Amazon (AMZN) CEO Andy Jassy recently set a jaw-dropping new target for the company's cloud computing unit. If he's right, the upside for Amazon investors could be massive. The boldness of Jassy's vision is hard to ignore. He told employees during an internal all-hands meeting on March 17 that Amazon Web Services (AWS) could one day reach $600 billion in annual revenue, double what he had previously thought possible.

Amazon Web Services ended 2025 with revenue of $128.7 billion, which indicates the cloud segment could expand by about 300% from current levels.

AWS Is the Key Revenue Driver

Despite its massive size, AWS is growing steadily. In Q4 2025, it posted 24% year-over-year revenue growth, the fastest pace in 13 quarters, reaching an annualized run rate of $142 billion. As Jassy noted on the earnings call, growing 24% on a $142 billion base adds far more real dollars than growing at a higher percentage on a smaller one.

Jassy also flagged that demand is outpacing supply. AWS added more data center capacity than any other company in the world in 2025, including more than 1 gigawatt of new capacity in Q4.

The company added 3.9 gigawatts of power over the past 12 months, twice as much as it had in all of 2022. And yet, by Jassy's own admission, AWS could be growing even faster if it had more supply to offer. This supply crunch is part of why Amazon is committing $200 billion in capital spending in 2026, with most of it directed to AWS.

A Focus on Amazon’s AI Moat

A key part of Amazon's AI strategy is its custom silicon.

- The company's Trainium2 chip delivers 30% to 40% better price performance than comparable GPUs, and the faster Trainium3, 40% better than Trainium2, is expected to be nearly fully committed by mid-2026.

- Together with Graviton, Amazon's CPU chip, the chips business now generates over $10 billion in annual revenue, growing in the triple digits year-over-year.

- These chips make Amazon's own AI services cheaper to run, improving margins while giving customers a reason to stay within the AWS ecosystem.

On the partnerships front, Amazon has locked in major agreements. OpenAI, in a deal worth up to $50 billion, will use Amazon's Trainium chips. Anthropic, the AI safety company, is training its next flagship model on AWS through a project called Rainier, which now uses 500,000 Trainium2 chips. Amazon's Bedrock AI platform, which gives developers access to models from Anthropic, Mistral, and Amazon's own Nova series, saw customer spending grow 60% quarter-over-quarter. Bedrock is now a multibillion-dollar business in its own right.

AWS backlog stood at $244 billion at the end of Q4, up 40% year-over-year and 22% quarter-over-quarter. That's a massive pipeline of committed future revenue.

The Bull Case for Amazon Investors

Jassy said it plainly on the earnings call: "As fast as we install this capacity, this AI capacity, we are monetizing it."

The message to investors is clear. AI demand is real, it's growing, and Amazon has both the infrastructure and the technology to capture a disproportionate share of it. If Jassy's $600 billion vision for AWS even partially comes true, Amazon's stock could look very different in five to 10 years.

Amazon's overall net sales hit $716.9 billion in 2025, up 12% year-over-year. The company's operating income for the full year was strong, and AWS alone generated $12.5 billion in operating income in Q4 at a 35% margin.

Analysts forecast Amazon to increase revenue from $717 billion in 2025 to $1.22 trillion in 2030. In this period, adjusted earnings are forecast to expand from $7.17 per share to $16.44 per share.

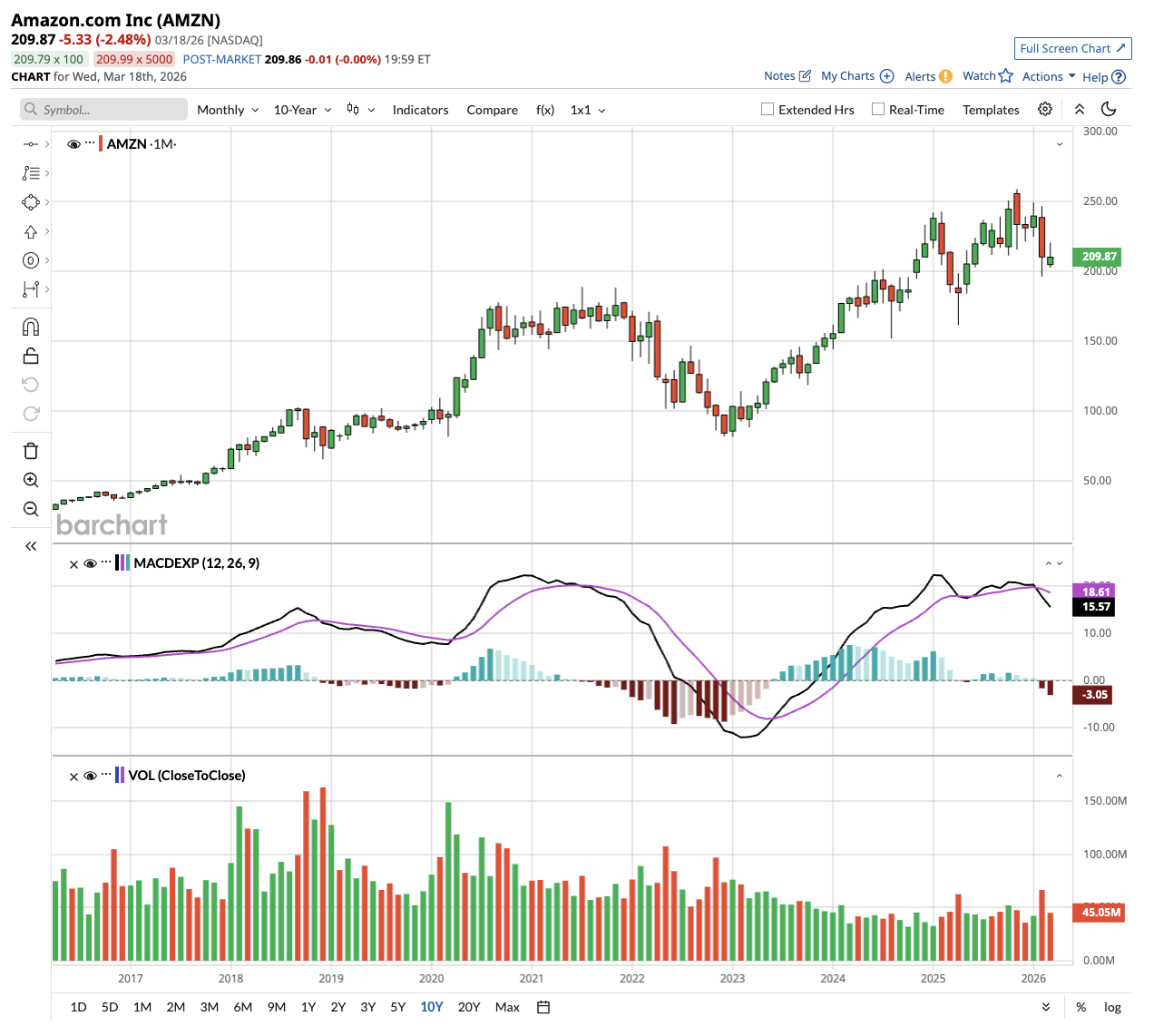

If AMZN stock is priced at 27x forward earnings, which is similar to its current multiple, it could surge to $445 in early 2030, indicating upside potential of more than 100% from current levels.

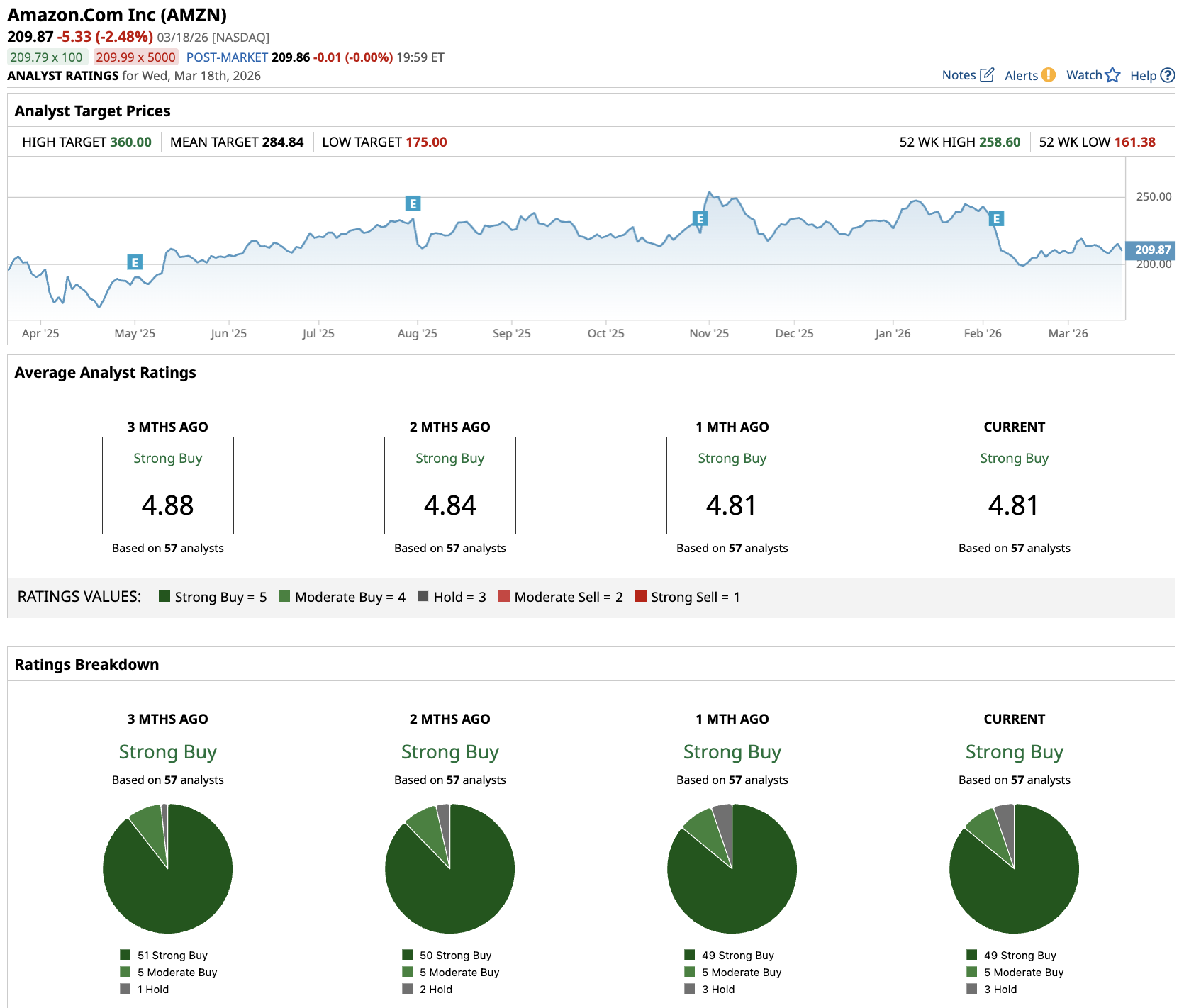

Out of the 57 analysts covering AMZN stock, 49 rate it a “Strong Buy,” five recommend it as a “Moderate Buy,” and three rate it a “Hold.” The average AMZN stock price target is $285, significantly above the current price.

For investors looking for a stock with a credible, AI-driven growth story backed by real revenue and a CEO who has been consistently right about the cloud, Amazon deserves a hard look right now.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart