Over the last 10 years, markets ( Equities and Commodities in particular) have shown a strong tendency to ignore classic technical and fundamental analysis.

Algorithms are theoretically based on technical factors like volatility and momentum, but the reality is they are driven by social media posts.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.With the war in Iran escalating, the test will be commodity markets that are rallying without the support of real fundamentals.

Toward the end of January, I gave a market talk at the annual meeting of a local soybean processing company in Omaha. I filled the hour with talk of the economic Law of Supply and Demand, the importance of intrinsic value, basis, and futures spreads – all of our reads on real supply and demand. I discussed my 7 Market Rules, and how if we put everything together, the US soybean situation was as bearish if not more so than a year ago at the same time. Earlier this week, one of the attendees at that meeting called with a simple message, “You were wrong”.

My next speaking engagement is in the Quad Cities area this coming Thursday night. My initial plan was to use an updated version of my previous presentation – something I used to do frequently when my winter travel season was much busier. But I won’t, because none of it matters at this time. Fundamentals don’t matter at this time, and that’s fine. It’s just something we have to accept and move on. How will I spend the hour explaining markets to a group of Midwest producers this week? By talking about Just. One. Thing.

Trend. Price direction over time. Nothing more. That’s all that matters these days. Maybe it’s all that ever mattered, but there was just more to it the past few decades. After all, I did make that Rule #1: Don’t get crossways with the trend. Why? Because of Newton’s First Law of Motion applied to markets: A trending market will still in that trend until acted upon by an outside force. And that outside force has long been the noncommercial (speculative, fund, investment, etc.) side. The most important factor in markets these days is the flow of investment money in a market, either through buying (e.g. soybeans) or selling (e.g. sugar).

Let’s take a quick look at sugar. This past week, as the commodity sector was blowing up – literally due to bombs being dropped on Iran with retaliatory missiles fired back at Israel, I heard from my long-time friend Myra Saefong. Myra is a commodities reporter for MarketWatch who I’ve had the pleasure of working with for years. As I mentioned in a piece I wrote for Barchart, Myra wanted to know how the “conflict” in Iran was affecting the sugar market. (She is much more professional than I am. I call it a “war”.) I took a look and saw that it wasn’t, at least not at the time. In fact, what we’ve seen in sugar futures is a downtrend that has taken the spot-month contract from a high of 27.77 cents (week of October 30, 2023) to a recent low of 13.78 (week of February 9, 2026), a price decrease of 50%. At the same time, according to weekly CFTC Commitments of Traders reports (legacy, futures only) the noncommercial net futures position went form a long of nearly 280,000 contracts to short 254,000 contracts, a switch of more than 530,000 contracts.

Within that switch, Watson (algorithm driven funds) went from a record large long futures position of 354,600 contracts to a record large short futures position of 438,300 contracts, the latter as part of the most recent report for positions as of Tuesday, March 3, 2026 . This could be viewed as a warning flag that the force behind the trend is about to change.

Was there a fundamental reason behind the trends in sugar? Yes. The market hit its 2023 peak due to adverse weather in Brazil, the world’s largest producer and exporter of the commodity. But like normal weather markets of the past, supplies were rebuilt with the next harvest and improved weather the past few years have resulted in larger crops.

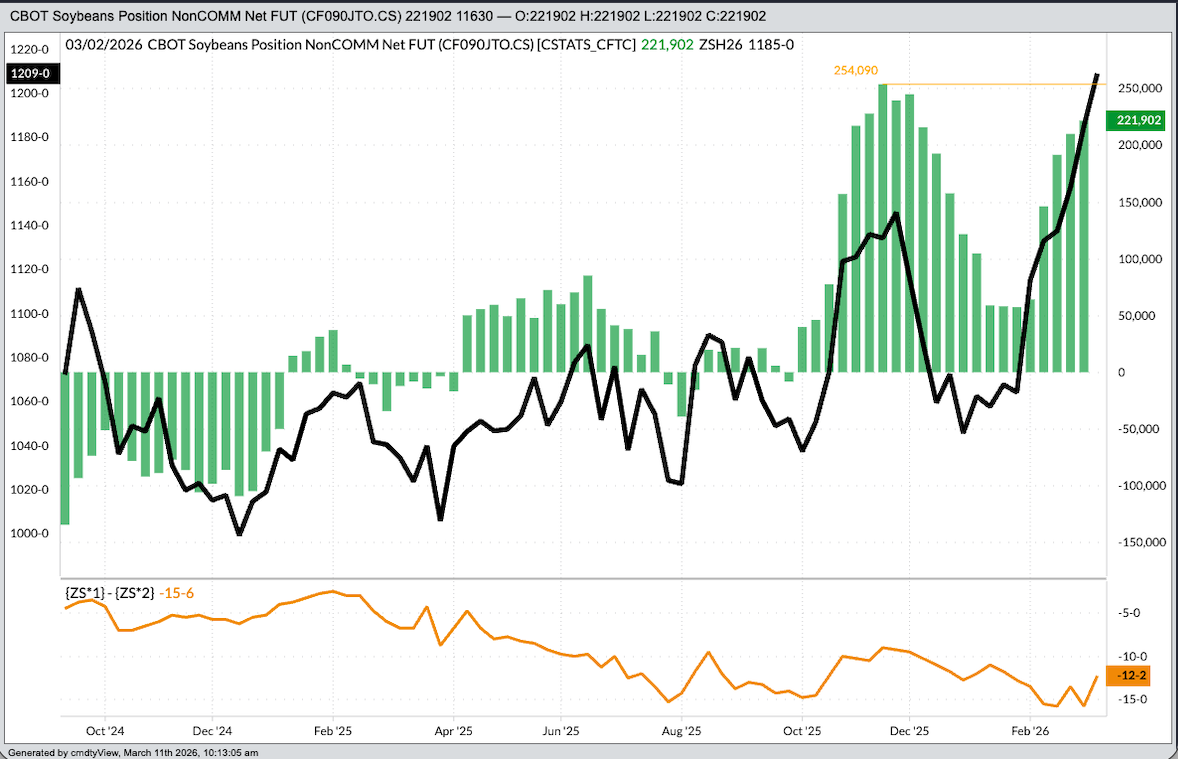

It’s a similar story in soybeans. The latest Commitments of Traders report put the noncommercial net-long futures position at 221,900 contracts, an increase of 11,630 contracts from the previous week. However, from last Tuesday’s settlement through last night’s close the May issue (ZSK26) added 31.5 cents indicating continued fund buying, possibly to the point of testing last fall’s largest net-long futures position of 254,090 contracts. Here’s where things get interesting. By late last summer, Watson held a net-short futures position of as much as 39,160 contracts. Then the US president started in with a few not necessarily the Truth Social media posts talking about how much China was going to buy, and algorithms were triggered into buying. After the net-long futures position peaked in late October, reality set back in and funds started liquidating, leading to the expected selloff in soybean futures. Once again, though, starting in late January, similar social media posts were made, this set including the great things that were going to happen with domestic crush demand, and Watson was fooled into buying, rallying the futures market roughly $1.50.

Have the fundamentals actually changed? As of the end of January, the US export pace projection was 1.168 billion bushels, down 670 mb (37%) from reported total export shipments the previous marketing year (1.841 bb). At the same time, the end of January, the US had crushed a total of 1.121 bb of soybeans, an increase of 77 mb (7%) from the previous marketing year. Quickly doing the math, total usage from these two key categories of demand still showed a decrease of nearly 600 mb from the previous year. But that is fundamental talk, and as we can now see, a complete waste of time.

How then should we approach market analysis? We know Watson doesn’t use traditional technical analysis, at least as it pertains to trendlines and patterns (head and shoulders, reversals, etc.), putting more of an emphasis on factors such as momentum and volatility. And social media posts. Yes, social media posts have replaced the study of real supply and demand as National Cash Price Indexes, basis, and futures spreads can be skewed by explosive activity in the nearby futures contract.

The game now is to predict what the next post will be.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.