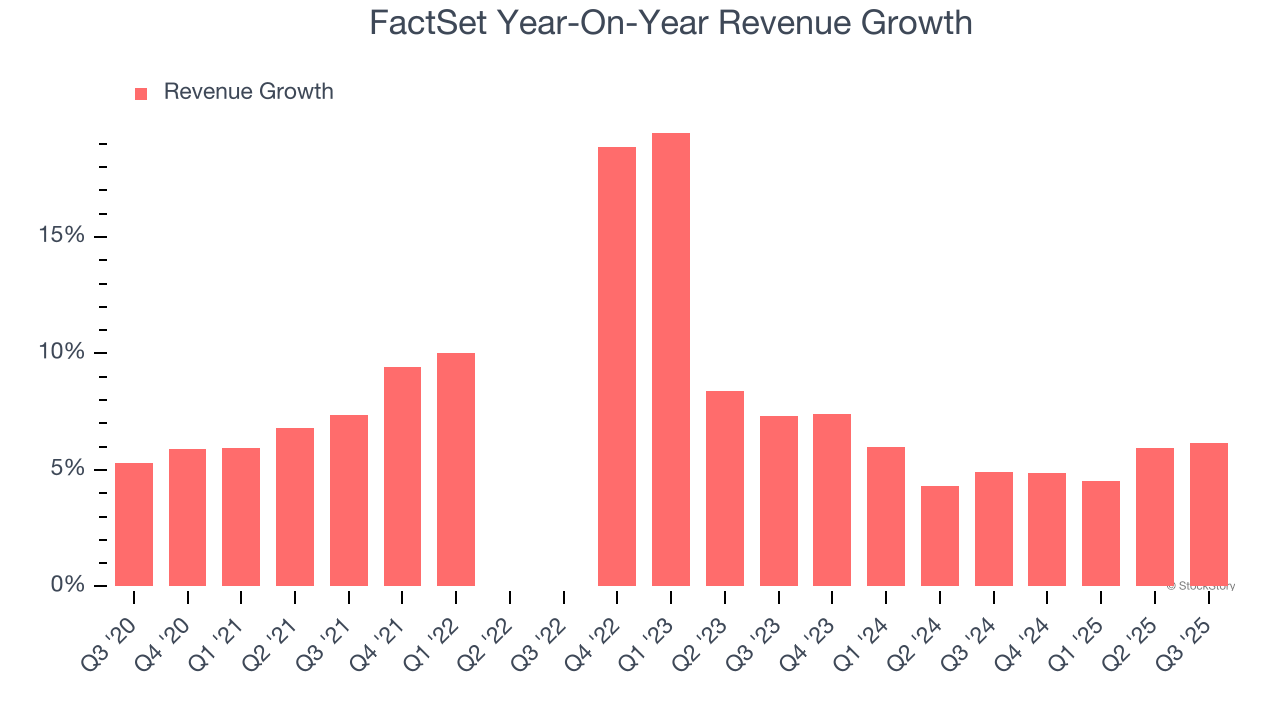

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, FactSet grew its revenue at a decent 9.2% compounded annual growth rate. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. FactSet’s recent performance shows its demand has slowed as its annualized revenue growth of 5.5% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, FactSet reported year-on-year revenue growth of 6.2%, and its $596.9 million of revenue exceeded Wall Street’s estimates by 0.6%.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Key Takeaways from FactSet’s Q3 Results

We were impressed by how significantly FactSet blew past analysts’ EBITDA expectations this quarter. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.8% to $326.34 immediately after reporting.

FactSet’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.