Uncertainty and instability surrounding the Iran war have been weighing heavily on sentiments, and the S&P 500 Index ($SPX) has closed in the red for three consecutive weeks. While the world’s most popular index is down just over 2% for the year, the pain has been particularly severe in tech names, which are also reeling from fears of a possible artificial intelligence (AI) bubble.

Meanwhile, Apple (AAPL), which largely held its ground last month amid the tech and software selloff, has also looked under pressure. The stock is down 7% for the year and is in correction territory after plunging over 12% from its recent highs. In my previous article, I had noted that AAPL was a hedge against the tech selloff, as usually the iPhone maker tends to outperform its “Magnificent 7” peers in periods of economic turmoil.

However, the global macro environment has worsened over the last couple of weeks as the war in Iran threatens the benign crude oil price environment that consumers, central bankers, and governments had grown so used to. Let's dig into whether AAPL stock is a buy now or if investors would be better off waiting for a lower entry point.

iPhone Sales Have Picked Up

Apple's recent financial performance has been impressive, and after many quarters of muted growth, Apple reported a 16% year-over-year (YoY) rise in revenues for the December quarter, with the top end of its guidance calling for a similar growth in the current quarter. It was particularly encouraging to see a pickup in iPhone sales and the 37% rise in revenues in the Greater China region, which, of late, has been a challenging market for the Cupertino-based company.

Apple’s Services business continues to do well, with revenues rising 14% YoY in the December quarter to a record high. Apple’s installed base of devices has topped 2.5 billion, which bodes well for the future growth of the company’s Services business. However, the so-called “Apple tax,” or the hefty fees the company levies on App Store purchases, has been facing scrutiny, and the U.S. tech giant has had to lower the fees in China from 30% to 25%. The services business is quite lucrative for Apple, and the segment generated a gross profit margin of 76.5% in the most recent quarter, while the corresponding number for Products was 40.7%.

AAPL Stock Forecast

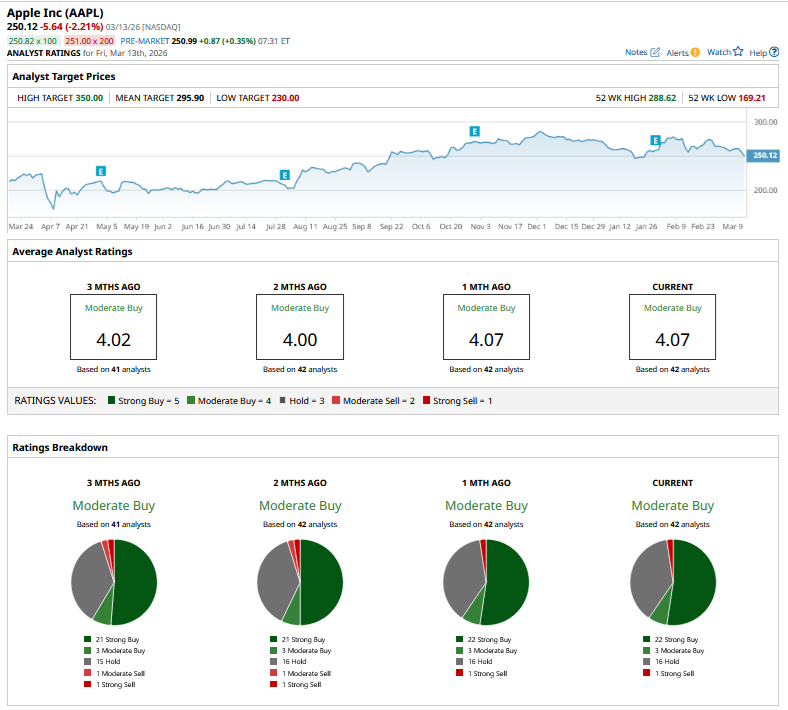

Analyst action has been quite muted when it comes to AAPL stock over the last two months, and there have just been cursory target price tweaks, including after the fiscal Q1 2026 earnings report. AAPL started the year with a downgrade from Raymond James, though. It is, in fact, the third consecutive year when Apple received a downgrade right at the beginning of the year, even as the number of downgrades this year is much lower than in the previous two years.

The company’s MacBook Neo and the iPhone 17e did receive positive reviews from analysts, but the optimism hasn’t really flowed into their target prices, and Apple is rated as a “Moderate Buy” by the 42 analysts tracked by Barchart. It carries a mean target price of $295.9, which is 18.3% higher than last week’s closing prices.

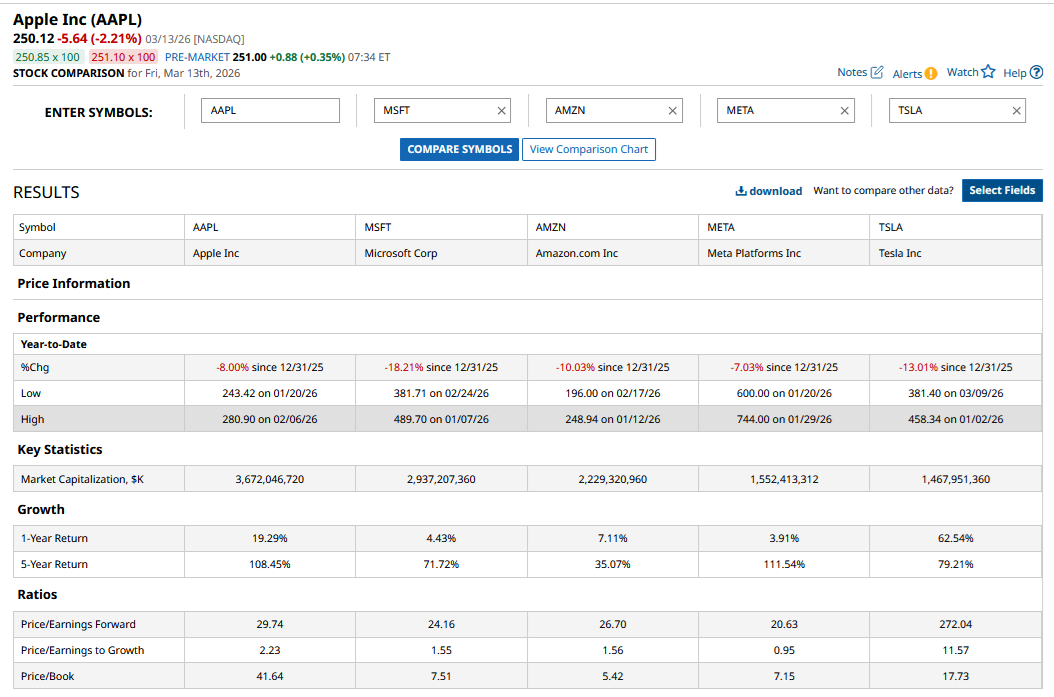

The key reason analysts have been frugal with raising Apple’s target price is the stock’s rich valuations. It was trading at a forward price-to-earnings multiple in the mid-30s, which made it tough to build a compelling “buy” case for the stock. Even after the recent correction, AAPL stock’s forward P/E has dipped slightly below 30x, which I don’t find too attractive, though I'd still suggest cautiously buying the stock, as the risk-reward looks more favorable now.

Apple has indeed tasted success with the iPhone 17 lineup, and the Tim Cook-led company has yet again displayed its supply chain resilience as it was able to mostly dodge the sharp rise in tariffs. However, there are several headwinds that investors should watch out for, especially as the race for the next computing platform heats up with companies like Alibaba (BABA), Meta Platforms (META), and, apparently, even OpenAI looking to crack the code with smart glasses.

On the date of publication, Mohit Oberoi had a position in: AAPL , META , BABA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.