The controversial Affordable Care Act (ACA), commonly known as Obamacare, was enacted in 2010 with grand promises of lowering health insurance premiums while expanding coverage to millions of Americans. Although it succeeded in providing insurance to many who previously lacked it, the pledge of reduced premiums proved short-lived. Instead, most enrollees witnessed significant premium surges (although at a slower rate than employee-based premiums).

To bolster the program, President Biden's American Rescue Plan Act of 2021 and Inflation Reduction Act of 2022 introduced and extended enhanced premium tax credits. However, these subsidies are now expiring, causing premiums to skyrocket once again. As a result, millions of enrollees are abandoning the exchanges, severely impacting Centene (CNC), the nation's largest provider of Obamacare policies.

Grim Forecast Leads to Sharp Decline

CNC stock plummeted 15% yesterday after executives warned that roughly 40% of its Obamacare members could drop coverage this year amid the subsidy cliff. ACA marketplace enrollment for the company is already falling 36% to 3.5 million members in the first quarter, down from 5.5 million at the end of 2025. The reaction sent shares to around $36.40, erasing recent gains in a single session.

In 2026 so far, CNC stock has posted negative returns of 13% amid broader uncertainty in government-sponsored health plans, reflecting early volatility tied to policy shifts and enrollment data. Over the past year, the shares have declined 39%, underperforming the broader market as investors priced in the end of enhanced subsidies and rising medical costs across Centene’s book. This marks a stark reversal from prior years when ACA growth fueled optimism.

A Double-Edged Sword for Revenue and Profits

For Centene, the ACA marketplace has long been a critical engine of growth. The segment—primarily through its Ambetter plans—drove substantial premium and service revenue increases in recent years, contributing tens of billions annually and helping offset Medicaid fluctuations. In 2025, marketplace membership surged, boosting overall premium revenues by 20% company-wide and playing a key role in profitability before the subsidy expiration.

Now, however, the rapid membership exodus is reshaping the outlook. Centene has already lowered its 2026 revenue guidance, citing the sharp contraction in marketplace lives and higher per-member costs as healthier enrollees exit. Profits are taking a hit too, with elevated health benefits ratios in the commercial segment pressuring margins. As the largest Obamacare insurer by far, Centene bears disproportionate exposure; what was once a tailwind has become a significant drag on both top- and bottom-line results.

Medicaid Pressures Add to the Challenges

While ACA woes dominate headlines, changes in Medicaid reimbursement policies have also influenced Centene’s performance, though the impact has been more mixed than catastrophic. As the country’s biggest Medicaid managed-care provider, the business still accounts for the lion’s share of revenue—roughly half or more in recent reporting periods. Rate increases of 5.5% in 2025 provided a solid base, and Centene expects composite rate growth around 4.5% this year, helping stabilize medical loss ratios that improved sequentially to 93% in late 2025.

Still, utilization pressures from behavioral health, home care, and high-cost drugs have kept margins tight in some states. Proposed federal reforms and ongoing state-level adjustments have introduced variability, occasionally leading to goodwill impairments or conservative guidance. These dynamics have compounded the ACA-related pain, forcing the company to focus on cost controls and network optimization to protect profitability.

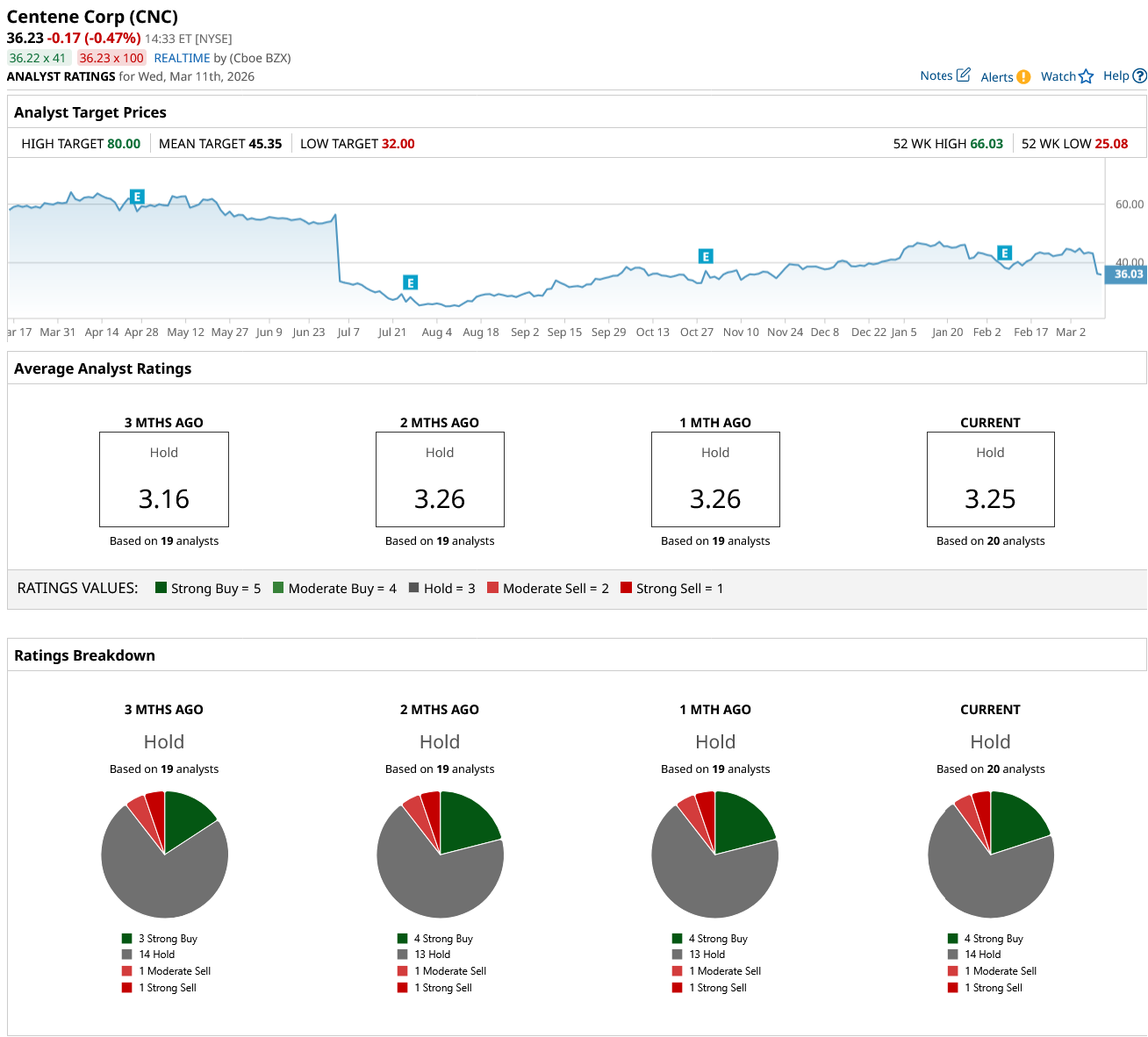

Analyst Opinions Remain Cautious

Wall Street analysts are largely taking a wait-and-see approach. Analysts' consensus rating on CNC is a “Hold,” based on input from 20 analysts. The mean price target sits around $45.35, implying roughly 25% upside from current levels even after the recent plunge. High targets reach near $80, while lows hover around $32, reflecting a wide range of views on how quickly the company can pivot away from ACA exposure.

Recent rating adjustments show slight softening in optimism, but many still credit Centene’s scale in Medicaid and Medicare for long-term resilience.

Bottom Line

Following the cue of the Street's analysts, CNC should be considered a “Hold.” At current prices, the stock trades at a noticeable discount to its historical average valuation multiples—where forward price-to-earnings ratios have typically ranged higher—and appears inexpensive compared with managed-care peers on price-to-sales metrics. The discount reflects legitimate risks from ACA enrollment erosion and Medicaid variability, yet it also embeds a margin of safety for investors betting on stabilization.

Until clearer evidence emerges on membership retention and margin recovery, however, aggressive buying looks premature.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should Risk-Takers Roll the Dice on These 3 Penny Stocks at 52-Week Lows?

- As Archer Aviation Joins a DoT Pilot Program, Should You Buy, Sell, or Hold ACHR Stock?

- Analysts Are Still Betting That Oracle Stock Can Gain 150% Over the Next 12 Months. Should You Buy ORCL Here?

- 3 Analyst-Approved Stocks With Fat Yields That Could Rally 27% or More